(Bloomberg) — Gold’s rally to successive all-time highs isn’t over, according to macro fund managers interviewed by Bloomberg, with the factors that have powered a near-20% surge since mid-February expected to fuel more gains.

Most Read from Bloomberg

The gains have been fueled by expectations for the US Federal Reserve to lower interest rates this year — an environment that reduces the opportunity cost of holding the metal. Meanwhile, messy conflicts in the Middle East and Ukraine support demand for safe-haven assets, and purchases by global central banks add to a bullish backdrop.

The current momentum is a signal to increase holdings in gold, according to Rajeev De Mello, global macro portfolio manager at GAMA Asset Management SA. Prices may now be vulnerable to a slight correction, he said, but any pullback is likely to bring in more buyers.

“It’s a relatively small market and it can squeeze higher very fast,” he said, comparing it to the size of US government debt securities. “It’s a very momentum driven asset, really.”

Gold’s sharp and sustained move higher has vexed some observers because it’s happening at a time when real yields remain elevated. That’s typically a headwind for precious metals because they don’t pay interest.

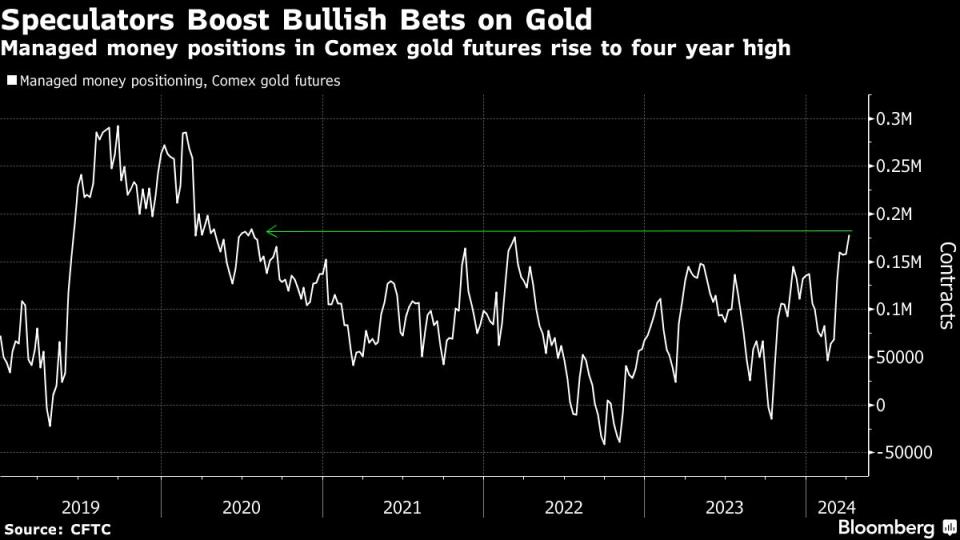

But investors have not been deterred. In New York’s Comex gold futures market, money managers are placing more bullish bets on gold, with net long positions rising to near four-year high in the week ended April 2.

One key factor has been enthusiasm among central banks, encouraging buyers like Matthew Schwab, head of investor solutions at Quantix Commodities with $933 million under management. The firm’s long-only fund has been overweight gold since 2022, with bullion’s weighting around 30% — compared with about 15% in the Bloomberg Commodity Index.

Purchases by central banks totaled more than 1,000 tons in 2022 and 2023 with much of that led by economies, particularly China, where efforts to diversify away from the dollar have accelerated.

“What I think is really, really bullish about gold is that those ounces will be taken off the market and never come back. And that’s clearly very different to the ETFs where ultimately everyone’s a trader of it.” said Duncan MacInnes, investment director at Ruffer Investment Co. He last month increased his exposure to gold and silver to roughly 8% across his two portfolios, which combined have about $3 billion under management.

There’s one further reason to expect another boost. Unusually in this environment, investor demand for gold-backed exchange traded funds — typically a key driver for bullion — has yet to materialize. In fact, total holdings are close to the lowest level since 2019, according to data compiled by Bloomberg.

According to Ben Ross, who manages about $410 million in commodities strategies at Cohen & Steers, that’s largely explained by investors chasing returns in the money market. But once the Fed actually deploys its planned rate cuts, that will eventually trigger fresh inflows into ETFs and give gold prices a further boost.

That, argues MacInnes, will create a very squeezed market.

Of course not everyone is sold on bullion’s continued run. Jay Hatfield, chief executive officer of Infrastructure Capital Advisors, has no plans to add gold in the next 12 months, opting instead for equities as central banks start to cut rates. There are small-cap stocks trading at “historic lows on a relative multiple basis” that will do much better than gold, he said.

Near term, the sudden exuberance in the market could induce a correction. Gold’s rapid ascent has lifted the 14-day relative strength index to a level that indicates prices have risen too far, too fast.

“There’s quite a bit of expectation going into the current price,” said Darwei Kung, head of commodities and portfolio manager at DWS Group. Kung is still bullish into the second half and expects more participants to increase allocations.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}