US stocks wobbled on Monday as investors kicked off a big week that will see a fresh inflation data test for rate-cut views and the start of first-quarter earnings season.

The Dow Jones Industrial Average (^DJI), the S&P 500 (^GSPC) and the tech-heavy Nasdaq Composite (^IXIC) wavered around the flatline after opening with slight gains.

A strong jobs report helped lift stocks on Friday but couldn’t fend off weekly losses as doubts about the Federal Reserve’s resolve for interest-rate cuts preyed on minds.

US bonds sold off last week amid that uncertainty, and the pressure continued Monday with a slight rise in the 10-year Treasury yield (^TNX) to above 4.45%. While the benchmark has pared gains, it is still within reach of the key 4.5% level seen by some as a potential tipping point for a run-up toward last year’s highs.

Other concerns added to the unsettled mood: Divided views on policy from Fed speakers, growing noise around the coming US presidential election, and a spike in oil prices from escalating Middle East tensions that could fan inflation pressures.

All that is sharpening focus on the release of the Consumer Price Index on Wednesday, a key input in the Fed’s decision making and a clue to continuing resilience in the US economy. Investors will watch for signs that inflation returned to its downward trend in March after signs of stickiness in readings earlier this year.

At the same time, the market is bracing for the new earnings season, with Delta Air Lines (DAL) setting the stage on Wednesday for big banks’ results on Friday. Broadly, Wall Street expects the first quarter to set the tone for a robust year of earnings growth among S&P 500 companies, hopes boosted by the blowout March labor figures.

Against that backdrop, gold rose above $2,350 an ounce to touch a fresh record. Meanwhile, oil was reaching for recent multimonth highs as the market assessed easing tensions in the Middle East. Brent crude futures (BZ=F) were slightly lower at $90.80 a barrel, while West Texas Intermediate futures (CL=F) were a touch higher at just below $87.

Live9 updates

-

-

Oil futures pull back amid signs of easing Middle East tensions

Oil futures pulled back roughly 1% on Monday amid some signs of easing tensions in the Middle East.

West Texas Intermediate (CL=F) futures were trading above $85 while Brent (BZ=F) traded around the $90 level after Israel agreed to remove some ground troops from the southern Gaza area.

“Still, the growing demand picture remains a tailwind for crude,” Dennis Kissler, senior vice president at BOK Financial said in a note on Monday.

The analyst noted oil has risen by roughly $7.00 in the last two weeks.

“Caution is warranted as the “overbought” condition is also carrying heavy fund long positions that may have pushed up prices a bit too much too fast,” wrote Kissler.

WTI has risen roughly 16% year-to-date. Brent climbed 15% during the same period.

-

-

-

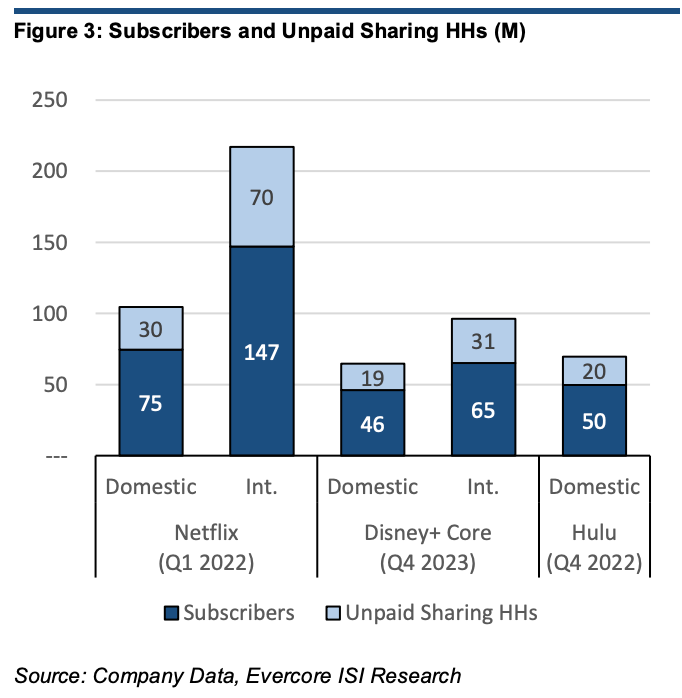

Disney’s potential lift from password sharing crackdown

Disney (DIS) has a lot of password sharers to crack down on.

The media giant is expected to begin tightening the grips on password sharing for Disney+ and Hula this June, teased CEO Bob Iger in a Friday TV interview.

A new chart from EvercoreISI analyst Vivant Jayant (below) sheds light on how impactful a password sharing crackdown could be to the streaming division’s profitability.

Disney will follow Netflix and crack down on password sharing. (EvercoreISI) -

-

-

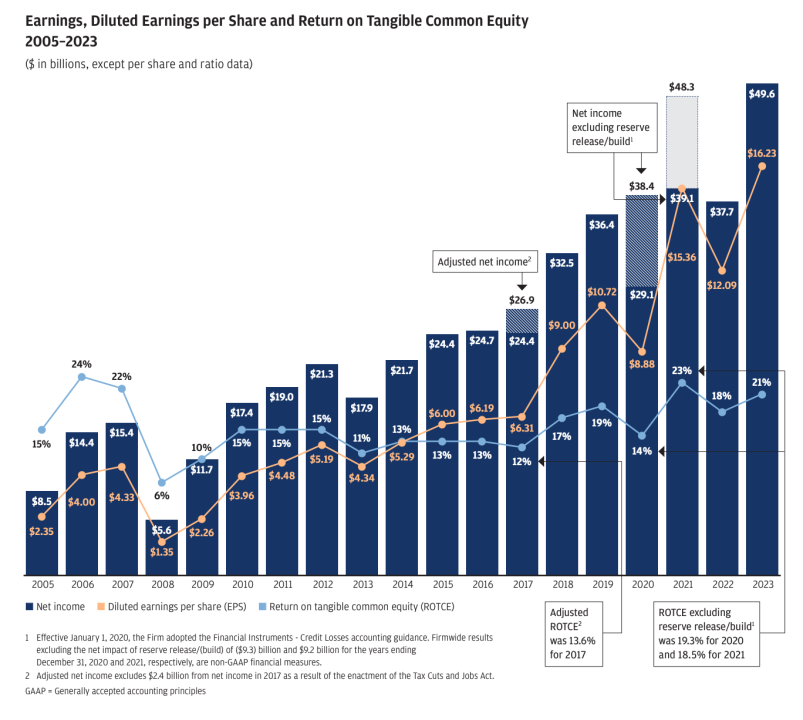

JP Morgan CEO Jamie Dimon’s masterclass in making money, in one chart

Want to know why JP Morgan (JPM) investors hope Jamie Dimon stays CEO for 50 more years?

Sure, the guy is the face of banking with the best relationships in the game, but at the end of the day — he just knows how to make jobs of money for shareholders.

That’s perfectly captured in Dimon’s annual letter out this morning. Check out this chart on page 8, showing how JP Morgan’s net income has grown by about six times since 2005.

The money machine that is JP Morgan. (JP Morgan) -

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}