Chelsea and big numbers. A tale as old as, well, at least 23 years.

When Russia invaded Ukraine four years ago, Roman Abramovich’s proximity to Vladimir Putin and the Russian war effort resulted in Chelsea’s then owner being sanctioned, his assets frozen and the club marooned. Without the backing of the man whose funds had fuelled them since 2003, Chelsea could not sell tickets or merchandise, or take part in football’s bustling transfer market. Cash flow became a heightened concern.

Not so since. Abramovich was replaced by a private equity-backed consortium, BlueCo, who, alongside paying £2.35billion ($2.97bn) in cash for the club and £49.8m ($63m) to former Chelsea directors for their roles in facilitating the sale, also committed to investing a further £1.7bn ($2.1bn) into the club.

Four seasons of new ownership have seen almost £2billion ($2.7bn) spent on new signings as BlueCo undertake the most aggressive player-trading strategy in football. Financial regulations have been skirted at home and breached abroad. A second club, Strasbourg, have been added to the group. Players and coaches have been ferried between the two clubs at pace.

Despite the largesse, the adoration Abramovich still enjoys among some Chelsea supporters is sorely lacking for BlueCo. Before Saturday’s 1-0 home defeat to Manchester United, the first time Chelsea have lost four straight games without scoring in 28 years, hundreds of fans gathered near Stamford Bridge to protest the ownership, singing “Get out of our club”.

Fans protest against BlueCo outside Stamford Bridge on Saturday (Photo: John Walton/PA Images via Getty Images)

That defeat has left Chelsea seven points shy of a guaranteed Champions League spot with five Premier League games remaining. Failing to qualify for that competition would mark the third time in four years under BlueCo its riches have gone begging. Record player sales last summer translated to much lower profits. Chelsea shirts have become more familiar without sponsors than with; commercial revenues lag rivals.

All of this is set against the backdrop of BlueCo’s mammoth bet on football.

The over £4billion committed to the project has been added to with borrowings that don’t show on Chelsea’s books, accruing interest at significant rates. The fate of the club’s home ground, an impediment to higher earnings, has caused rifts within the consortium; no decision on its future has yet been made.

And next month marks the fourth anniversary of the arrival of an ownership group who need Chelsea to be worth a lot of money if they are to make a success of the most brazen deployment of private equity strategy football has ever seen.

Will it work?

Four years of BlueCo has brought four years of headlines and, more often than not, the story hasn’t been on the pitch. Where years one and two were marked by club assets being ‘sold’ to fellow group companies — two hotels and a car park in 2022-23, the women’s team in 2023-24 — to avoid breaching Premier League profitability and sustainability rules (PSR), year three brought the biggest financial loss in English football history. Chelsea FC Holdings Limited, which houses the club’s men’s team, posted a pre-tax deficit of £262.4million last season.

The story, and the deficits, run deeper. Chelsea’s loss was even larger in submissions to UEFA, which requires clubs to adjust for various industry rules and, pertinently for Chelsea and BlueCo, demands clubs adhere to a ‘reporting perimeter’. This seeks to capture all of the activities of running a club, even if costs don’t necessarily appear in a club’s standalone financial statements.

Those factors pushed Chelsea’s UEFA-reported loss up to £342million, and the loss at 22 Holdco Limited, the uppermost UK-registered company in the BlueCo group, was even more stark: £700.8m. In its first 38 months of existence, losses at 22 Holdco were £1.852billion.

That is a staggering sum by any measure, though there are some accounting quirks to consider. One is the premium paid by BlueCo to acquire Chelsea, being the £1.049billion excess, or ‘goodwill’, spent over the value of the club’s net assets in May 2022. BlueCo is expensing, or amortising, that sum over 10 years, meaning 22 Holdco’s accounts includes a £104.9m goodwill amortisation charge every year until 2032.

Yet even accepting that, the losses in the company heading the project are enormous, reflecting huge spending from the moment BlueCo arrived. Most of that has gone on Chelsea, where cash requirements have outstripped everyone else in football and the club’s own hefty shareholder funding under Abramovich. In the past three seasons, the club’s free cash flow — cash generated after covering operating costs and capital spending, such as that on transfers — was £1.131billion in the red.

Naturally, someone needs to actually cough up that money.

Discerning the precise funding of BlueCo, and by extension Chelsea and Strasbourg, is akin to unravelling the Gordian Knot. Private equity is aptly named.

The club’s owners, those investing the funds on behalf of others, are well known. Through 22 Holdco, Chelsea are owned by a combination of Blues Investment Midco, L.P., an investment vehicle owned by Clearlake Capital Group and headed by Behdad Eghbali and Jose Feliciano, and Blueco 22 Holdings L.P., a separate group led by Todd Boehly.

