This past week, I had the pleasure of hosting a webcast on gold and gold mining stocks, and I was happy to be joined by portfolio manager Ralph Aldis. Thanks to all who participated!

Regretfully, I’m not permitted to share a replay of our discussion since it was intended for financial advisors, but there are a few key points I’d like to highlight.

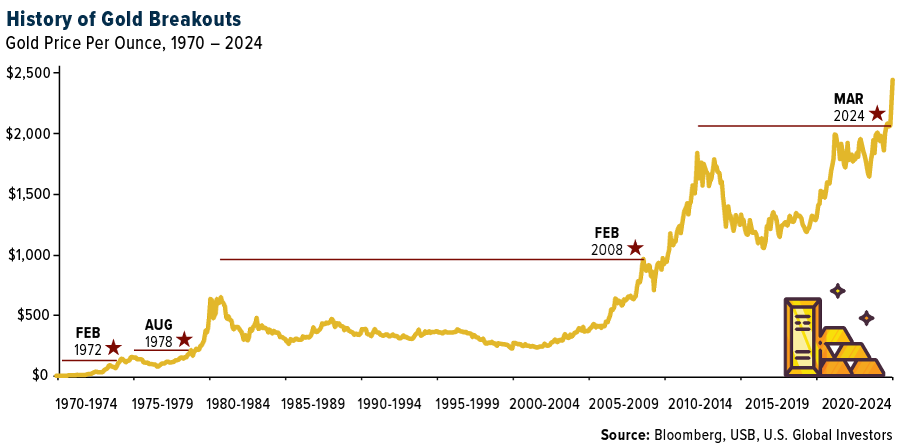

Gold hit a fresh all-time high of $2,432 per ounce last Friday, marking what Ralph and I see as one of the great gold breakouts since the end of Bretton Woods. The yellow metal’s appeal as a hedge against uncertainty, coupled with steady monthly purchases by central banks, has not merely raised the price floor but should help the asset achieve new highs in the coming weeks and months.

Preserving Purchasing Power Across Borders

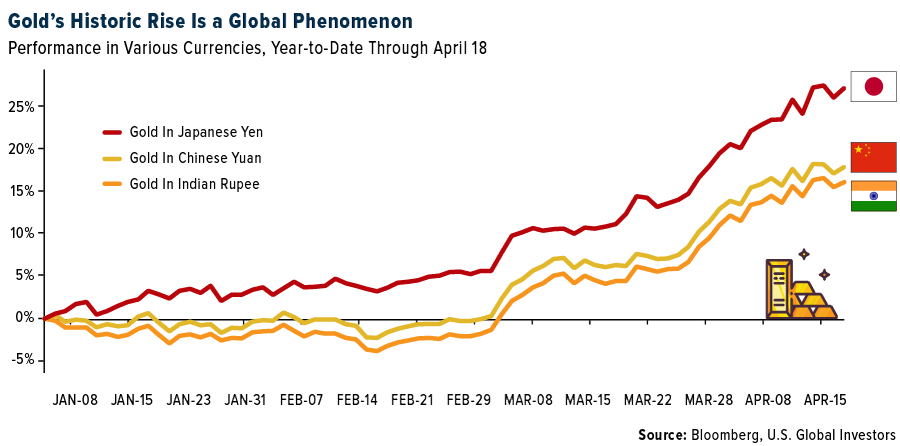

Gold’s recent surge is not just a U.S. dollar story. The precious metal is also making historic breakouts in various currencies around the world, from the Japanese yen to the Chinese yuan and Indian rupee.

This global phenomenon underscores the universal appeal of gold as a store of value and a means of preserving purchasing power.

Chinese retail investors are leading a significant influx into the country’s gold-backed ETFs. In March alone, Chinese gold ETFs saw an impressive inflow of RMB1.2 billion ($164 million), marking the fourth straight month of positive flows, according to the World Gold Council (WGC). The investing spree propelled total AUM in gold ETFs to a staggering RMB35 billion ($5 billion) by month’s end.

Historic Central Bank Demand Reshaping the Gold Market

Gold’s bull market can be attributed to several factors, including negative real interest rates, expanding government debt and the ongoing de-dollarization efforts by BRICS countries such as China and Russia. As central banks continue to print money and governments run massive deficits, investors are increasingly turning to gold as a way to protect their wealth from the erosion of fiat currencies.

