146th Edition: April 2026

Key Points:

- Post-Eid prices stay high, margins crushed.

- Zero tariff proposal draws fierce industry opposition.

- SAT-1 FMD threat tightens Thai cattle border.

- Australia dominates beef imports, US trade deal looms.

Regional Trends and Overview

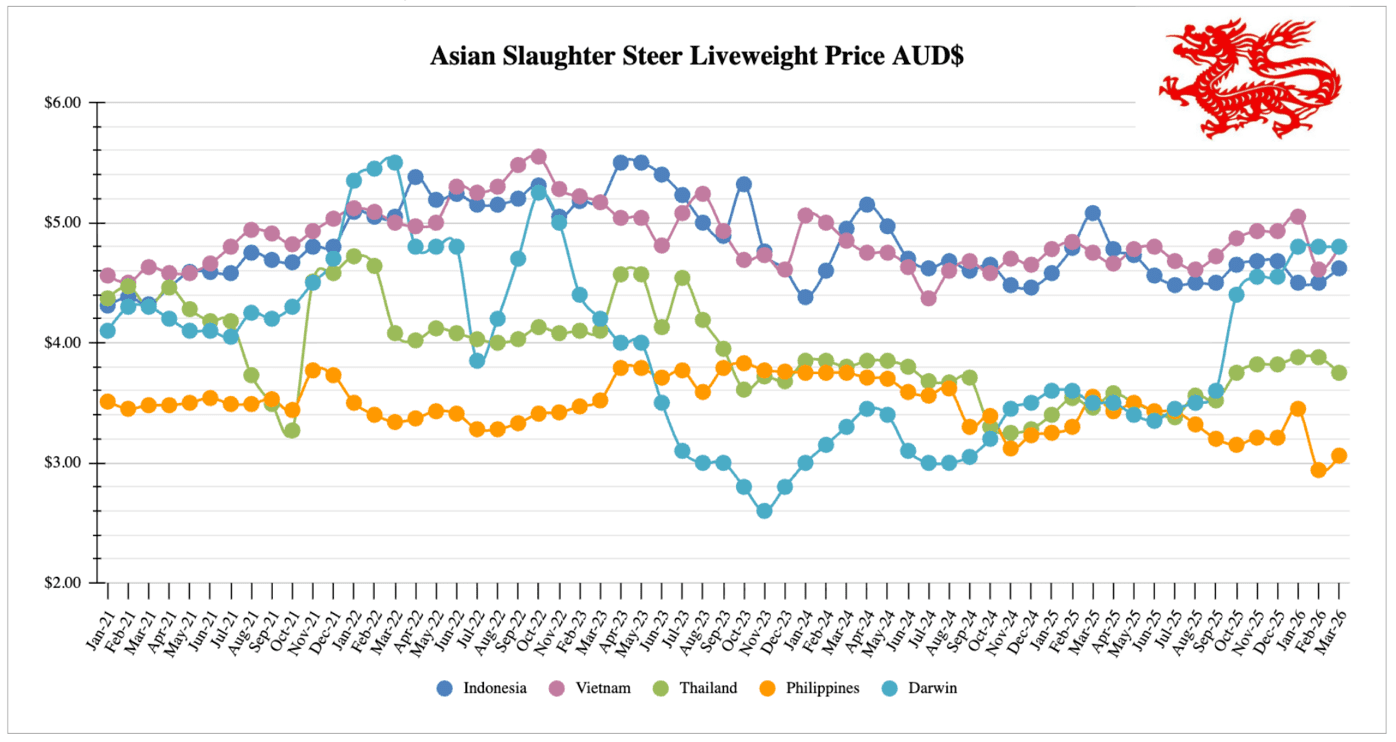

Regional Price Graph

Indonesia: Slaughter Steers $4.87 AUD per kg live weight (IDR 12,000 = $1 AUD)

Prices

Prices continue to move in one direction.

Dr Michael Patching

Lampung slaughter steers are at IDR 58,500 per kg (AUD 4.87), Java at IDR 60,750 (AUD 5.06).

At retail, wet market beef knuckle is running IDR 140,000 per kg (AUD 11.67) and supermarket knuckle around IDR 158,000 (AUD 13.17).

Chicken sits at IDR 38,000 (AUD 3.17), and that gap between beef and chicken keeps widening in ways that will eventually shift how Indonesian households buy protein.

Post-Eid Beef Prices Fail to Ease

The story out of Indonesia is that prices simply did not fall after Eid al-Fitr this year. Normally we see a 5 to 15 percent correction once festival demand fades, but wet market prices have held at IDR 140,000 to 150,000 per kilogram, which tells me this market is structurally short rather than just seasonally tight. Local cattle numbers are low, import activity has been slower than usual, and feedlotters are getting squeezed from every direction.