Clearlake owns a majority stake of 61.8 per cent (up slightly from 61.5 per cent at the point of the takeover) and to the end of June 2025 had injected £1.794billion of cash into 22 Holdco as equity. The Boehly-led group has provided £1.106bn, taking total equity funding into 22 Holdco in its first three years of operation to £2.9bn. In the event of a future sale where the group loses money on its investment, it is Clearlake which has downside risk protection. The Boehly-led group absorbs the losses first.

The bulk of that equity was provided back in May 2022 to fund the initial purchase of Chelsea, with the group reliant on debt funding (which we’ll come to) to fund activity in the interim.

That changed last season. Four separate tranches of equity funding arrived into 22 Holdco from Chelsea’s owners during 2024-25: £190million in September and October 2024, £80m in November, £65m in February 2025 and a further £115m in March, for a total of £450m in just seven months. Of that, £330m found its way into Chelsea coffers.

As to where the BlueCo operation sits in majority owner Clearlake’s sprawling portfolio, a company missive in September 2022 identified Clearlake Opportunities III (COP III) as having ‘led the Chelsea Football Club investment on behalf of Clearlake’s affiliated funds and other partners’.

That’s curious in a couple of ways. For one, COP III is a private credit rather than equity fund, one which, according to a public investment memorandum released by the state of Pennsylvania’s Public School Employees’ Retirement System (PSERS have invested in COP III), aims to provide returns ‘by investing in non-control special situations investments’. It would be hard to argue Clearlake’s majority shareholding position in West London is one of ‘non-control’.

Second, COP III raised a little over $2.5billion (£2.2bn at the date the fundraising closed), or less than Clearlake’s share of the £4.2bn committed to the Chelsea project upon acquisition.

Clearlake said COP III led the investment on behalf of affiliated funds and other partners, and disclosures in the accounts of 22 Holdco appear to confirm involvement of one of Clearlake’s flagship private equity funds. Eight of those have been opened since the firm was formed in 2006, and the seventh (VII) closed in May 2022 with over $14.1billion (£11.4bn) in commitments from investors.

The VII fund provided, in conjunction with the Boehly-led group, a £100million loan to 22 Holdco in 2023-24. The loan was repaid in full, but there’s evidently been involvement from Clearlake funds besides COP III, not least because the latter’s total fundraising didn’t meet the level committed to the Chelsea project, as well as the fact COP III has other investments beyond football.

One source with knowledge of BlueCo’s dealings, speaking anonymously like others in this article to discuss private business matters, told The Athletic that the £4.24billion originally earmarked for the Chelsea project was fully reserved. Cash beyond the equity provided so far by the owners remains in place.

Importantly, The Athletic has been told that the £1.7billion post-takeover commitment has already been met, reflecting how more than that has flowed into 22 Holdco in the first three years. That commitment is deemed met even as £1.3bn of it came via debt held in Chelsea’s parent companies rather than as equity. Even as the group has the funds to, and almost certainly will put more money in, there is no obligation for BlueCo to provide more equity funding than has already been committed.

That totals the £2.9bn previously mentioned, meaning a further £1.3bn could yet be utilised. That was, of course, only to the end of last June. More has gone in since; 22 Holdco’s accounts confirmed that ‘in both the base case and reasonably possible downsides’, more funding would be required from the ownership in 2025-26, and not just to cover ongoing operations. Per those accounts: “The most significant factor that determines the extent of the financial support requirement [from the ownership group] is the net impact of future player transfer activity.” Chelsea don’t disclose transfer debts, but The Athletic estimates their net payables to other clubs sat above £200m in June 2025 even with a decline last season.

That should quell any concerns observers may have about the group’s, or Chelsea’s, liquidity. But it’s not like that £4.2billion can be used up with no consequence. Unlike benefactor owners elsewhere in English football, BlueCo has invested the funds of others, and so needs to generate a return. Given the sums already involved, that return will need to be substantially above the initial cost of buying Chelsea.

BlueCo’s equity investment to date differs from the overall project funding because of one simple reason: the group has taken on huge levels of debt to fund its activity. At the end of June 2025, debt in 22 Holdco was £1.390billion. Not all of that has been used to fund Chelsea, but if 22 Holdco was a single football club it would be the most indebted on the planet.

BlueCo has converted all of its funding to Chelsea into shares, meaning the club was debt-free at the end of June 2025, even as £1.4billion sat higher up the chain. Moreover, and crucially, Chelsea have borne no interest costs under their current owners — despite the huge level of funding provided. The club’s enormous losses have arisen even as they’ve received all of their funding interest-free.

Further up the chain, interest is anything but free.

That £1.4billion in debt is split into two facilities, the most senior of which comprises £800m in revolving credit loans held by Blueco 22 Limited, the company below 22 Holdco in the corporate chain. Those loans accrue interest annually at a 3.25 per cent plus SONIA, the primary interest rate benchmark in England. That fluctuates daily, but currently sits at 3.73 per cent.