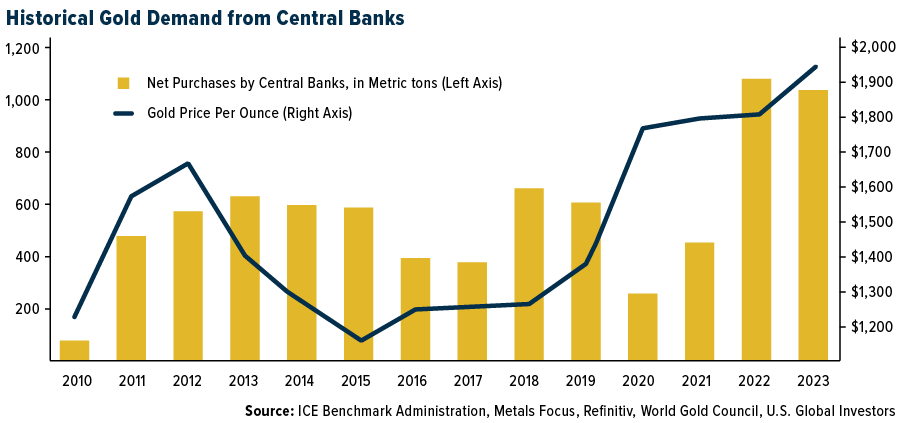

One of the most striking developments over the past several years has been the historic demand from central banks. These institutions have been accumulating gold at an unprecedented pace as they seek to reduce their dependence on the U.S. dollar and create an alternative global reserve currency. As I said during the webcast, China may need to buy the equivalent of eight years’ worth of total global gold production to rival the U.S. dollar.

Consolidation in the Gold Mining Industry

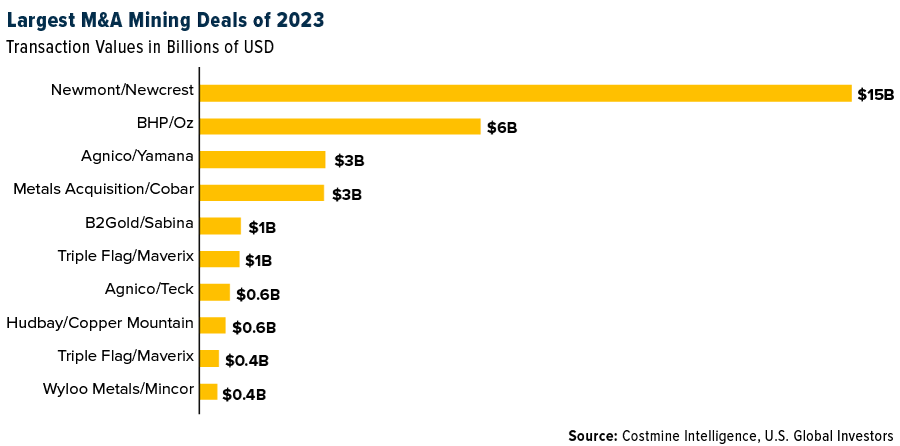

We’re seeing an incredible amount of merger and acquisition (M&A) activity in the gold mining sector.

Gold producers that are struggling to grow their reserves organically due to the lack of new, large discoveries and declining reserves at existing mines. As a result, many companies are turning to M&A as a way to expand their production and take advantage of the bullish gold market. Below are the top 10 largest mining deals of 2023, starting with Newmont’s acquisition of Newcrest for approximately $15 billion.

This consolidation is creating some exciting opportunities for investors. By owning shares in well-managed gold mining companies, investors can gain leverage to the rising gold price while also benefiting from the potential upside of successful M&A transactions.

Diversifying Portfolios with Gold and Gold-Related Investments

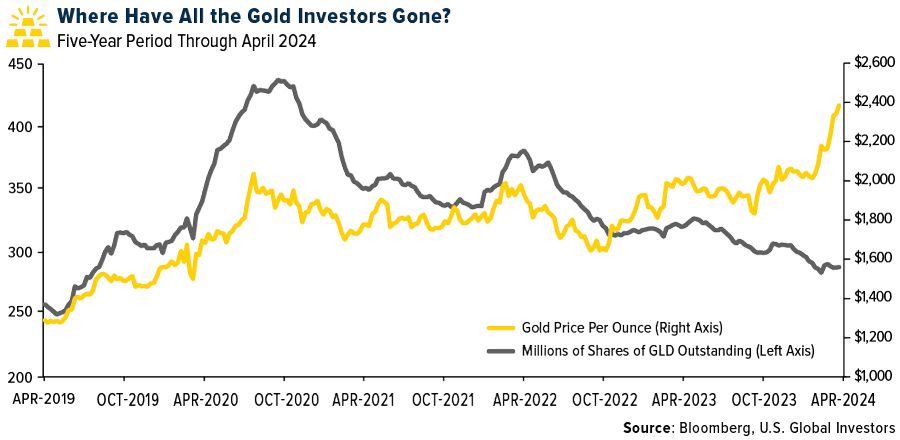

Higher prices have not necessarily resulted in greater investment in the U.S., and Ralph and I believe investors may be leaving an opportunity on the table. Even as the price of gold has crept up over the past four years, the number of shares outstanding in the SPDR Gold Shares ETF (GLD) has declined, indicating demand has a lot of catching up to do.