The government’s reference price system is a big part of the problem. Feedlot cattle are still expected to trade near IDR 55,000 per kilogram liveweight despite costs running well above that, which limits retail price increases but also kills the incentive to import and makes restocking even harder.

The government’s reference price system is a big part of the problem. Feedlot cattle are still expected to trade near IDR 55,000 per kilogram liveweight despite costs running well above that, which limits retail price increases but also kills the incentive to import and makes restocking even harder.

Then there is the rupiah. The IDR has fallen roughly 9 to 10 percent against the AUD year-to-date, sitting around IDR 12,000 to 12,300 per dollar, with USD/IDR at approximately 17,100.

What makes this particularly painful is that cattle are bought in AUD, freight is priced in USD, and feed ingredients trade in USD, but every price control in the Indonesian system is fixed in rupiah. The feedlot reference price, the retail beef reference price, the margins available to butchers and meat traders, all of it denominated in a currency that keeps losing value. As the IDR weakens, the cost of bringing cattle into the system rises in foreign currency terms while the rupiah ceiling at the other end stays put. Feedlotters cannot pass the loss through because the price controls will not allow it. Butchers are in the same position. The currency move quietly erodes margins at every point in the chain, and no single participant can adjust their way out of it.

Thailand: Slaughter Steers $4.68 AUD per kg live weight (THB 23 = $1 AUD)

US Trade Framework Poses Longer-Term Risk to Australian Market Position

The longer-term watch item for Thailand is the US-Thailand reciprocal trade framework agreed in October 2025. Negotiations are ongoing, but the US has committed Thailand to accelerating access for FSIS-certified meat and poultry and addressing non-tariff barriers. The US currently sits at a 50 percent tariff disadvantage against Australia’s zero rate under the Thailand-Australia FTA, which explains why the US holds only around 3 percent of Thai beef imports by value. Thai cattle industry groups have lobbied hard against any opening to US beef, citing the damage Australian FTA access has already done to domestic producers, and I have some sympathy for that position. But the framework is moving, and if the US closes the tariff gap it would be the first real competitive pressure on Australia’s position in this market in years.

Vietnam: Slaughter Steers $4.80 AUD per kg live weight (VND 18,263 = $1 AUD)

Ambitious Export Targets, Tough Reality for Beef

The Vietnamese government has been promoting its US$1 billion livestock product export target for 2027. Total meat production has risen from 6.85 million tonnes in 2021 to 8.66 million tonnes in 2025, and exports surged 84 percent year on year in the first two months of 2026 to around US$141 million, though most of that growth is pork and poultry. Per capita beef consumption sits flat at around 6.3 kilograms, a trend fairly common across the region where beef struggles to compete against the far cheaper proteins of poultry and pork. The policy push toward disease-free zones, better breeding and deeper processing is the right direction, but Vietnam still needs Australian cattle to fill its supply gap and I think that dependence persists for some time yet.

I was in Vietnam this month and the conversations I had around beef confirmed what the numbers suggest. Conditions are tough for local production and consumption. There are some genuine success stories in high-end retail and foodservice, but for Australian beef in the wet market it has been difficult for several years now. Competing against Indian buffalo meat on price is a losing battle, and at the same time abattoirs are facing rising costs as pressure mounts to meet higher food safety and sanitary requirements. Both forces are squeezing the same operators from opposite ends.

The government restructure continues to have its impact in Vietnam. To date there have been a total estimated job impact of ~100,000 roles affected, including layoffs, early retirement, reassignment. 80,000 of these have been public sector jobs. The 63 Provinces are now down to 34. And a complete structural overhaul of government with District level abolished entirely (3-tier to a 2-tier system) and Commune level units reduced by ~60–70%. This is obviously a huge and important overhaul of the Vietnamese system and will result in significant decreases in costs, better planning, administrative simplification, and stronger central control. There are still significant implementation issues that they face in their execution including clarity on administrative roles. My own experience was that I was directed to 3 different offices to hand in complete a simple form, which now needs to be sent to someone else in Hanoi. I am sure that there will be ongoing disruption in the short term, but in true Vietnamese fashion I am sure they will make it work and prosper even more within a more streamlined system.