Apply those fixed and floating rates to £800million and you wind up at an annual interest charge of nearly £56m on Blueco 22’s debt. In all, across interest and transaction costs, the loan cost the group £143.5m cash in three years to the end of last season.

Blueco 22’s facility is short-term, due for repayment in July 2027. People with knowledge of the group’s dealings have told The Athletic that the £800million facility has already been renewed at the same level of borrowing, apparently with a lower rate of interest attached. Whether that means the fixed portion of the interest has been lowered or is simply reflective of broader falling interest rates is unclear.

No documentary proof of the refinancing terms is yet available. The debt in Blueco 22 may now be held on more favourable terms, and we’ll see in future accounts if it is.

Some of the messages around the club’s modern finances have yet to translate to hard evidence, such as suggestions of a falling wage bill, talk of record player sales which does not mention them translating to paltry profits, and the claim the club is profitable at the operating level even as it posts day-to-day deficits never before seen in English football.

Either way, at £800million in borrowings, its service costs will remain significant.

Of even greater intrigue is a smaller facility that BlueCo has yet to pay anything back on.

In late 2023, 22 Holdco Limited entered into a £500million loan agreement with Ares Management, repayable in August 2033. The group drew down an initial £367million, a further £16m in April 2024 and the remaining £117m in August that year. The loan was reportedly taken out to fund works at Stamford Bridge and the acquisition of further clubs. Strasbourg were bought prior to the loan’s first drawdown.

While the Ares loan may look the less cumbersome of the group’s two facilities on face value, its terms change that view drastically.

The 10-year, £500million facility is structured as a payment-in-kind (PIK) debt, whereby 22 Holdco pays no cash interest until the principal amount falls due in August 2033. Instead, the PIK interest is added to that principal amount, compounding each year until maturity.

That compounding effectively means interest is built on top of interest, and in the case of this particular loan, the annual interest rate is hefty: 7.5 per cent plus SONIA.

At current rates, that works out at 11.23 per cent, which is actually an improvement; at the end of 2023, higher SONIA rates meant PIK interest was accruing at 12.96 per cent.

The effect of such a high interest rate compounding year-on-year is significant, even if rates continue to reduce. Filings from Ares confirm the loan has an interest rate floor. To the end of June 2025, £109million in PIK costs had already been accrued. At an assumed SONIA rate equal to today, by the time the loan falls due for repayment in late 2033 PIK interest will have built to £926m. In all, 22 Holdco will be on the hook for over £1.4billion, almost triple the amount originally borrowed.

Naturally, that’s based on assumptions over a seven-year period in which much could change. BlueCo could choose to pay down the debt, currently at £609million, inclusive of the accrued interest, using some of their reserved equity funding.

Alternatively, sources have advised The Athletic the PIK interest can be paid in cash instead of accruing, ideally from the group generating sufficient cash flows. Doing so would leave the principal to be repaid upon maturity but would stop the overall liability swelling to the total forecast above.

At present, BlueCo’s PIKs don’t impact the group’s cash flow, which is just as well given the already extraordinary funding required to underwrite what we’ve seen at Stamford Bridge in the past four years. 22 Holdco’s losses include the impact of the PIKs — net interest costs totalled £138.6million last season — but in cash terms, there’s been no payment on top of the hefty Blueco 22 interest.

Yet come 2033, the bill on the PIK debt will fall due. What happens then is difficult to determine from here, but if Chelsea’s value has not increased substantially by that point, issues are easy to foresee.

Repayment of the loan from the group’s own cash generation would require a turnaround which, from here, looks improbable. Alternative means would be raising further funds from investors or through selling up, and any appetite for either is linked to Chelsea’s value. Likewise, refinancing the debt; if the BlueCo project isn’t creating value, lenders — be they Ares or otherwise — are hardly likely to provide more favourable terms than those currently in place.

The £800million debt in Blueco 22 comprises the group’s senior debt, meaning it has to be repaid first in the event of insolvency. The huge interest on the £500m Ares-originated debt reflects the fact those borrowings are lower in the pecking order, and the nature of Ares’ business means there’s serious reason to wonder what might happen in seven years.

The exact nature of the Ares lending is unknown but reports at the time described it as a preferred equity deal, rather than a mere loan. Preferred equity confers dividends, which the PIK interest effectively is, but it’s also common for the lender to have recourse to convert debt to shares if certain conditions are triggered.

The £500million is spread out across lenders but Ares Capital Corporation (ARCC) held £69.1m of it at the end of 2025. ARCC lists its portion of the debt as a ‘senior subordinated loan’, and does not mention any accompanying warrants to buy shares in 22 Holdco in the manner it does for Eagle Football Holdings, the multi-club empire of John Textor which Ares put into administration last month.