For investors seeking exposure to gold without the risks associated with individual mining stocks, gold royalty and streaming companies offer an attractive option. These companies provide upfront capital to gold miners in exchange for a percentage of future gold production or revenue. This business model allows royalty and streaming companies to generate high margins and strong cash flows with minimal operational risk.

Both Ralph and I believe that gold’s role as a safe-haven asset is becoming increasingly important. With central banks buying gold at historic levels, M&A activity heating up in the mining sector, and the metal making new highs in various currencies, the case for owning gold and gold-related investments has never been stronger.

Speaking of gold, I had a great interview with Proactive Investors this week which I invite you to watch. Check it out by clicking here.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.01%. The S&P 500 Stock Index fell 3.05%, while the Nasdaq Composite fell 5.52%. The Russell 2000 small capitalization index lost 2.77% this week.

- The Hang Seng Composite gained 12.19% this week; while Taiwan was down 5.83% and the KOSPI fell 3.35%.

- The 10-year Treasury bond yield rose 9 basis points to 4.622%.

Airlines and Shipping

Strengths

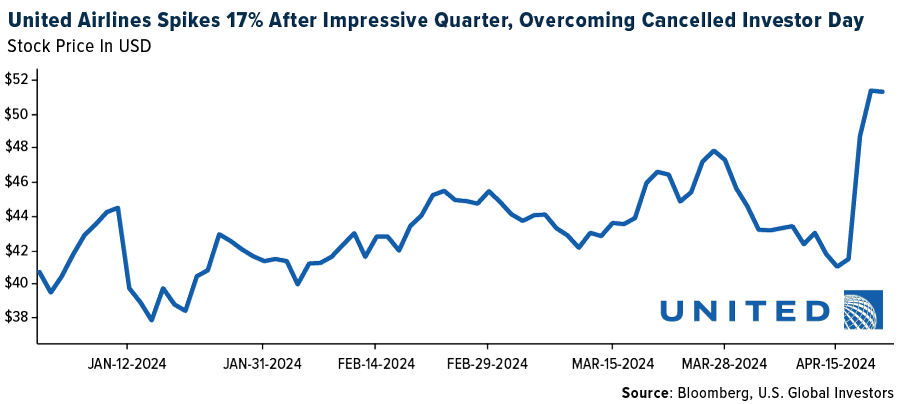

- The best performing airline stock for the week was United Airlines, up 22.4%. United Airlines was able to report earnings per share (EPS) of $(0.15), significantly better than guidance of $(0.85) -(0.35), and the Street’s $(0.57). Driving the EPS beat was strong unit revenue growth of positive 0.6% (guidance was flat), 100 basis points (bps) better than Delta Air Lines’ -0.6% despite higher capacity growth, according to Bank of America.

- According to Shipping Watch, the number of canceled sailings on the major routes from Asia to Europe and North America have dropped significantly in recent weeks. Despite the falling spot rates, shipping companies are not dropping sailings to stem the decline – they are doing the exact opposite.

- JetBlue has already restructured its West Coast footprint, will exit Baltimore in two weeks, and has announced the cessation of service to Kansas City, Stewart, New York, and four Latin destinations. JPMorgan believes affected markets speak to a high tolerance for loss production that hopefully concluded with the departure of JetBlue’s prior CEO and the ascent of Joanna Geraghty.

Weaknesses

- The worst performing airline stock for the week was Azul, down 12.5%. UBS notes that airline schedules suggest China seats into Europe are at 87% of 2019 levels in the second quarter of 2024, a sequential deterioration versus 93% in the first quarter of this year.

- The U.S. Trade Representative made a formal announcement to launch an investigation into the China shipbuilding industry. With limited details known so far, awaiting results of investigation, it will likely cover the key aspects highlighted in the petition put forward by the U.S. unions in mid-March, according to JPMorgan.

- In China, travel intentions slightly improved versus the fourth quarter of 2023, but remained lower versus the post-Covid peak level in mid-2023. Consumers’ shopping budgets for their next trip also dropped 6% year-over-year, with more pressure on outbound travel versus domestic travel, according to Morgan Stanley.

Opportunities

- United Airlines smoothed out its aircraft delivery schedule on the back of Boeing delivery and certification delays that will result in the airline taking just 61 narrowbody aircraft this year from 101 expected just a few months ago. As a result, 2024 capex was lowered to $6.5 billion from $9 billion previously, with 2025-2027 capex expected at $7-9 billion annually. United could generate more than $1 billion of free cash flow over the next three years, according to Bank of America.

- The Evercore ISI Shipping Cos. Survey increased from 74.8 to 75.3, as activity and rates remain strong for tankers and LNG ships as the impact of the longer trade routes has had a positive impact on freight rates due to the increase in ton-miles.

