The company is a bona fide market-beater with a long growth runway left ahead.

The healthcare industry demands innovation because it directly translates to better patient care. Intuitive Surgical (ISRG 1.04%) stock has won big-time because of this simple concept. Shares have appreciated more than 22,000% over their lifetime because the company’s robotic equipment has revolutionized surgery.

Intuitive Surgical is no longer a rising star, but an industry behemoth with a market capitalization of $161 billion. Given this size, it’s fair to question the company’s remaining long-term growth opportunities and whether the stock has enough investment potential to generate adequate shareholder returns.

So, is Intuitive Surgical stock a buy? Here is what you need to know.

Elevating worldwide healthcare

Humans have performed surgery for centuries, naturally making the practice ripe for technological improvement. Intuitive Surgical sells robotic systems that assist surgeons in non-invasive procedures. These robotic systems enhance human surgeons’ talents. They help surgeons minimize mistakes, improve their range of motion, and do more with smaller patient incisions. That means better procedure outcomes and faster patient recovery.

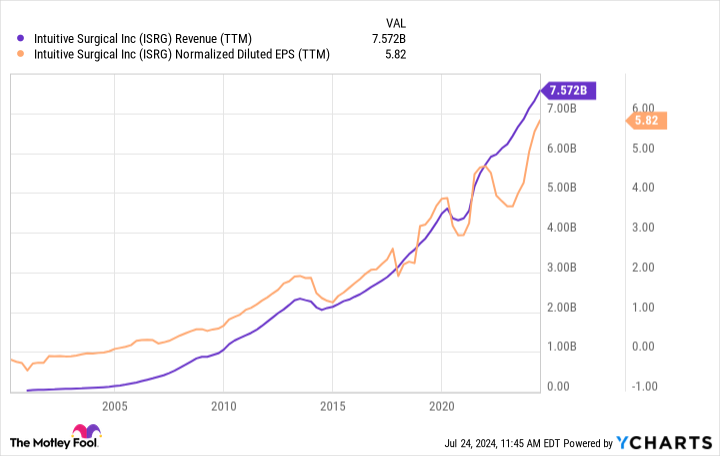

Intuitive Surgical was founded in the mid-1990s and says that over 60,000 surgeons have trained to use its flagship da Vinci system. As of second-quarter 2024, the company has over 9,800 installed systems. The install base grew 14% year over year in Q2, so there is still healthy growth momentum, as most installations are incremental or completely new rather than replacements of old systems.

ISRG Revenue (TTM) data by YCharts.

Investors should love two aspects of the business. First, these systems require maintenance. Recurring revenue streams have grown from 71% of total sales in 2016 to 83% last year. That means the business is increasingly predictable, while selling new systems fuels incremental growth and expands the install base (driving more recurring revenue). Once a hospital commits to a system, it’s doubtful that it will neglect the ongoing spending to maintain it.

Second, there are significant growth opportunities outside the U.S. There are an estimated 165,000 hospitals worldwide, most outside the United States. Intuitive Surgical already has 3,818 international systems installed, a fraction of the addressable market. Many hospitals in emerging markets may not be able to afford robotics equipment right now, but they could over the coming decades as these economies develop and mature.

But how much of this growth is already priced in?

Usually, the biggest challenge with blue chip growth stocks is that everyone knows how great they are. As a result, the market often makes investors pay up to own shares. Intuitive Surgical is no exception here.

The stock has appreciated nearly 800% over the past decade, which easily beats the broader stock market. But as you can see below, the stock’s valuation has grown increasingly hot.

ISRG PE Ratio data by YCharts.

In other words, the stock has risen faster than the business has grown. This pattern doesn’t generally last forever. Higher stock valuations create higher market expectations. The first time the company’s results can’t satisfy these increasingly lofty expectations, the stock will be prone to a painful “reset,” often involving a lower share price.

Is Intuitive Surgical stock a buy?

Analysts believe Intuitive Surgical will grow earnings by an average of 17% annually over the next three to five years. That doesn’t seem like enough growth to justify the stock’s forward price-to-earnings (P/E) of 69. I typically look for stocks trading at a price/earnings-to-growth (PEG) ratio under 1.5. Intuitive Surgical’s PEG ratio is almost 4. That’s a strong clue that the stock is expensive for its expected growth.

The company’s long-term growth trajectory looks promising, so investors should consider Intuitive Surgical a stock to target on a pullback that brings shares well below their current levels. But as I’ve hinted throughout this article, the stock is far too expensive today for investors to have much shot at seeing the company’s strong quality reflected in their investment returns.

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Intuitive Surgical. The Motley Fool has a disclosure policy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}