(Bloomberg) — After coming under attack from both environmentalists and investors in the first half of his seven-year tenure at the helm of Exxon Mobil Corp., Darren Woods is on the offensive.

Most Read from Bloomberg

Already this year, Woods filed an arbitration case against Chevron Corp. for attempting to buy into Exxon’s massive offshore oil project in Guyana and a lawsuit against investors demanding that his company cut emissions. Just months earlier, he agreed to a $60 billion takeover that would make Exxon the biggest US shale producer.

Woods is also becoming much more strident about climate goals in speeches and interviews, arguing that fossil fuels will still be needed for years to come to meet energy demand and the world is not on a path to net-zero carbon emissions by 2050 because people are unwilling to pay for cleaner alternatives.

The message may be controversial, but it’s resonating on Wall Street, where “ESG” is fast becoming a loathed moniker as ambitious environmental, social and governance pledges are rubbing against the need for secure and affordable energy. Exxon is up 89%, more than four times that of the S&P 500, since losing a climate-fueled proxy battle with Engine No. 1. in 2021.

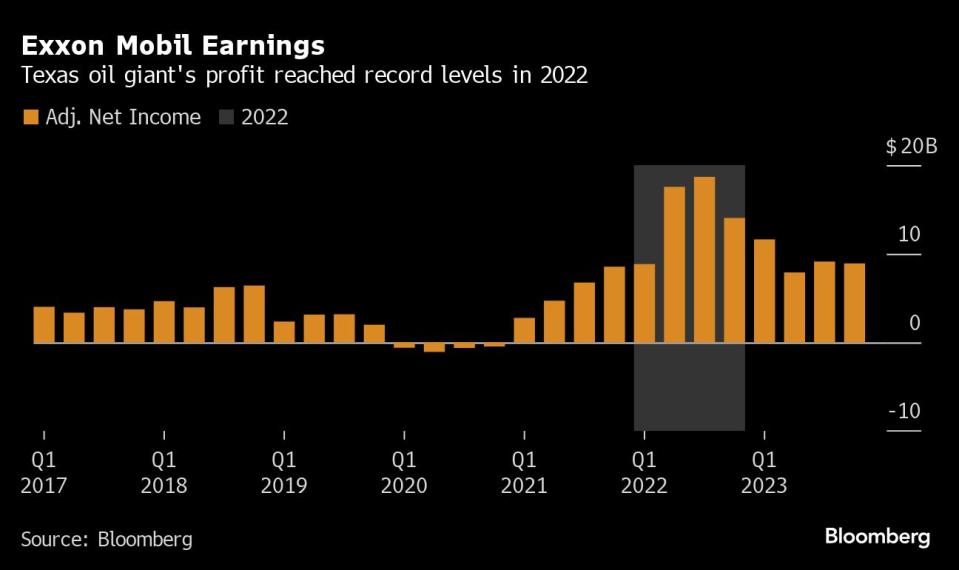

It’s a remarkable turnaround from the pandemic era, when Exxon posted its biggest-ever loss, employees were leaving in droves and the shareholder rebellion forced Woods to replace a quarter of his board. Exxon’s revival is emblematic of a resurgent American oil industry, which is now pumping 40% more crude each day than Saudi Arabia, forcing OPEC and its allies to retreat.

“It wasn’t that long ago it looked like taking the green approach was what the industry needed to attract capital,” said Jeff Wyll, a senior analyst at Neuberger Berman, which manages about $440 billion. But Russia’s invasion of Ukraine “flipped the switch and energy security became more important. Exxon benefited because they never stepped back from their traditional business.”

When Woods takes center stage at the CERAWeek by S&P Global energy conference in Houston this week, he’s likely to double down on his long-held view that fossil fuels will be in demand for decades to come and that governments and consumers — rather than just Big Oil — will need to pay for any meaningful transition to greener energy.

For those who see Exxon and Big Oil as responsible for decades of delay and misinformation about climate change, it’s an unpopular argument. But it’s one made from a position of increasing financial strength.

Exxon paid out $32 billion in dividends and buybacks in 2023, the fourth-highest in the S&P 500, and is pledging more this year. Its pending $60 billion acquisition of Pioneer Natural Resources Co. will make it the country’s dominant producer of shale oil, putting it at the top of the industry largely responsible for OPEC+ losing market share to the US.