- Cowen believes airline loyalty and co-brand credit card programs are undervalued in the market. Delta’s AMEX SkyMiles card contributed $6.8 billion in 2023 revenue; management believes this can grow to $10 billion by 2030.

Threats

- Lufthansa’s guidance downgrade now sees fiscal year 2024 adjusted EBIT at €2.2B, 13% below company consensus, and 15% lower than previous guidance. Most of the downgrade comes from a first quarter 2024 adjusted EBIT loss at €849M, significantly below consensus expectations, driven by a larger than expected €350M negative impact from various strike actions in the quarter, reports Goldman.

- The owner of the ship that destroyed Baltimore’s Francis Scott Key Bridge has started a formal process in which companies that own goods on the stricken Dali will have to share some of the financial losses, according to the world’s leading container carrier. A.P. Moller-Maersk A/S has indicated that the process, known as “general average,” was declared by Singapore-based Grace Ocean, according to a customer advisory Friday from Geneva, Switzerland-based MSC Mediterranean Shipping Co. SA, as noted by Shipping Watch.

- Confirmation of 737-MAX deliveries from Boeing over the past few months make Ryanair’s latest expectation for 40 aircraft deliveries by the end of June look increasingly challenging, in JPMorgan’s view. The bank sees a risk that Ryanair announces a further downgrade to expectations, following the one in early March.

Luxury Goods and International Markets

Strengths

- Louis Vuitton reported organic revenue growth of 3% in the first quarter of the year, the company announced this week. In contrast, however, the previous year saw a robust 17% growth during the same period. Notably, the core fashion and leather goods division surpassed analysts’ forecasts, while the wine and spirit business recorded the most significant decline.The geopolitical and economic environment remains uncertain, the company explained.

- L’Oreal’s shares experienced an increase on Friday following the company’s report of first-quarter sales that surpassed expectations. This was driven by robust demand in North America and Europe, offsetting a decline in purchases by Chinese travelers. Estee Lauder also saw an increase in its share value, with competitors reporting favorable operating results.

- Amorepacific Corporation, a South Korean cosmetic company, was the best performing S&P Global Luxury stock. Shares gained 6.4% in the past five days after the company boosted sales for the current year.

Weaknesses

- Bloomberg reported that new car sales in the Eurozone fell by 5.2% on a year-over-year basis in March, which was the first drop this year and the biggest fall since July 2022. The data showed car registrations fell in March; the most in Germany, followed by Spain, Italy, and France.

- Tesla’s shares continue to fall. Elon Musk announced that he will cut more than 10% of the global workforce as the carmaker struggles with slower demand for electric vehicles. The move was needed to reduce costs.

- Farraday Future Intelligence was the worst performing S&P Global Luxury stock, losing 29.3% in the past five days. The EV startup could face delisting from the NASDAQ over its share price, as it dropped from more than $55 a year ago to 6 cents, as of the close of Thursday.

Opportunities

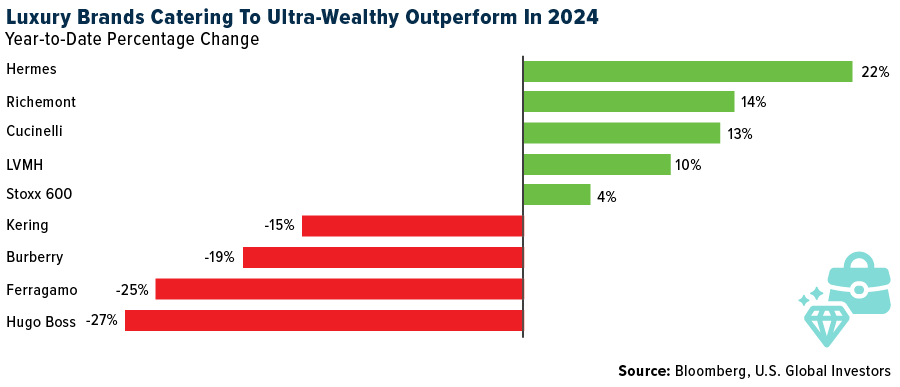

- Year-to-date, there is a noticeable divergence between luxury stocks that are performing well and those that are struggling. This performance gap is likely to persist throughout the year. According to Bank of America analyst Ashley Wallace, companies associated with high-end luxury brands are expected to maintain their robust performance. Their customer base is less affected by economic downturns and price increases.

- The luxury property market is booming in Dubai. Sales of homes with a price tag of $10 million or more climbed 19% during the first quarter, as the world’s ultra-wealthy continue to buy real estate in the region. A total of 105 luxury homes were sold for $1.73 billion in the first three months of the year, according to property consulting group Knight Frank LLP. Sales on the Palm Jumeirah accounted for 36.6% of the activity in the quarter.