Again, few specifics on the terms of the 22 Holdco debt are known, but ARCC’s annual report is chock-full of explanations of how the group limits its downside risk and protects investments. With its lending to BlueCo subordinated — it sits below the £800m senior debt but ranks ahead of any payouts to the ownership group — it is a safe bet they’ve covered themselves in the event BlueCo’s project goes down in flames.

That project needs significant capital appreciation if it is to be successful. Even just using the funds committed to the end of June 2025 across equity from the ownership and the £1.4billion debt, BlueCo would need to hit a valuation of £4.1bn just to break even.

A more realistic estimate would be higher still. That Ares PIK debt figure for 2033 is laden with assumptions but without any repayments made between now and then, alongside the £800million senior debt and the £2.9bn in equity committed so far, the assets accumulated by BlueCo would need to be worth £5.1bn for the group to make its money back.

How do they ever get to such a figure?

The huge losses might open up broader discussions about whether it is appropriate for a football club to be run in this manner, but in terms of strategy they represent the first phase of a plan to reinvent not only Chelsea (and Strasbourg) but perhaps football as we know it.

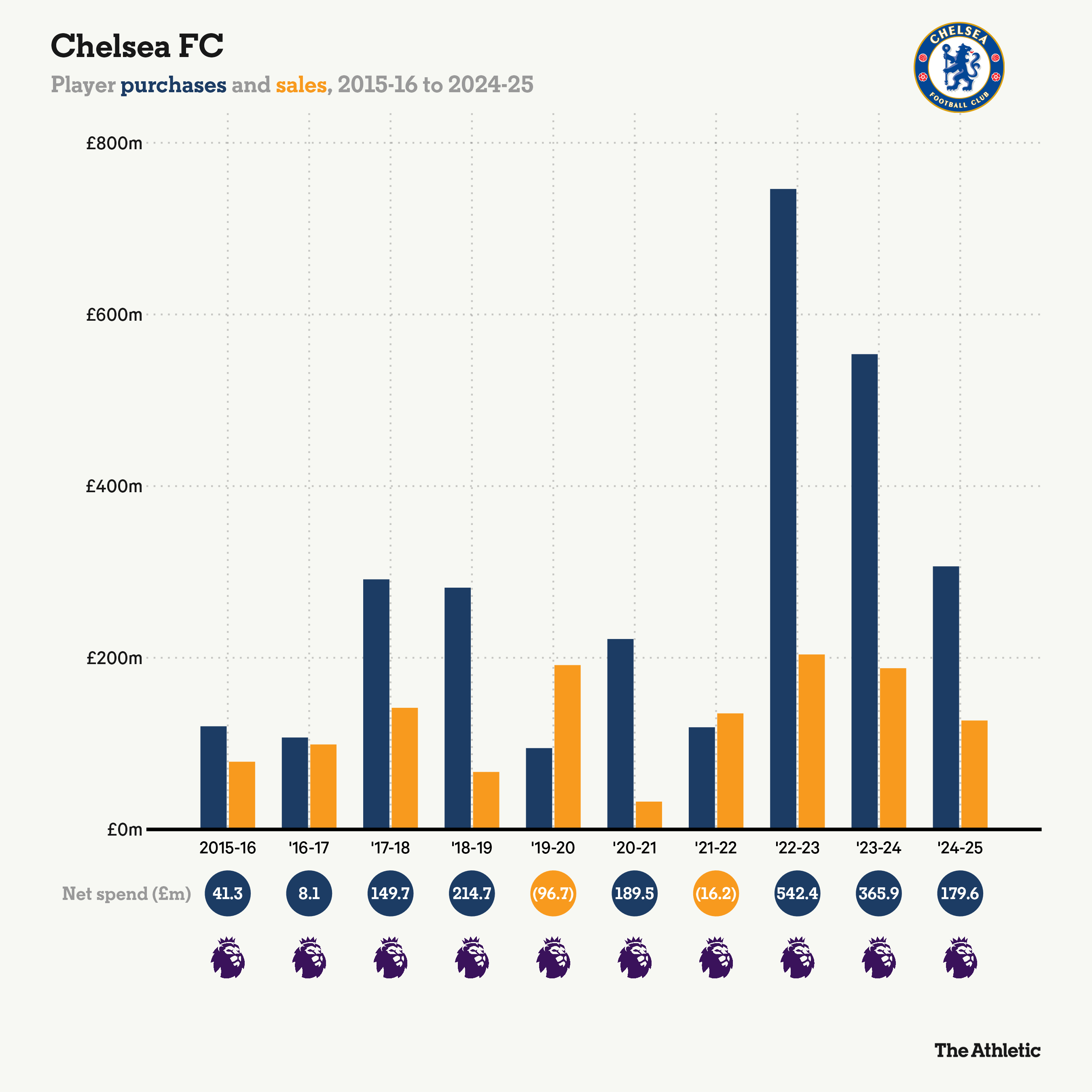

BlueCo has poured in enormous amounts to completely revamp Chelsea’s squad, deploying massive transfer fees on young players and signing them up to lengthy contracts. Over £1billion in transfer spending has gone on players aged 24 and under; they have spent more on teenagers than the rest of the ‘Big Six’ combined.

