US futures extend their record-breaking meltup following the long weekend (which was to be expected with hedge funds piling into shorts last week, hoping for a reversal), with most European markets still closed and Asian stocks closing lower. As of 7:30am, S&P futures were 0.3% higher, but trading near session lows; Nasdaq futures gained 0.4%. Bond yields are 1-3bp higher with the USD unchanged from its Friday close. Commodities are mixed: oil down and metals are mostly higher this morning as China PMIs beat expectations. While bitcoin suffered one of its trademark futures slamdowns overnight to push it back below $70K despite relentless ETF inflows, gold was on a tear and rose 1.6% to hit a new all time high of $2,265 before easing back. after upbeat China factory data added to Friday’s relatively benign US core PCE figures. This week, keep an eye on Payrolls, ISMs, and Fedspeak (8x this week), and today, we get the Mfg ISM at 10am ET where consensus expects a 48.3 print vs. 47.8 prior.

In premarket trading, megacap tech names were mostly higher with NVDA/MU/AMD up more than 1%. AT&T fell as much as 2% in premarket trading after the telecom giant said that personal data from about 7.6 million current account holders and 65.4 million former customers was leaked onto the dark web. Nikola rose as much as 16% in premarket trading, set to extend gains for a record-setting ninth consecutive session.

A slow down in the Fed’s preferred measure of inflation last month, coupled with a rebound in household spending, suggests that bullish narratives that propelled stocks to records this year remains intact. The core PCE price index, which strips out the volatile food and energy components, rose 0.3% from the prior month, slowing from January’s surprisingly strong reading, suggesting the Fed is still on pace for a June rate cut.

With markets in Europe, Australia and Hong Kong still shut for the Easter holiday, Asian stock benchmark which were open fell in the first trading day of the second quarter, as investors sold Japanese shares following a record-breaking rally and bought into Chinese equities. The MSCI Asia Pacific Index declined as much as 0.7%, with Toyota and Mitsubishi UFJ Financial among the biggest drags. Following the strongest quarter for the Nikkei 225 average in almost 15 years, investors booked profits as Japan’s new fiscal year kicked off and Japanese equities fell after a report showed confidence among the country’s large manufacturers weakened.

Meanwhile, China stocks led gains in Asia on Monday following a rebound in domestic manufacturing activity that reinforced hopes that economic growth is gaining traction. Chinese stocks rallied as a rebound in manufacturing activity reinforced hopes that the nation’s economic recovery may be starting to gain traction. The benchmark CSI 300 Index rose 1.6% to lead gains in Asia. “Emerging optimism about China is real,” said Vishnu Varathan, chief economist for Asia ex-Japan at Mizuho Bank in Singapore. Benchmarks in Taiwan and Indonesia were lower, while those in India, South Korea and Singapore climbed. Markets in Hong Kong, Australia and New Zealand were shut for a holiday.

In FX,

In rates, the Treasury yield curve remained steeper vs Thursday’s close after gapping wider at the Asia open. Front-end yields are richer by around 2bp after opening gapping lower, with many European markets still closed. Front-end outperformance steepens 2s10s spread by nearly 3bp, 5s30s by more than 3bp. 10-year yields around 4.21%, up ~1bp; 30-year yields are cheaper by almost 3bp on the day at around 4.37% The front-end outperformance stems from February PCE deflators released Friday and comments by Fed Chair Powell that left intact expectations for rate cuts this year. US session includes manufacturing PMIs; ahead this week are several Fed speakers and March jobs report. Fed-dated OIS contracts price in slightly more rate cuts for the year vs Thursday, with 74bp of easing expected by December vs 70bp prior.

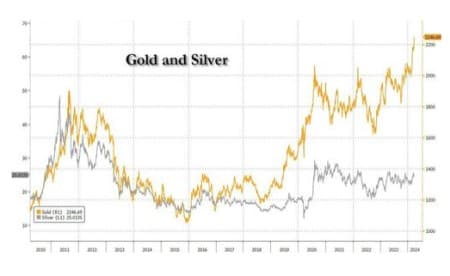

In commodities, oil dipped after hitting a fresh 5 month high last week. Gold jumped to a record as indications the Federal Reserve is getting closer to cutting interest rates added impetus to a rally that’s also been driven by geopolitical tensions and robust Chinese demand. Bullion jumped to as much as $2,265.73 an ounce on Monday, up 1.6% from Thursday’s close, after setting a series of peaks in recent sessions. Silver meanwhile continue to underperform and remains about 50% below its 2011 highs.

A host of positive drivers have pushed up bullion by around 14% since the middle of February. The prospect of monetary easing by major central banks, and elevated tensions in the Middle East and Ukraine have underpinned the rally. There’s also been strong buying by central banks, particularly in China, while consumers there have been loading up on the metal amid ongoing problems in Asia’s largest economy.