- BMW is betting on China’s recovery. The Chairman of the German auto giant is confident that the country will prosper and intends to increase its investment there. China is BMW’s largest market. Last year, China sales expanded 4.2% from 2022 to 824,932 automobiles, accounting for almost one-third of BMW’s shipments.

Threats

- The Hong Kong property market remains in a state of distress, as reported by Bloomberg. In an effort to stimulate demand, some developers are slashing prices by nearly half per square foot. For instance, prices for certain units at The Corniche project have dropped from HK$45,000 to HK$25,000 ($3,200 per square foot). Despite marketing efforts beginning in January 2023, this six-tower project has only managed to sell five out of its 295 apartments.

- United States regulators are considering blocking fashion company Tapestry’s planned $8.5 billion takeover of Capri Holdings, which would prevent the formation of a U.S.-based luxury conglomerate to rival big European fashion companies. The two combined companies would be the fourth-largest luxury group globally and the second-largest in America, trailing only Louis Vuitton. Tapestry’s brands include Coach, Kate Spade, and Stuart Weitzman, while Capri Holdings owns Michael Kors, Versace, and Jimmy Choo.

- Next week, Kering, Prada, Moncler, and Hermes are set to release their sales updates. The performance of luxury stocks has varied this year, with outcomes heavily influenced by individual company strength. The upcoming results may unveil more underperforming companies than those surpassing expectations.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was aluminum, rising 6.94%, on news that the U.S. and UK have tightened sanctions on Russia, which means that metal exchanges are no longer able to accept aluminum, copper and nickel produced by Russia. The appeal of Russian metal on Western physical markets may decline though – Europe has re-directed a large part of its aluminum purchases already from Russia to the UAE and India, according to RBC.

- China’s oil processing rose to the highest level in five months on robust demand following the Lunar New Year holiday and as refiners rebuilt fuel stockpiles ahead of seasonal maintenance. The nation refined 63.78 million tons in March, up 1.3% from a year earlier, according to Bloomberg.

- Tin is at risk of a short squeeze after a price spike this month. Tin on the London Metal Exchange has risen this month and its 25% advance in 2024 puts it well ahead of more closely watched commodities like copper and crude oil. Disruptions have hit tin supply in major producers like Indonesia, Myanmar, and Democratic Republic of Congo, according to Bloomberg.

Weaknesses

- The worst performing commodity for the week was crude palm oil, dropping 6.75%, and marking a sixth consecutive day of losses. China has cut it imports of palm oil by 45%, compared to the first quarter of the prior year, as reported by Bloomberg. Following last week’s news that India intends to purchase only roughly half the volumes offered at the lowest bid price, urea prices saw sharp drops globally this week. In New Orleans, barges traded as low at $282 per ton versus mid-$300s in the prior week, according to Bank of America.

- Shale explorers are drilling wells faster than they are fracking them, a signal that U.S. oil-production growth is slowing. Oil companies added to the number of drilled-but-uncompleted wells (known as the fracklog) last month for the first time in more than a year, according to a report from the U.S. Energy Information Administration on Monday. Drillers sometimes carry an inventory of drilled but uncompleted and will only do the fracking and completion when prices are high enough to earn an economic margin.

- Chinese steel mills cut production last month in response to subdued demand due to the protracted collapse in the housing market. Output in March fell 7.8% year-on-year to 88.3 million tons, leaving the year-to-date figure 1.9% behind last year’s pace, according to the statistics bureau on Tuesday.

Opportunities

- A group of U.S. regional banks is ratcheting up lending to oil, gas, and coal clients, grabbing market share as bigger European rivals back away, writes Bloomberg. The list of banks includes Citizens Financial Group Inc., BOK Financial Corp. and Truist Securities Inc.

- With U.S. Henry Hub prices down 30% year-to-date and near multi-decade lows, supply is declining. Morgan Stanley expects prices to recover from $2 currently to over $4 in 2025 as a cycle of demand growth from LNG expansion and rising power demand tightens the market.

- With energy stocks trading near all-time highs and oil climbing as well, hedge funds think they have found a trade to capitalize: Sell the shares and pour the profits into buying more crude. Hedge funds have been selling US energy stocks for three straight weeks, according to prime brokerage data from Goldman Sachs Group Inc. The net allocation to energy is also well below historical levels, with energy now making up just 2.2% of overall U.S. net exposure on Goldman’s prime brokerage book.

Threats

- The U.S. set aside 23 million acres of Alaska’s North Slope to serve as an emergency oil supply a century ago, writes Bloomberg. Now, U.S. President Joe Biden is moving to block oil and gas development across roughly half of it. The initiative, set to be finalized within days, marks one of the most sweeping efforts yet by Biden to limit oil and gas exploration on federal lands, according to Bloomberg.

- Russia’s seaborne crude exports soared to an 11-month high in the second week of April with flows from all major ports near peak levels. Last week’s jump propelled total weekly flows to the highest since May 2023, for a level that has been exceeded only twice since the start of 2022, vessel-tracking data compiled by Bloomberg show.