Think of that all as seed money.

Both Chelsea and Strasbourg now have the youngest squads in their respective divisions and, in BlueCo’s mind, the multi-club organisation holds the signatures of players who will be or already are worth several times what was paid for them.

BlueCo’s bet on football spans far beyond the transfer market, but it is there we’ve seen the most activity in their first four years in charge. In the first, Chelsea broke all records for transfer spending, splurging £745.2m on new players. A year later, it was £552.7m, then £305.5m last season. Between July and September 2025, a further £263.3m went on just six players: Joao Pedro, Jamie Gittens, Jorrel Hato, Alejandro Garnacho, Estevao and Ishe Samuels-Smith (who had only been sold to Strasbourg two months earlier).

In all, Chelsea under BlueCo have spent £1.867billion on new signings. The net is some way lower, but still around £1bn. The idea is that the club, alongside Strasbourg, can turn significant player trading profits from a pipeline of talent.

There are signs of a slowdown in buying, and a move to the next stage. Chelsea’s net spend of £179.6million last season was the Premier League’s third-highest but low by their recent standards. This season, a reported £300m was made on player sales. The club’s net spend might well have been negative last summer.

As a reminder, those 22 Holdco accounts are explicit about the importance of successful player trading in weaning BlueCo’s clubs off reliance on funding from above.

Yet Chelsea’s latest accounts highlight the difficulty of turning it all into consistent, high profits. As The Athletic detailed last week, the policy of lengthy contracts and high purchase fees meant those £300million in sales likely didn’t even generate £50m in profit. And only £31.8m landed in 2025-26.

Those profits are also hindered by the realities of football. No one has spent more than Chelsea’s £272million on agents in the BlueCo era, a byproduct of their huge levels of transfer activity. Chelsea’s explanation — that they partake in more deals, but fees per deal aren’t higher than elsewhere — is accurate, but nobody forced them to employ a strategy quite so frantic. And the money is still being spent, whether it is a proportionally low amount or not.

Chelsea particularly need player trading to be profitable because they continue to generate massive, historic operating losses. Even just taking the club accounts figures for last season, and excluding £50.2million in legal and regulatory fees relating to potential or accepted rules breaches, their deficit pre-player sales was £258m.

In three years under BlueCo, operating losses total £689m, or £629,000 every single day. The operating loss is even higher in UEFA submissions.

One reason behind Chelsea’s swingeing operating deficits is that revenue has barely improved even as costs have jumped.