US economic data slate includes the US manufacturing PMI (9:45am), February construction spending and March ISM manufacturing (10am); ahead this week are JOLTS job openings and factory orders (Tuesday), ADP employment change and services PMIs (Wednesday), and the March jobs report. Fed speaker slate includes Cook at 6:50pm; Bowman, Williams, Mester, Daly, Goolsbee, Powell, Barr, Kugler, Harker, Barkin, Musalem and Logan have appearances scheduled.

Market Snapshot

- S&P 500 futures up 0.4% to 5,328.75

- MXAP down 0.6% to 175.87

- MXAPJ little changed at 537.52

- Nikkei down 1.4% to 39,803.09

- Topix down 1.7% to 2,721.22

- Shanghai Composite up 1.2% to 3,077.38

- Sensex up 0.5% to 74,022.68

- Kospi little changed at 2,747.86

- Brent Futures up 0.2% to $87.18/bbl

- Gold spot up 1.3% to $2,258.11

- US Dollar Index little changed at 104.50

Top Overnight News

- China’s NBS PMIs for March came in solidly ahead of expectations, with manufacturing at 50.8 (up from 49.1 in Feb and above the Street’s 50.1 forecast) and non-manufacturing at 53 (up from 51.4 in Feb and above the Street’s 51.5 forecast). China’s Caixin manufacturing PMI came in at 51.1 for Mar, a small beat vs. the consensus forecast of 51 and up modestly from 50.9 in Feb. FT

- Some of the biggest U.S. companies in artificial intelligence have asked their Taiwanese manufacturing partners to step up production of AI-related hardware in Mexico, seeking to diminish reliance on China. Taiwan-based Foxconn, the world’s largest contract electronics manufacturer, and other Taiwanese companies are heeding the call and investing more in Mexico, according to industry executives and analysts. WSJ

- Taiwan’s former president, Ma Ying-jeou, is set to visit mainland China, and could meet with Xi, a sign of Beijing being receptive to certain politicians that favor closer ties. NYT

- Turkey’s main opposition defeated Recep Tayyip Erdogan in the country’s local elections, claiming big wins in Istanbul and Ankara as voters pushed back amid rampant inflation. It won’t lead to any reversal in the country’s pivot to a restrictive monetary policy. BBG

- Tens of thousands of people demonstrated in Jerusalem on Sunday against Benjamin Netanyahu’s government and against exemptions granted to ultra-Orthodox Jewish men from military service, in scenes reminiscent of mass street protests last year. Protest groups, including some that led the mass demonstrations that rocked Israel in 2023, organized the rally outside parliament, the Knesset, calling for a new election to replace the government. RTRS

- Venezuela likely won’t see the US fully reimpose energy sanctions as Washington fears doing so could drive gas prices higher during an election year (one scenario under discussion would permit int’l buyers to continue purchasing Venezuelan oil, but not with US dollars). WaPo

- US PCE for Feb was largely inline with expectations. The headline number came in at +0.3% M/M (vs. the Street +0.4%) and +2.5% Y/Y (vs. the Street +2.5% and vs. +2.4% in Jan). Powell spoke Friday afternoon (after the Feb PCE, personal spending, and personal income data hit), and his tone was largely consistent with the recent post-meeting press conference. NYT

- AT&T fell premarket after saying personal data from about 7.6 million current account holders and 65.4 million former customers was leaked onto the dark web. BBG

- MSFT & Open AI are apparently planning a massive ~$100B supercomputer project that would contain millions of specialized server chips to power OpenAI’s services and software. The Information

- Info Tech and Communication Services were the most net sold sectors on our US Prime book last week, driven almost entirely by short sales. The group collectively made up ~75% of last week’s notional net selling in all US Single Stocks. TMT stocks collectively now make up 29.1% of total US single stock Net exposure (vs. YTD high of 32.5% seen in mid-February), which is in the 2nd percentile vs. the past year and in the 13th percentile vs. the past 5 years.

US Event Calendar

- 09:45: March S&P Global US Manufacturing PM, est. 52.5, prior 52.5

- 10:00: March ISM Employment, prior 45.9

- March ISM New Orders, est. 49.8, prior 49.2

- March ISM Prices Paid, est. 52.9, prior 52.5

- March ISM Manufacturing, est. 48.3, prior 47.8

- 10:00: Feb. Construction Spending MoM, est. 0.7%, prior -0.2%

By Zerohedge.com

More Top Reads From Oilprice.com:

- Exxon and CNOOC Team Up To Challenge Chevron’s Guyana Oil Deal

- Baltimore Port Closure Threatens U.S. Coal Exports

- Natural Gas Producers Are Ready To Pounce When Prices Rebound

Read this article on OilPrice.com

This story originally appeared on Oilprice.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}