- As reported by multiple media outlet, the U.S. is considering increasing the existing 7.5% average tariff rate on Chinese steel and aluminum under Section 301 of the Trade Expansion Act. These higher tariffs would apply to imports of Chinese steel and aluminum that were not subject to the existing 25% tariff on steel imports and 10% tariff on aluminum imports under former President Trump’s Section 232.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Celestia, rising 9.48%.

- Move-to-earn game Stepn announced the launch of a collaborative NFT collection with titan sportswear brand Adidas on Monday, writes Decrypt, with plans to bring Solana NFT sneakers from the brand into the fitness-focused game.

- The advent of EigenLayer restaking has opened up new yield opportunities for Ethereum holders, writes Bloomberg. A handful of protocols now provide liquid restaked ETH, juicing returns for those who know where to look. A new product from Index Coop aims to bundle those yields into an index token for easy access and built-in diversification, the article continues.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Nervos Nework, down 31.81%.

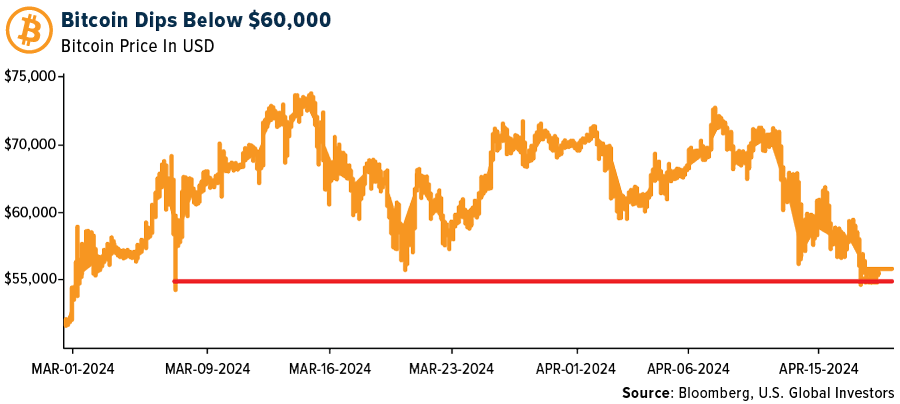

- Bitcoin briefly dropped below $60,000 for the first time in more than a month, with volatility increasing ahead of a software update in the blockchain that has long been touted as bullish for the cryptocurrency. The digital asset fell as much as 5% before paring the decline, writes Bloomberg.

- Grand Base experienced a devastating hack and a significant security breach that shocked the DeFi community. The breach occurred when a malicious actor accessed the Grand base deployer’s wallet, triggering approximately a $2 million loss, writes Bloomberg.

Opportunities

- With just a day or so to go, JPMorgan and Deutsche Bank say that the once-every-four-years Bitcoin software update called the “halving,” that has long been touted as one of the keys to propping up the cryptocurrency’s value, is pretty much priced in, writes Bloomberg.

- Binance Holdings received its long-sought full crypto license in Dubai after co-founder CZ agreed to give up voting control in the local entity. The license is a much-needed win for Binance which suffered a string of regulatory hits over the past two years, Bloomberg reports.

- A startup prime brokerage, backed by Citadel Securities, is the latest firm looking to raise new funds amid a bounce back in the digital-asset market, writes Bloomberg. Hidden road partners, which focuses on cryptocurrencies and foreign exchange, is raising a series B equity round that will bring its valuation to around $1 billion.

Threats

- A trader accused of exploiting Mango Markets rules to steal $110 million from the exchange was convicted of fraud in the first U.S. trial involving criminal charges tied to cryptocurrency manipulation, reports Bloomberg. Federal jurors in New York found Avraham Eisenberg, 28, guilty of commodities fraud, commodities manipulation, and wire fraud.

- Two senators are proposing a measure to regulate stablecoins amid a push in the House and Senate to pass such legislation as soon as next month. The bill states that they would be protecting both consumers and the U.S. dollar, writes Bloomberg.

- Anthony’s Scaramucci, the founder of SkyBridge Capital, has voiced his skepticism toward meme coins, despite their recent high returns in the first quarter of 2024. Skybridge Capital will not touch meme coins despite returns north of 1,000%, writes Bloomberg.

Defense and Cybersecurity

Strengths

- Lockheed Martin Corp. won a $17 billion contract over Northrop Grumman Corp. to develop and produce a new warhead for the U.S. missile defense systems in California and Alaska. It aims to enhance interceptor capabilities against threats like North Korea’s ballistic missiles, with plans for deployment by 2028 following the cancellation of a prior failed program.