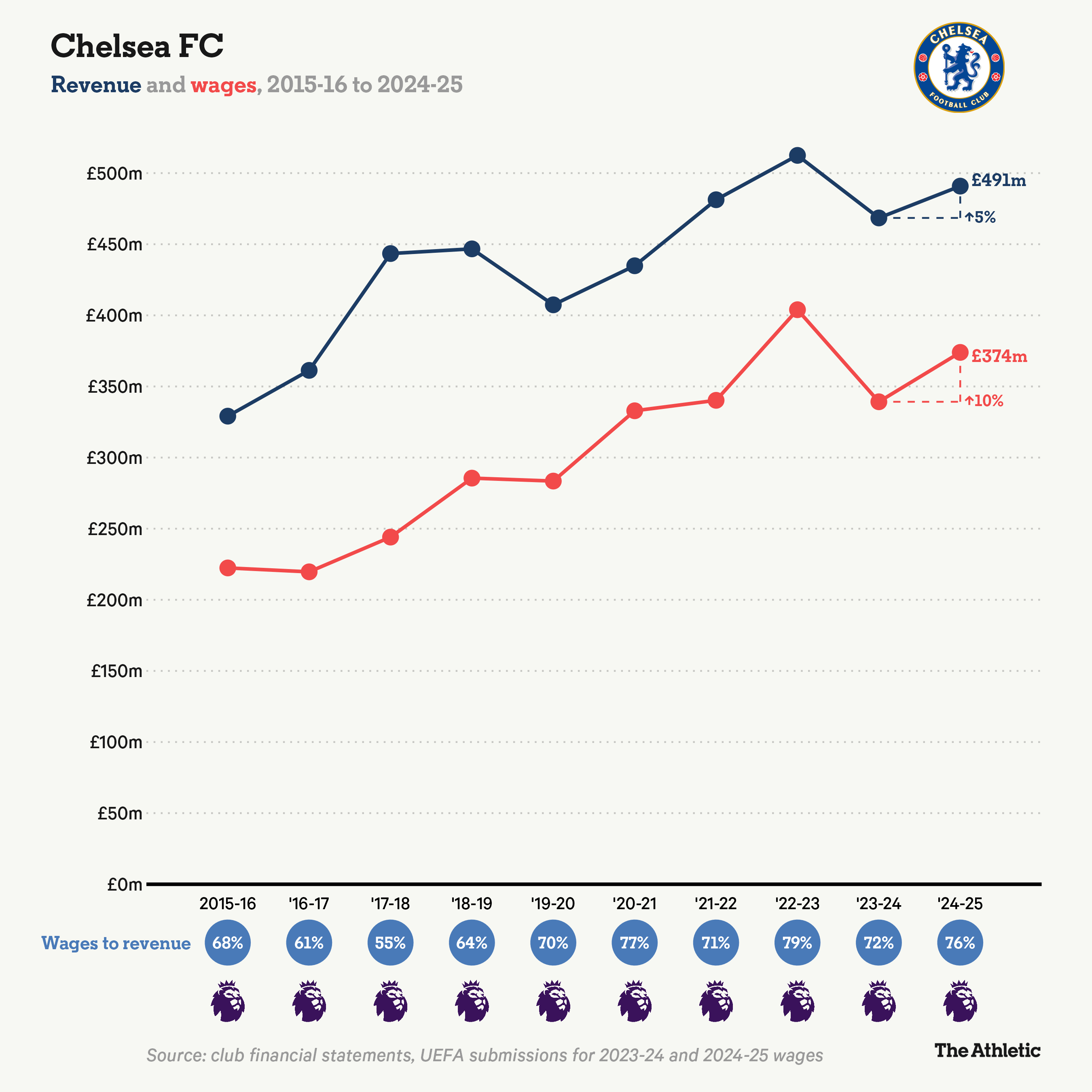

Turnover last season of £490.9million meant just a £9.6m improvement in three years, and Chelsea have fallen from the eighth-highest earning club in football to 10th under BlueCo.

Chelsea, like the rest of the ‘Big Six’, rely on TV money for less than half their income. That makes them less susceptible to performance-related swings than the rest of the Premier League, but a gap has opened to their elite peers, driven by sporting underperformance.

Non-broadcast income at Stamford Bridge last season was £287.6million, over £100m more than anyone outside the ‘Big Six’ but also over £100m less than their nearest rival among that grouping. All of Arsenal, Liverpool, Manchester City, Manchester United and Spurs earned more than £400m in non-TV money in 2024-25.

Takings at Stamford Bridge lag others, but the majority of the gulf has arisen from Chelsea’s stalling commercial revenues, hardly surprising given they’ve spent big chunks of recent seasons without a front-of-shirt sponsor. Yet, the numbers are still stark. In 2018-19, Chelsea’s £179.9million commercial income wasn’t far shy of the average of the other five clubs (£187.2m). Since then, those sides have raced beyond. Commercial income at Stamford Bridge last season was £200.9m, £62.3m behind the next-lowest in that cohort (Arsenal) and over £100m below the average of the five.

Chelsea began a 15-year kit manufacturing deal with Nike in the 2017-18 season, and a recent UEFA report disclosed it earned them around £80million last season. That made it the ninth-best kit deal in Europe, eclipsing both Paris Saint-Germain and Manchester City, but growth has been slim.

2024-25’s earnings were only £16million more than six years earlier; all of the rest of the ‘Big Six’ have enjoyed greater improvements in that time, as have nine other clubs across Europe. Bayern Munich’s kit deal last year generated £50m more than in 2018-19. At both Barcelona and Real Madrid, the improvement tops £100m. With Chelsea tied into the Nike deal until 2032, their scope for similar revenue growth is limited.

Such flailing commercial performance is made all the more stark by the fact BlueCo appear to have poured plenty of resources into improving it. Administrative and commercial staff have grown by almost half since the current owners arrived, including a 20 per cent jump last season alone. One person familiar with the situation told The Athletic that the jump in staff numbers owes to around 150 staff being absorbed from the club’s foundation rather than into the commercial department. Yet even removing that number still puts Chelsea among the top three employers of non-playing staff in England.

In turn, Chelsea’s wage bill is much higher than the wider narrative presents, and higher even than the accounts show. According to UEFA’s European Club Financial and Investment Landscape report, which incorporates that ‘reporting perimeter’, Chelsea’s wage bill last season was £374million — £15m higher than the accounts figure.

Chelsea’s wages to revenue was 76 per cent, comfortably the highest of the ‘Big Six’ and not far behind 2020-21, when Covid-19 shuttered stadia and hampered income. Only Liverpool (£428m) and Manchester City (£468m) spent more on wages last season.

That wage bill, combined with a transfer fee amortisation bill which exceeds £200million, means Chelsea’s costs are enormous. Operating expenses now top £150m even without those £50.2m legal and regulatory fees. Running costs are up across the board in football, but Chelsea’s are up 30 per cent in three seasons and, again, the true figure is higher in those UEFA reports.

