The unique combination of investment in mutual funds, debt market, and life insurance coverage has always attracted investors to different unit-linked insurance plans (ULIPs). These plans also help in investing for long-term goals like buying a house, retirement, or children’s higher education. Additionally, the waiver of premium (WOP) feature enables ULIPs to fulfil long-term investment goals even in case of unfortunate incidents like the untimely demise of the policyholder.

The ULIP provides the dual benefit of investment and life insurance. The premium paid to a ULIP is divided into two parts. The first part goes into life cover, whereas the other one is invested in the fund of the investor’s choice, be it equity, debt, or a combination of both. Opting for a waiver of premium rider with ULIP helps in the protection of long-term investment goals even at the time of the untimely demise of the person.

Also Read: Income tax news: How the profits on redemption of ULIP policies are taxed?

How does WOP in ULIP work?

A WOP plan ensures that a policy like ULIP doesn’t lapse in case of the policyholder’s demise. It also protects the dual benefit of ULIP, i.e. insurance and investment.

“In case of the untimely demise of the policyholder, the company will pay out life cover or fund value, whichever is higher. However, the investment part will not be continued because of the lapse of premiums that will be invested,” explained Vivek Jain, Head of Investments, Policybazaar.com.

On the other hand, a WOP feature in ULIP ensures the continuity in investment along with the payout of the life cover at the time of demise, he added.

Why a term insurance plan is never enough

There is a common perception that disapproves of mixing investment goals and life insurance coverage, making ULIPS an unfavourable option. Many advocate taking a term insurance plan along with investment in high-interest paying options like mutual funds, SIP, etc.

Partially agreeing with the opinion, Vivek Jain said, “ One should have a term cover. But, the common problem in India with term cover is that most people fail to understand that a term cover needs to take care of all their expenses. Hence, they end up buying a ₹1 crore term cover. However, a normal common earning person would at least require two or three crores of term insurance for their non-negotiable goals.”

What is the cost of taking ULIP with WOP?

Opting for the ULIP comes with different types of charges and fees, making it complex for the investor-cum-policyholder to understand the structure. Over time, there have been some changes in the charges implemented in ULIPs. The recent new-age online ULIP does not have the premium allocation and the policy admin charge anymore. “The only charges to be paid with ULIPs are FMC and the mortality charge. FMC will be there in a mutual fund also, and the additional charge that gets left in mortality, gets returned at the end of the policy terms in most ULIP schemes,” explained Jain.

Also Read: How and when should you exit from bad-performing ULIP?

Talking about the charges one needs to pay for WOP, he noted, “If the cost of a ULIP is around 1.5 per cent every year, guaranteeing a 15 per cent return, then 1.5 per cent gets invested in a normal unit. In a WOP, there will be an additional 0.5 per cent charge. So, it will be close to 1.8, 1.9 per cent. This means if a person gets a 15 per cent return, then the net return will finally come out to be around 13.1.”

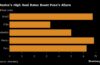

Top ULIPs with WOP with high returns

The lack of availability of WOP features in investment tools like mutual funds also makes ULIP a lucrative option to secure investment for future goals. However, the feature is available in insurance policies and certain child protection plans.

Over the past five years, many ULIPs performed way better than the industry expectations in terms of returns. Many plans have offered as high as 22 per cent interest which is higher than the 10-year average of 15 per cent return for them.

Unlock a world of Benefits! From insightful newsletters to real-time stock tracking, breaking news and a personalized newsfeed – it’s all here, just a click away! Login Now!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}