By Josh Katzowitz, WCI Content Director

By Josh Katzowitz, WCI Content Director

One of the classic investing questions that seems to have a right answer but maybe actually doesn’t is whether one should lump sum or dollar cost average a large amount of money. Dr. Jim Dahle, WCI’s founder, makes it clear what he thinks in a post from 2013 bluntly titled Dollar-Cost Averaging (DCA) Is for Wimps.

His four reasons why you should lump sum a windfall, inheritance, or rollover (throwing the entire amount of money into the market at once) instead of DCAing it (investing the money into the market a little at a time) are as follows:

- The market generally goes up.

- You miss out on the dividends for those shares that weren’t invested originally.

- It’s a hassle and opens the door to behavioral mistakes.

- You get lower expected returns.

Theoretically, I completely agree. Get your money into the market as soon as you can so it can start working for you immediately. But we as investors find ourselves in an interesting spot these days. The stock market hit an all-time high in December 2023, blasting through the 37,000 mark for the first time ever, and it has stayed in that general vicinity ever since. Meanwhile, some investors are predicting that a recession will hit the US in 2024.

How do those two factors change the lump sum vs. DCA debate, if at all? I decided to ask a few financial experts their thoughts. Here’s the scenario I presented to them.

“An investor has just rolled over a 401(k) from an old employer into the 401(k) of their current employer. It’s worth about $150,000. It’s a substantial sum of money, and since the market has been at or near its all-time high since mid-December 2023, the investor finds themself a little paralyzed about what to do. Now that the Dow is exceeding 37,000, they are worried about throwing the entire amount of money into the market, especially with the whispers of a possible recession in 2024. The stock market just went up 20% in 2023. Can we really expect anywhere close to those gains again? Plus, the investor just read an article that quoted a financial analyst who said that December 2023 was “kind of a sloppy rally” because companies were “wanting to put things on their books maybe or cover shorts.” So, that doesn’t sound great, right?

Here are the options:

-

Lump sum all $150,000 right now.

-

Dollar cost average it: invest $50,000 in January, $50,000 in February, and $50,000 in March.

-

DCA it and spread it out even more: $12,500 each month until the end of 2024″

What should this investor do?”

Lump Sum vs. Dollar Cost Averaging in 2024

I asked WCI Columnist and dentist-turned-financial-planner Tyler Scott, RFK Capital Management Founder Ryan Kelly (who recently wrote a guest post on the transition from firing your financial advisor to becoming a DIY investor), and Jim Dahle their thoughts on the matter. Here’s what they said.

That Money Was Already Invested in the Market

Dr. Tyler Scott

If it smells like market timing and walks like market timing, well then . . . it’s market timing. In the evidence-based and rational universe of this blog, we don’t believe in market timing so there is no real decision here. The money needs to be invested today. I would say that even if this was an actual windfall of new money rather than just a perceived windfall of money that was already yours, but in this case, it’s an even easier decision to go with the lump sum choice because the money was ALREADY invested in this allegedly overpriced market. So, just put your money back in the market where it was before your rollover and get on with stressing about something else in your life.

I have more nuanced empathy for someone who receives a sum of money that has not ever been invested in their own financial plan—like an inheritance, the proceeds from the sale of a home/business, an insurance payout, etc. In this case, the evidence still points to a lump sum contribution regardless of anyone’s arbitrary perception of where the stock market is today along an unknowable timeline of future performance. However, even though the lump sum is more likely to produce better long-term returns than DCA, the differences are probably not statistically significant in affecting your long-term goals (i.e. it’s not like you will be able to retire a year earlier by doing the $150,000 lump sum compared to the DCA option).

In my observation, personal finance is about 80% personal and only 20% finance. We talk about the finance side of that equation a lot and justifiably so, but the personal side doesn’t get nearly enough attention, especially relative to its impact on our real world decision making. None of us are the living embodiment of homo economicus. Rather we are all emotional creatures that are subject to a wide array of feelings that, while perhaps irrational, are nonetheless impactful on how we behave and how well we sleep at night. So, if employing a DCA strategy produces slightly suboptimal financial outcomes yet far more optimal peace-of-mind outcomes, then it’s a no-brainer to go with DCA.