In 2023, Clearlake co-founder Feliciano told attendees at the IPEM private equity conference that BlueCo were “trying to reduce the salary and essentially the [operating] expenses of the business by over $100million (£81m) per year.”

By The Athletic’s estimate, using UEFA figures and removing those legal and regulatory costs as one-offs, the reduction across wages and operating expenditure is just £6m. Meanwhile, transfer amortisation costs have exploded.

Reducing such outgoings is imperative if Chelsea are to move toward something more sustainable. By design, the first three seasons under BlueCo have not, yet now there’s a pressing need to improve the bottom line, and not just to ensure an eventual return for investors.

The Athletic outlined a year ago how Chelsea’s previous intragroup sales would have a lasting impact, and so it has proven. The club’s English record pre-tax loss of last season breached no domestic financial rules, ostensibly because Chelsea’s three-year PSR calculation still included £275.3million in paper profits generated by internal asset sales.

Compliance on the continent has been much trickier. Faced with lower loss limits and more stringent rules around both player and other asset sales, Chelsea breached each of UEFA’s Football Earnings and squad cost rules in 2023-24.

Those breaches imposed a £26.5million fine but also led them into a settlement agreement with European football’s governing body, one they now have to comply with to the end of the 2028-29 season.

The agreement is multi-faceted. Chelsea were subject to restrictions on who they could add to their ‘List A’ squad for the Champions League this season, and will be again in 2026-27 (if they qualify for any of UEFA’s three competitions).

The club got a pass on losses in 2024-25, enabling them to book that record deficit, but this season they’re limited to a maximum Football Earnings deficit of €60million (£52.2m). Next season, the maximum deficit drops to zero, although it can be topped up by whatever headroom they have in 2025-26, up to, again, a maximum of €60m. Then, in 2027-28, Chelsea must ensure their three-year Football Earnings deficit is below €60m.

If they exceed their loss limit by €20million or less in either this season or next, they’ll be fined up to €20m each time, with the size of the fine dependent on the size of the excess. Exceeding by more than €10m but less than €20m will also see that ‘List A’ sanction become more restrictive.

The real kicker is if Chelsea exceed either their 2025-26 or 2026-27 targets by more than €20million, or if they exceed that three-year loss target in 2027-28 by any sum. UEFA would then find them in breach of the settlement agreement, terminate it, and exclude Chelsea from European competition for one year, provided they would otherwise qualify within the three seasons following the breach.

Cole Palmer is one of Chelsea’s most valuable players (Photo: Robin Jones/Getty Images)

The Football Earnings rule, like Premier League PSR, allows deductions for ‘good’ expenditure, and assessing Chelsea’s position is complicated by those lengthy contracts. UEFA limit player amortisation to five years, so figures presented to regulators are higher than what we see in the accounts.

What we do know is Chelsea’s operating loss was higher in UEFA submissions, with a £15million difference in the wage bill and around £12m more in operating costs. That only accounts for £27m of the overall £80m difference in pre-tax loss highlighted earlier, and The Athletic was not able to obtain an explanation from Chelsea of the remaining £53m.

Some of it, undoubtedly, stems from the impact of shortened amortisation periods, though that’s unlikely to account for all of it. Whatever the case may be, Chelsea’s operating loss under UEFA rules was even higher than the £258m in their accounts.

Chelsea are confident that figure will tumble this season, and they need it to. With just £31.8million in player sale profits made last summer, their previous recourse for lowering operating losses hasn’t made much of a dent.

Reports elsewhere, echoed by sources spoken to for this piece, have outlined an expectation Chelsea will hit £700million in revenue this season, which would help. The claim is a little hard to fathom, though we do know they are on course for record broadcast income.

Chelsea’s successful Club World Cup campaign last summer generated £85million in prize money, of which £18m fell into 2024-25. The Athletic estimates a return to Champions League football has reaped a further £80m, or £62m higher than last season’s takings from winning the Conference League. Chelsea’s TV income should top £300m this season, though the unknown is what they’ll earn from the Premier League.

A new TV deal cycle is expected to have increased overall distributions to clubs but each league spot is now understood to be worth over £3m in merit payments. Dropping down the table would, naturally, hinder earnings.

Even with broadcast income up by over £100million, £700m in revenue would still require a near-£100m increase across matchday and commercial income. That looks steep. Stamford Bridge’s earning potential is limited, even with more lucrative European games.

Commercially, Chelsea again went a large chunk of this season without a front-of-shirt sponsor, before inking a deal with IFS in February. Nicolas Jackson’s roughly £14million loan fee will help that line item but getting to a level of revenue only two other English clubs — Manchester City and Liverpool — have reached looks an ambitious goal from here.