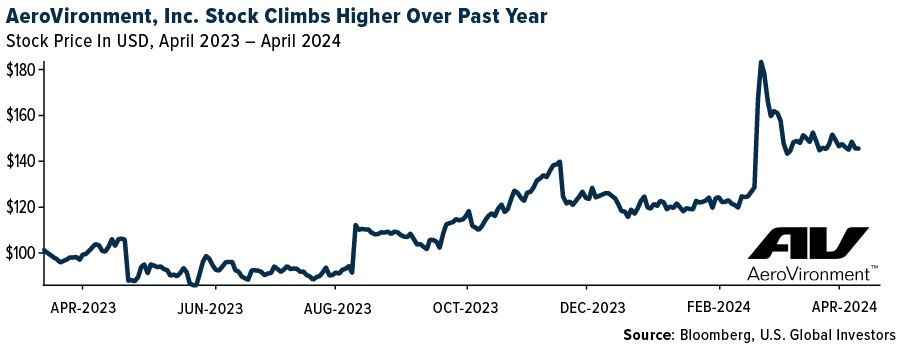

- AeroVironment’s Switchblade drones have demonstrated their effectiveness in Ukraine’s challenging electronic warfare conditions, contributing positively to the complex battlefield, (contrary to claims in a Wall Street Journal article about American drones failing in the conflict).

- The best performing stock in the XAR ETF this week was V2X, rising 7.67%. The company announced its selection as one of six prime contractors for the U.S. Nayy’s Global Contingency Services Multiple Award Contract III, valued at $2 billion.

Weaknesses

- Israel reportedly launched a retaliatory strike this week on Iran following recent attacks, with concerns about escalation and economic repercussions amid tense diplomatic efforts to contain the situation.

- The U.S., once dominant in global commercial shipbuilding, now struggles to maintain its naval supremacy. Significant production delays and rising threats from China, which has not only become the world’s largest shipbuilder but also expanded its military presence, are challenging the U.S. in the Indo-Pacific and global security.

- The worst performing stock in the XAR ETF this week was Virgin Galactic Holdings, falling 20.7%. The company’s shares declined after it proposed a reverse split of its stock.

Opportunities

- ASAP Semiconductor is now an approved supplier for Lockheed Martin, aiming to enhance operations and streamline procurement with high-quality components and comprehensive services.

- Air Force Secretary Frank Kendall, speaking at a Senate Defense Appropriations Subcommittee hearing, announced a decrease in the unit cost of the B-21 Raider bomber. This is reflective of successful price negotiations with Northrop Grumman for the fiscal year 2025 budget. Despite not disclosing specific details due to the program’s classified status, Kendall highlighted this cost reduction as a significant advancement, emphasizing the bomber’s importance in aligning with national defense priorities and securing sustainable military capabilities.

- The U.S. Space Force is collaborating with Rocket Lab and True Anomaly on a mission named Victus Haze to demonstrate countermeasures against potential on-orbit threats. It does so by simulating a chase and surveillance scenario between two satellites, showcasing rapid response capabilities and operational readiness in space.

Threats

- Russia is recruiting up to 30,000 contract soldiers monthly to bolster its invasion of Ukraine without resorting to a mass draft that could decrease public support. It is focusing instead on replacing losses and increasing troop strength to maintain military pressure despite potential strategic limits.

- Ukrainian and Western officials view Russia’s intensified bombings of Kharkiv, Ukraine’s second-largest city, as a strategic effort to make the area uninhabitable and force civilian evacuations, amidst ongoing attacks that have severely damaged residential and power infrastructure.

- Amid rising tensions, Israel’s reported strikes on Iran spark fears of nuclear conflict, with concerns heightened by Israel’s policy of strategic ambiguity and Iran’s nuclear ambitions, amplifying the risk of further escalation in the region.

Gold Market

This week gold futures closed the week at $2,403.00, up $28.90 per ounce, or 1.22%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher buy by just 0.12%. The S&P/TSX Venture Index came in off 3.52%. The U.S. Trade-Weighted Dollar rose just 0.09%.