More information here:

Jumping into Deep Water vs. Slowly Wading in

Ryan Kelly

I believe the most logical decision is to lump sum. There are two basic reasons for this. First, these are funds that were fully invested only very recently, and you’re only in cash because the rollover process required that previous investments be liquidated. And second, according to research from Vanguard, lump sum investing outperforms dollar cost averaging 68% of the time.

However, while the logical decision is to lump sum, it’s not necessarily the right decision for every investor. This is because successful investing requires the management of emotions. Therefore, if lump sum investing causes too much trepidation and anxiety, then DCA can be an effective way to help manage those emotions. As is the case with swimming in cold water, some prefer to jump right into the deep end, whereas others prefer to wade in gradually. One approach is not necessarily better than the other approach.

If you are an investor who prefers the DCA approach, then the key is to write down your DCA plan and stick to it. For example, if you have $100,000 to invest, then you could write down that you will invest into your target allocation in four equal installments on January 15, April 15, June 15, and August 15. If you don’t write your plan down, then you run the risk that the inevitable day-to-day fluctuations of the stock market will cause emotion to drive your entire process. You want to act and not react.

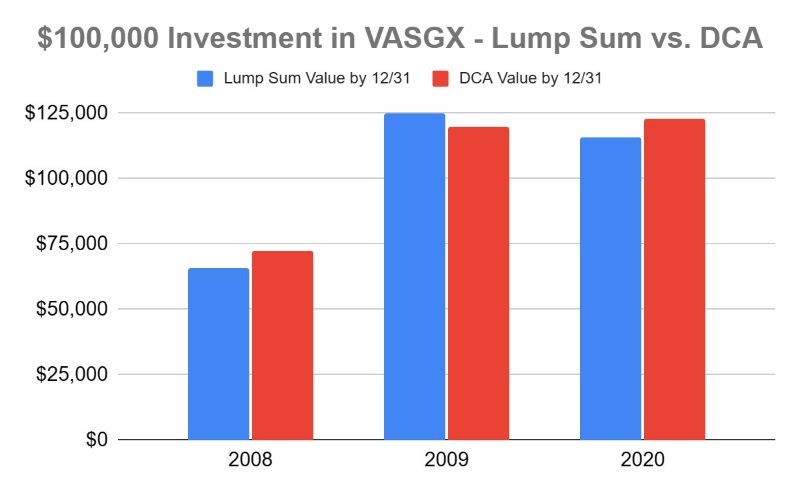

The calendar years this century with the most stock market turmoil were arguably 2008, 2009, and 2020. In 2008, the S&P 500 declined more than 40% over a three-month period. In 2009, the S&P 500 declined by 27% for the first two months of that year. I remember this time being especially scary given that it followed such a disastrous 2008 for the stock market. And in a one-month period in 2020, the S&P 500 declined by 34%.

You would think that in these calendar years that DCA did way better than lump-sum investing. That would make sense given the calendar years each included such a severe stock market decline.

However, DCA actually underperformed lump sum in 2009. And in 2008 and 2020, it didn’t really do that much better than lump sum investing. This reminds me of a point John Bogle made in one of his books that even for mutual funds that do outperform index funds over a long period, the amount of outperformance is so often quite modest.

I think a good investment benchmark to use is the Vanguard LifeStrategy Growth Fund (VASGX). It has about 50% in U.S. stocks, 30% in international stocks, and 20% in bonds. From my experience and observation, I think it’s an allocation that is pretty close to the target asset allocation of a large portion of White Coat Investor readers—especially those under the age of 50.

The chart below shows the end-of-year values (for 2008, 2009, and 2020) of a $100,000 investment in VASGX with both a lump sum approach and a DCA approach. For the DCA approach, I assume four equal installments of $25,000 on the following dates: January 1, April 1, July 1, and October 1.

My point is that even if 2024 does bring a severe stock market decline, recent market history suggests that the DCA approach may not be all that much better compared to the lump sum approach. And there’s even a decent chance that the lump sum approach would still do better than the DCA approach.

