As central banks in major economies hold interest rates steady amid geopolitical uncertainties, Asian markets are navigating a complex landscape marked by both challenges and opportunities. In this environment, growth companies with strong insider ownership can offer unique insights into their potential stability and long-term vision.

Top 10 Growth Companies With High Insider Ownership In Asia

|

Name |

Insider Ownership |

Earnings Growth |

|

Zhejiang Taotao Vehicles (SZSE:301345) |

27.5% |

31.7% |

|

UTI (KOSDAQ:A179900) |

24.6% |

113.6% |

|

Shanghai Biren Technology (SEHK:6082) |

11% |

121.5% |

|

SEERS (KOSDAQ:A458870) |

33.2% |

45.2% |

|

Modetour Network (KOSDAQ:A080160) |

12.5% |

61.6% |

|

Meitu (SEHK:1357) |

22.7% |

31.4% |

|

L&C BIOLTD (KOSDAQ:A290650) |

26% |

155% |

|

J&V Energy Technology (TWSE:6869) |

17.9% |

114.3% |

|

Guangzhou Tinci Materials Technology (SZSE:002709) |

38.4% |

32.6% |

|

Gold Circuit Electronics (TWSE:2368) |

30.5% |

36.8% |

Let’s review some notable picks from our screened stocks.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited, along with its subsidiaries, operates in the automobiles and batteries sectors across the People’s Republic of China, Hong Kong, Macau, Taiwan, and internationally with a market cap of approximately HK$1.02 trillion.

Operations: BYD’s revenue segments include its operations in the automobiles and batteries industries across various regions, including China, Hong Kong, Macau, Taiwan, and international markets.

Insider Ownership: 28.3%

Earnings Growth Forecast: 20.7% p.a.

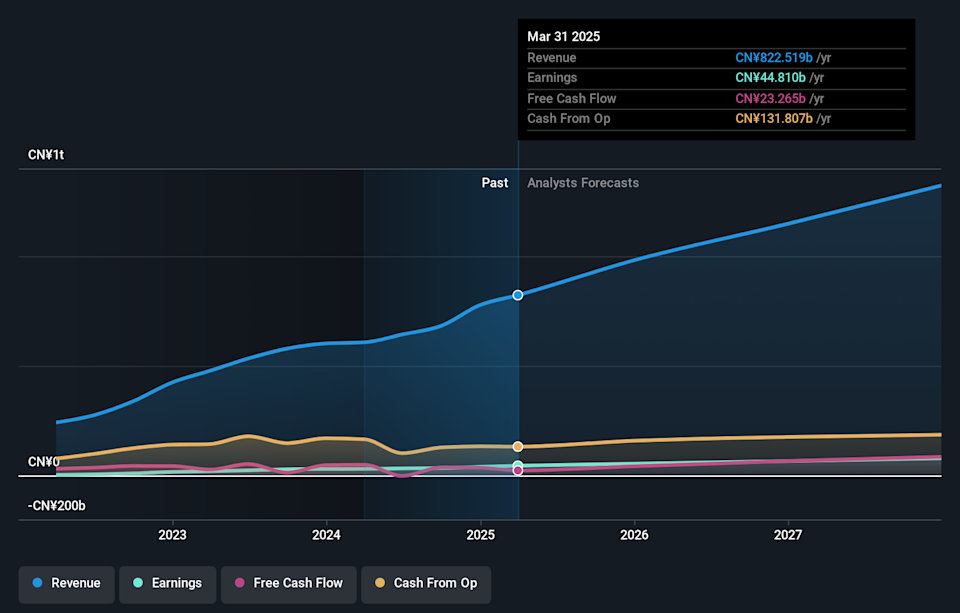

BYD is experiencing significant earnings growth, projected at over 20% annually, outpacing the Hong Kong market. However, recent financial results show a decline in sales and net income compared to last year. Trading below estimated fair value suggests potential upside, supported by analysts’ consensus of a 21.4% price increase. The company’s strategic partnerships and technological advancements in electric vehicles highlight its focus on innovation and expansion in the global automotive sector.

Simply Wall St Growth Rating: ★★★★★☆

Overview: Raytron Technology Co., Ltd. is involved in the R&D, design, manufacturing, and sales of uncooled infrared imaging, MEMS sensors, and image processing algorithms technology in China with a market cap of CN¥66.80 billion.

Operations: Raytron Technology Co., Ltd. generates revenue through its activities in uncooled infrared imaging, MEMS sensors, and image processing algorithms technology within the Chinese market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}