Strengths

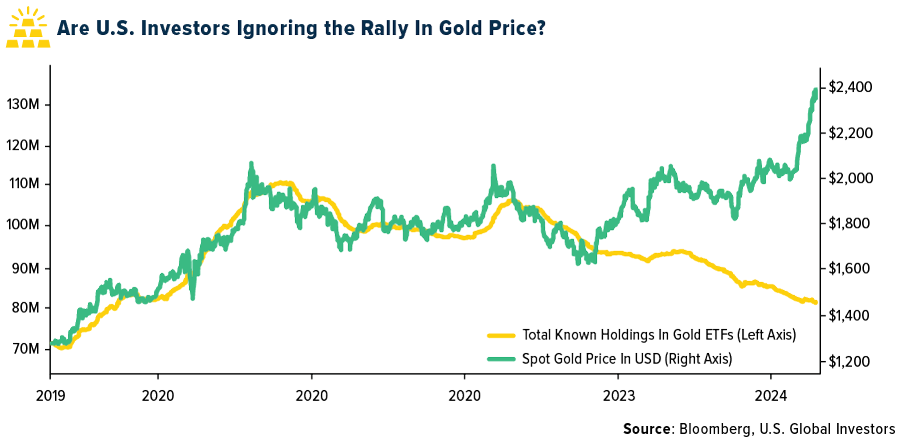

- The best performing precious metal for the week was silver, up 1.36%. The Times of India is reporting that the Reserve Bank of India (RBI) has increased its gold purchases to enhance the diversity of its foreign exchange reserves amid fluctuations in the U.S. dollar. The surge in the value of outstanding gold reserves accounted for more than 80% of the nearly $3 billion rise in forex reserves. Interestingly shown in the chart below as central bankers have steadily increased their holding in gold bullion in recent years, retail buyers of gold bullion, particularly in the West, are ignoring gold as it makes new all-time highs in prices. Wall Street recently got on the bandwagon with an even higher gold price forecast. FOMO is coming.

- Gold rose to trade near a record high, even as investors weighed a shift in messaging from Federal Reserve Chief Jerome Powell, who said the central bank will likely keep rates on hold for longer than originally planned. The precious metal is up about 15% so far this year, with gains partially driven by haven demand as geopolitical tensions in the Middle East and Ukraine continue to escalate, according to Bloomberg.

- SilverCrest Metals reported Q1 silver production of 1.41 million ounces, ahead of Scotia’s estimate of 1.20 million ounces, and gold production of 14,700 ounces, ahead of their 12,400 ounce forecast.

Weaknesses

- The worst performing precious metal for the week was platinum, down 5.69%. In terms of retail demand, ETF holdings remain subdued in the west. And, while Costco gold bar sales are making headlines, Perth Mint and the U.S. Mint sales were down by 80% and by more than 90% year-over-year, respectively in March, according to JP Morgan.

- First Majestic reported preliminary gold production for the first quarter that missed the average analyst estimate. Preliminary gold production was 35,936 ounces, versus the estimate 39,011 according to Bloomberg.

- Endeavour Mining Plc has been accused by Lilium Mining of misrepresentation over the sale of two African gold mines, as the fallout from the tenure of ousted Chief Executive Officer Sebastien de Montessus continues. Lilium made the allegations after purchasing the Wahgnion and Boungou projects in Burkina Faso last June, according to Bloomberg.

Opportunities

- Silver prices are finally catching up more stridently with gold’s rally, particularly this week, with the gold-to-silver ratio moving from 90 to around 84 currently. JPMorgan continues to think there is also more to come here. As gold continues its march higher this year and into 2025, they expect this ratio to fall towards the mid-70s. One of biggest beneficiaries of a rising silver price is Aya Gold & Silver Inc. (AYA), with most of its metal production actually being silver, Aya is one of the most exposed companies to a rising silver price. Price targets were raised this week after the company released its much-anticipated Boumadine initial resource statement.

- The sharp rise in gold prices this year could provide a nice bump to miner earnings starting in the current quarter, assuming bullion prices hold through the end of June. The gold price is now more than $300 above the fourth-quarter average, while the mining stocks — notably industry leaders Barrick Gold and Newmont — generally have performed poorly this year given the move in the metal, as noted by Barron’s.

- Gold is set to reach $3,000 an ounce over the next six to 18 months on increasing investor inflows amid expectations that the Federal Reserve will eventually cut interest rates, Citigroup said, adding to a roll call of Wall Street banks that have raised forecasts.

Threats

- Producers continue to face rising costs despite modest easing in input prices, which have been offset by persistent labor inflation. RBC estimates 8% wage growth over the past year in the mining industry, with Australia outpacing Canada/U.S. by over 2x.

- The Globe & Mail cites that Mali could be seeking to expropriate Barrick’s Loulo-Gounkoto mine, following reports on this topic by two other publications, the Africa Report and Africa Defense Forum. These reports follow prior news in 2023 that Mali was seeking to complete an audit of the mining industry and could revise its mining code.

- According to RBC, the timing of road remediation remains unclear for Gold Road Resources at the Gruyere mine, hence the timeframe of any cost and/or production impacts remains unclear. Thery have indicated Q2 will produce less gold than expected. If the haul road access remains impaired, this could bring CY24 guidance into doubt.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2024):

United Airlines

Delta Air Lines

JetBlue Airways

Boeing

Deutsche Lufthansa

AP Moeller-Maersk

Ryanair Holdings PLC

BMW

Kering

Prada

Moncler

Hermes

Tesla

LVMH

SPDR Gold Shares

BHP Group Ltd.

Agnico Eagle Mines Ltd.

Triple Flag Precious Metals Co.

SilverCrest Metals Inc.

Endeavor Mining Plc

Aya Gold & Silver Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}