Exxon also operates one of the world’s fastest-growing major oil developments in Guyana, the biggest crude discovery in a decade, and recently completed a raft of refinery and petrochemical expansions.

Its supermajor rivals are now racing to catch up.

Chevron agreed to buy Hess Corp. for $53 billion, in large part to gain a 30% stake in Exxon’s Guyana project. But Exxon claims the deal “attempted to circumvent” a contract that gives it right of first refusal over the stake, and is taking the dispute to arbitration at the International Chamber of Commerce in Paris.

Shell Plc and BP Plc, meanwhile, are now switching more of their investment dollars back toward oil and gas under new CEOs after their stocks slumped following a pivot toward renewables.

The European supermajors’ struggles demonstrate the perils of replacing high, steady cash flows from fossil fuels with low-margin renewables, according to Greg Buckley, a portfolio manager at Adams Funds who helps manage about $3.5 billion including Exxon shares.

“ESG was popular but I think that return on capital is more popular at the end of the day,” he said. Shell and BP “found out the hard way.”

The shift away from ESG terminology is a recognition that the energy transition will be complex and won’t unfold the same way in every part of the globe, Dan Yergin, the vice chairman of S&P Global, which organizes the CERAWeek conference, said in an interview. Conflicts around the world, including in the Middle East and Ukraine, have underscored the need for reliable energy supply, while investors remain focused on returns, he said.

“The energy companies have demonstrated a discipline in their capital investment and have been responsive to investors,” Yergin said. “You can see that in their spending and that’s refurbished the social contract between the companies and investors.”

Woods is also learning from his own experience with activist shareholders. In January, the company filed a lawsuit against US and Dutch climate investors who buy stock to push for lower emissions. The process by which they get votes on the ballot at company meetings “has become ripe for abuse by activists with minimal shares and no interest in growing long-term shareholder value,” Exxon said in the suit.

Woods is also being more vocal about his views on a lower-carbon future. “The dirty secret nobody talks about is how much all this is going to cost and who’s willing to pay for it,” he said in a recent Fortune podcast. The world “waited too long” to consider all the solutions needed to reduce emissions.

The comments invoked ire from environmentalists.

“It is an infuriating bit of rhetoric, especially from Exxon because they are the most associated with the effort to slow progress on climate change,” said Andrew Logan, oil and gas senior director at CERES, a coalition of environmentally-minded investors with $65 trillion under management. “They have a long history of over-promising and under delivering on low carbon.”

Emily Mir, a spokeswoman for Exxon, pushed back at Logan’s comments in a statement. The company has said it’s pursuing more than $20 billion in lower-emission investments from 2022 through 2027, in addition to its $4.9 billion acquisition of Denbury Inc., a deal that gave the oil giant the largest network of carbon dioxide pipelines in the US. Those pipes will be key to capturing carbon from heavily polluting facilities like refineries and chemical plants.

“Facts that don’t align with ill-informed prejudice are often infuriating,” Mir said. “That doesn’t make them wrong. Someone needs to tell the truth about what it’s going to take to get to a net-zero future.”

In November, Woods tried to flip the script on a slogan from the long-running “ExxonKnew” environmental campaign, which claims that company executives downplayed warnings from their own scientists since the 1970s that carbon dioxide causes climate change. Exxon has denied deliberately misleading the public on global warming.

“We’ve got the tools, the skills, the size — and the intellectual and financial resources — to bend the curve on emissions,” he said at the APEC CEO Summit 2023 in San Francisco. “That’s what Exxon Mobil knows.”

But the energy transition still looms large. Fears that oil demand will peak as soon as 2030 have led investors to discount the ability of Exxon and its peers to sustain dividends and buybacks as the transition takes hold. The S&P 500 is now dominated by tech stocks, whose earnings are seen as more resilient for decades into the future.

Even after its rally over the past few years, Exxon is only the S&P 500’s 17th largest company, trading at 12.2 times earnings, 42% below the index’s average. Energy stocks make up less than 4% of the index despite the US becoming the world’s biggest oil producer.

“Exxon and the industry has yet to make a case of how they will generate cash in a carbon-constrained future,” Logan said.

—With assistance from Naureen S Malik.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}