More information here:

4 Frugal Things I’ve Done Lately

The Stock Market Is Usually at All-Time Highs Anyway

Dr. Jim Dahle

There are few on the internet who feel as strongly as I do about this question. My article on this subject, written many years ago, is titled DCA is for Wimps, and I still believe that. While DCAing a lump sum over a few months or even a few years does occasionally outperform investing the lump sum as soon as you get it, that’s not the way to bet, even at “all-time highs.” What most people don’t realize until they look at a long-term stock market chart is that the stock market is usually at or near all-time highs.

Check out this chart from StockCharts that shows the Dow Jones Industrial Average from 1900 to the present to see what I mean (click the image to enlarge it).

Besides, your money will be fully exposed to the market as soon as you finish DCAing. If you can’t emotionally handle that now, why would you somehow magically be able to handle that in three months or 12 months? Maybe you should dial back your asset allocation to something where your fear of missing out precisely equals your fear of loss.

Invest the lump sum, quit worrying about it, and go spend your time doing something more worthwhile.

More information here:

Some Sobering (and Scary) Statistics on People’s Retirement Preparedness

After reading those opinions, the investor said they felt better about the decision and immediately invested the money. It’s probably the right move, but even if not, it’s a decision the investor doesn’t have to think about again—and that’s valuable too.

Money Song of the Week

I’ve always enjoyed songs that fight against The Man, whether it’s Rage Against the Machine railing against corporate greed or Taylor Swift eviscerating the patriarchy. Today, let’s look at Ben Harper’s “Excuse Me Mr.,” which takes a more chilled-out approach to putting a fist up in the air and which also briefly extolls the benefit of giving to charity.

As he sings,

“See, ’cause Mr., when you’re rattling on heaven’s gate/By then it is too late/’Cause Mr., when you get there, they don’t ask what you saved/All they’ll wanna know, Mr., is what you gave.

So excuse me Mr., but I’m a Mr. too/And you’re giving Mr. a bad name, Mr. like you/So I’m taking the Mr. from out in front of your name/ ‘Cause it’s the Mr. like you that puts the rest of us to shame.”

Some of the best live shows I saw in college were with Ben Harper and his band The Innocent Criminals. Also, take note in the live video below of bassist Juan Nelson, who I met after a show once in the early 2000s. He was a jovial character and one heck of a bass player (sadly, he died in 2021).

I loved Harper’s playing and the way he performs live. I was never wild about his lyrics – I thought they were a little too simplistic – but I never thought about it from this perspective until reading this piece on dropd.com in which Harper talked about why some of his work isn’t meant to be complex.

As the author wrote:

“Harper’s beliefs are deeply entrenched in his music. The roots of social and political comment percolate over the sparse melodies. What separates Harper from countless other singer/songwriters is an emotional intensity and a lyrical intelligence that speak directly to the heart without any excess baggage. The stark images and concise writing harken back to the ghosts of Bob Marley and Hank Williams Sr. The literary teeth of such songs as ‘Oppression,’ ‘God Fearing Man,’ and ‘Excuse Me Mr.’ bear witness to modern day injustices and evils, yet follow in the footsteps of gospel and dust bowl folk with their universal messages.

“‘I grew up listening to spiritual music, Blind Willie Johnson and folk,’ [Harper said]. ‘Folk is bare bones music. You can’t be too clever with it because it’s the people’s music. It’s the blood in the veins of the common man.’”

Tweet of the Week

I’m not sure whether this tweet is saying that those in the financial industry are paid less than we assume or just that they’re really practical with their automobile purchases, but it’s interesting nonetheless. No Lambos or Ferraris anywhere in sight, which speaks to WCI’s philosophy of getting rich by driving a cheaper car.

So this unnamed financial services company I work for has an automobile purchasing program and lists the top purchased models by employees in 2023, no surprise it reads like a @JLCollinsNH post.

Honda CR-V

Mazda CX-5

Toyota RAV4

Honda Civic— William Knowles (@c4i) December 27, 2023

How have you handled large windfalls or rollovers? Would you rather lump sum invest it or DCA it? Does the stock market at all-time highs give you pause? Comment below!

[Editor’s Note: For comments, complaints, suggestions, or plaudits, email Josh Katzowitz at [email protected].]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}