It’s a battle between a big stock market winner and a potential turnaround opportunity.

It’s a matchup between the world’s largest retailer and its smaller discount store rival. In one corner, Walmart (WMT -0.64%) stock is having a banner year, up 54% amid a string of better-than-expected results. On the other side, Dollar General (DG -1.25%) has struggled to manage weak sales, sending shares lower by 51% year to date.

What does this night-and-day difference in the performance between these two consumer goods giants mean for each stock heading into 2025? Let’s discuss whether shares of Walmart or Dollar General may offer the best buying opportunity right now.

The case for Walmart

Walmart investors have a lot to cheer about with the stock trading at a record high. Resilient macroeconomic conditions coupled with easing inflationary cost pressures and steps to improve operating efficiency have driven an earnings growth rebound.

In the last reported second quarter (for the period ended July 31), Walmart posted a 10% year-over-year increase in adjusted earnings per share (EPS) as the gross margin reached its highest level in nearly three years.

A major theme for the company has been its ability to pull bargain-seeking upper-income households into its stores, which management cited as contributing to its retail industry share gains. Second-quarter U.S. comparable sales climbed by 4.2% from the period last year, including momentum from the e-commerce business, where revenue was up 21%.

Trends internationally and in the Sam’s Club segment have also been solid, leading Walmart to revise its full-year growth guidance higher. For fiscal 2025, the company expects adjusted EPS in a range from $2.23 to $2.37, up around 10% at the midpoint from 2024.

Ultimately, the attraction of Walmart as a potential investment is its leadership and global diversification with a case to be made that its outlook is as strong as ever.

Image source: Getty Images.

The case for Dollar General

Sizing up Dollar General against Walmart is far from an apples-to-apples comparison. In this case, the company specializes in everyday household necessities through a smaller convenience store format. This is in contrast to Walmart’s wider selection that includes big-ticket items like furniture and electronics.

Despite an aggressive growth strategy, increasing its retail square footage by 5.5% this year, Dollar General’s results have disappointed. In its second quarter (for the period ended Aug. 2), same-store sales increased by just 0.5%, while its diluted EPS was down 20% from Q2 2023.

Management has pointed to a challenging economic environment, citing its core customers feeling financially constrained. This narrative is concerning, particularly next to Walmart, which is presenting a more positive industry assessment.

That being said, it’s important to recognize the strengths in Dollar General’s fundamentals. Even through the discouraging headlines, the company remains profitable and generates positive free cash flow with a well-supported balance sheet.

The company plans to get “back to basics” by improving its merchandise mix, adjusting inventory levels, and addressing supply chain constraints to drive sustainable growth. The ability to stabilize sales and improve margins will be points to monitor for the next several quarters, as they could kickstart a sustained rally in the stock price.

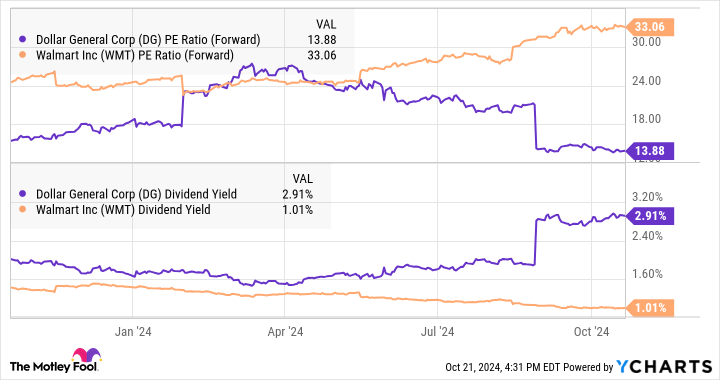

What makes shares of Dollar General interesting for investors today is its relative value following the stock price sell-off and reset of expectations. Shares are trading at 14 times its full-year consensus EPS, representing a deep discount to Walmart trading at 33 times the same valuation metric. Dollar General also offers a 3% dividend yield, compared to just 1% from Walmart.

DG PE Ratio (Forward) data by YCharts

The better buy: Walmart

As compelling as Dollar General’s turnaround opportunity could be, the company still has a lot of work to do and remains speculative without clear evidence of a bottom in its key financial metrics. The risk is that its results continue to disappoint, forcing the company to proceed with a more drastic restructuring strategy.

By this measure, I believe Walmart stock is the better buy today and the prudent choice for most investors, with the company well positioned to continue rewarding shareholders over the long run. Walmart’s high-quality fundamentals and global growth potential help justify the stock’s premium valuation and can work for investors within a diversified portfolio.

Dan Victor has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Walmart. The Motley Fool has a disclosure policy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}