Coming in under the €60million loss limit is doable if £700m revenue is achieved, albeit The Athletic’s estimate reckons Chelsea would only be able to increase costs across wages, operating expenses and player amortisation by a maximum of seven per cent this season and remain compliant — unless further, more profitable player sales are made before the end of June.

Such sales will become especially urgent next season if the nightmare scenario of missing out on the Champions League unfurls again. Chelsea’s revenue will already lose £67million in Club World Cup earnings; missing out on the Champions League would at least halve their £80m take from this season’s competition.

Chelsea are struggling to qualify again for the Champions League (Photo: Ryan Pierse/Getty Images)

Being banned from Europe for a year would only further compound the issue and further delay the appreciation in club value BlueCo needs. For their part, Chelsea are confident they will comply with the settlement agreement even if they drop into the Europa League.

Yet if they do require extra measures to achieve that compliance, the obvious solution is also a painful one: selling Chelsea’s best players.

Even that is limited in scope. As The Athletic detailed recently, selling Enzo Fernandez would need a fee of around £75million this summer just to break even on his book value. Of players who would be easier to generate significant profit from, the clearest candidate is Cole Palmer, whom it is tough to imagine anyone would be happy to see leave.

Chelsea’s finances, like several in football’s elite now, are heavily reliant on sustained revenues from Champions League football. Missing out again this season would not only delay an improvement in those finances, it would also heighten the likelihood of breaching a UEFA settlement agreement which would, in turn, lead to further absence from the competition.

The ownership group’s entire project is built on the premise Chelsea’s value will increase significantly, ideally by the end of a 10-year lock-up period in 2032 or the Ares debt maturity a year later.

There have been suggestions BlueCo can, contrary to reports at the time of the takeover, sell Chelsea while retaining their 22 Holdco shares. A source with understanding of the matter told The Athletic that is a misreading of things, and an “anti-circumvention” clause exists. In any case, the group’s borrowings are secured against holdings in the club; without those borrowings being repaid, which isn’t happening any time soon, BlueCo would struggle to sell up even if they wanted to.

Achieving a huge value increase is the only way Clearlake, in particular, will be able to return value to their investors from the BlueCo project.

The pertinent question for the rest of football is a simple one: how do they achieve that inflated value?

It is safe to say it will not come via a levelling of the playing field across the English pyramid, by an increase in competitive balance in a sport where, already, the best indicator of success is how much you spend.

Transforming Chelsea internally is one thing, but back in October 2022, speaking at SporticoLive’s Invest in Sport summit, Clearlake co-founder Eghbali said their investment in football was “about looking at the macro” and his belief that “European sports is probably 20 years behind U.S. sports in terms of sophistication on the commercial and data side”.

Eghbali was clear in his belief that a global audience was waiting to be tapped, and the most obvious macroeconomic change to aid Chelsea’s valuation would be a shift in broadcast rights values. Yet while the Premier League recently announced a trial of its first direct-to-consumer streaming service in Singapore, there’s nothing concrete to suggest TV rights will explode in the next seven years. UEFA’s growing TV deal would help too, but Chelsea keep failing to qualify for the only competition of financial worth to them.

Chelsea should earn more if TV deals rise (Photo: Darren Walsh/Chelsea FC via Getty Images)

So can BlueCo make this all add up?

A New York Times article in December identified Clearlake as one among many private equity firms “struggling to deliver on their core business model of taking on debt, buying companies and selling them for a profit”. One short-term fix, which Clearlake has deployed at times, is to use “continuation vehicles”, whereby firms sell companies to themselves, booking a paper gain while they wait for interest rates and selling conditions to improve before offloading those companies for actual money.

Those continuation vehicles reflect a broader struggle in private equity over the past few years. In July 2024, work from Bloomberg identified at least $10billion in distressed debt among Clearlake’s portfolio companies, the highest among any private equity firm. The end of low interest rates has made turning investments into profitable exits rather more difficult.

However, in each of the Clearlake funds known to have provided funding to the BlueCo project — COP III and the VII fund — recent public filings from some of the two funds’ investors have listed the market values of those investments as higher than the amount invested. The uplift has generally been around 10 per cent.

Meanwhile, the women’s team has at least begun bearing financial fruit for BlueCo. Alexis Ohanian’s 776 Chaos Fund has bought 7.6 per cent of the team for £18.5million in two transactions, the latter valuing Chelsea Women at £255m, or 28 per cent higher than the £200m of the internal sale made in June 2024.

Yet those are small gains in the context of the BlueCo bet. With no progress on Stamford Bridge and repeated exile from the Champions League, Chelsea’s value does not look discernibly higher than four years ago. The synergies of multi-club ownership have been slow in materialising; commercial revenues, a clear focal point of the project, are falling behind rather than overtaking rivals.

There is time left and plenty that may change. BlueCo will point to two trophies last season and massive player sales last summer as partial proof of concept. But the reality is they need an awful lot more for their gambit to pay off.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}