New SAT-1 Foot-and-Mouth Strain Adding Pressure on Thai Cattle Imports

The Vietnamese Ministry of Agriculture and Environment is watching a new disease threat closely right now. SAT-1, a strain of foot-and-mouth disease never previously recorded in Vietnam, has prompted urgent meetings and a push to get diagnostic kits deployed at border crossings. Adult cattle and buffalo mortality runs at 5 to 10 percent under normal conditions and can go higher in poor herd health situations, and authorities claim the impact on pigs is significantly worse. The source of the concern is Thailand, where SAT-1 has been circulating, and Thailand is a meaningful supplier of cattle into Vietnam through informal border crossings through Cambodia and Laos. Tighter biosecurity controls will add friction and cost to a pathway that is already complicated enough. Worth watching how seriously this gets enforced on the ground, because the announcement from Hanoi and what actually happens at the border can be very different things. Either way it could be an opportunity for Australia’s disease-free live cattle trade.

Photos: Thai cattle typical of those moved cross-border into Vietnam

Philippines: Slaughter Steers $3.00 AUD per kg Live weight (₱42 = $1 AUD)

Prices

Prices are broadly steady. Wet market beef knuckle at ₱360 per kg (AUD 8.56), supermarket knuckle at ₱415 (AUD 9.87), steer prices edging up to ₱126 (AUD 3.00), pork carcass at ₱245 (AUD 5.83), and broilers at ₱170 (AUD 4.04) with branded product around ₱247 (AUD 5.87).

Photos: Local meat and livestock sales in Mindanao

Meat Imports Continue to Rise as Local Producers Call for Higher Tariffs

The Marcos administration is floating zero tariffs on pork, chicken and corn imports. January meat imports were already up 4.2 percent year on year to almost 144 million kilograms with chicken up nearly 9 percent, so the timing is politically interesting. On 12 April a coalition of 17 agricultural groups led by SINAG wrote to President Marcos calling the proposal a “stab in the back”. Their argument is that Brazilian pork is already landing at USD 1.60 to 2.50 per kilogram, well below domestic production costs, chicken liveweight prices have fallen to around ₱82 against a breakeven of ₱100 to ₱110, and the farmgate-to-retail gap for pork and chicken is already running at 90 to 120 percent. ProPork wants a 500,000 tonne import cap and targeted subsidies for transport and feed costs instead. The evidence that previous tariff cuts reduced retail prices is thin at best, so the producers have a reasonable case. The cattle sector is equally concerned because when competing proteins get even cheaper, beef typically loses consumers. This is another example of a common theme across the region where we see politicians looking to the cheap proteins to alleviate cost-of-living pressures, with beef being left behind as a structurally more expensive protein to produce.

Photos: Local pork meat section in the Philippines

Australia: Feeder Steers Darwin $4.50

Darwin feeder prices have pulled back from the $4.80 per kilogram liveweight highs of the first quarter to around $4.50. Exporters are marking down their expectations for Indonesia this year and the headwinds are the same ones I have been writing about for a while now. Australian cattle prices above Indonesia’s feedlot reference price, a rupiah down 9 to 10 percent year-to-date, and freight costs increasing. The wet season is also still limiting Top End road and yard access, forcing some exporters to source further south.

Bunker fuel is worth a mention given what has happened since January. The Ship and Bunker Global 20 Ports Average for IFO380 has gone from around USD 464 per tonne at the start of the year to USD 957 by early April, roughly doubling on the back of the Iran conflict. Fuel is one of the biggest operating costs for livestock vessels, and those increases will flow through to freight rates as contracts roll over. The Darwin to Indonesia run is short enough to limit exposure somewhat, but it is still real cost pressure landing on a trade where the margins are already thin and Indonesia’s feedlot economics are already under strain.

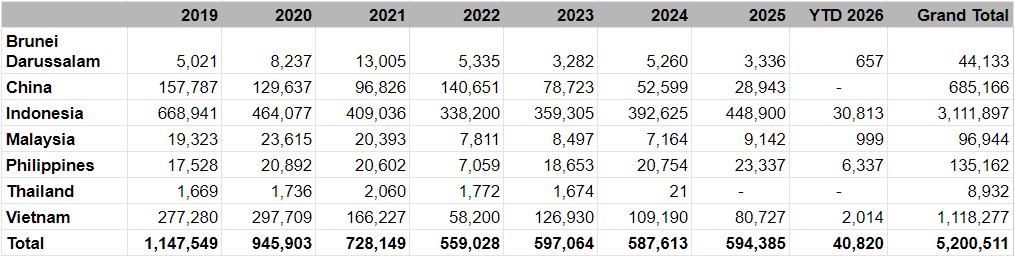

Year 2026 cattle exports – comparison across SE Asian markets

Source: DAFF website

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}