In today’s relatively subdued markets, the notable development is weakness in commodity currencies, led by Australian Dollar. This decline comes amid a drop in oil prices following Saudi Arabia’s decision to cut official selling prices across all regions. Additionally, precious metals have softened in response to rebound in global benchmark treasury yields. The downward trend also extends to industrial metals, which are affected by worsening global economic outlook.

On the other hand, Japanese Yen is currently the strongest among major currencies, but its gains are tempered as traders anticipate the release of Tokyo’s CPI and and Japan’s household spending data tomorrow. Euro is showing resilience despite weaker-than-expected investor confidence and retail sales data, trailing closely behind Yen. Swiss Franc is also performing well, supported by CPI figures that met expectations. Meanwhile, Dollar and British Pound are mixed movements.

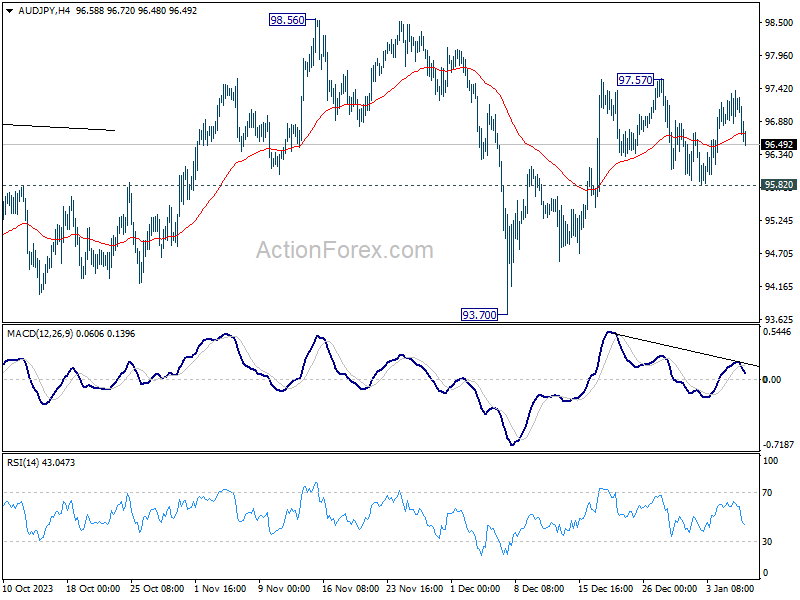

AUD/JPY would be a pair to watch in the upcoming Asian session, considering that Australia will also release retail sales. For now, rebound from 93.70 could still extend through 97.57 resistance. However, as this rise is seen as the second leg of the consolidation pattern from 98.56, upside should be limited by the resistance. Break of 95.82 minor support will suggest that the third leg has started to 93.70 support and below.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is up 0.28%. CAC is up 0.08%. Germany 10-year yield is up 0.048 at 2.207. UK 10-year yield is up 0.038 at 3.830. Earlier in Asia, Hong Kong HSI fell -1.88%. China Shanghai SSE fell -1.42%. Singapore Strait Times rose 0.09%. Japan was on holiday.

Eurozone Sentix rises to -15.8, but German recession continues

Eurozone Sentix Investor Confidence rose from -16.8 to -15.8 in January, below expectation of -15.4. That’s nonetheless the third increase in a row, and the highest reading since May 2023. Current Situation Index also rose for the third month from -23.5 to -22.5. Expectations Index rose for the fourth month, from -9.8 to -8.8, highest since February 2023.

Sentix noted that the sharp drop of -18 points in the sub-index of inflation expectations, from 16.25 to -1.75, raises concerns. This significant decrease is attributed not only to extensive administrative cost increases from tax hikes in Germany but also to a noticeable rise in freight costs, influenced by recent unrest in the Red Sea area. These factors suggest that the prevailing interest rate optimism might be misguided, potentially imposing new challenges on the already struggling Eurozone economy.

Also to be noted, Germany’s overall Investor Confidence Index fell from -25.5 to -26.1. Current Situation Index fell from -35.3 to -35.5. Expectations Index fell from -15.3 to -16.3. Sentix noted, “Germany is not emerging from the recession and thus from its economic crisis.”

Eurozone retail sales fall -0.3% mom in Nov, EU down -0.2% mom

Eurozone retail sales fell -0.3% mom in November, worse than expectation of -0.1% mom. Volume of retail trade decreased by -0.4% for non-food products and by -0.1% for food, drinks and tobacco, while it increased by 1.4% for automotive fuels.

EU retail sales fell -0.2% mom. Among Member States for which data are available, the largest monthly decreases in the total retail trade volume were registered in the Germany (-2.5%), Luxembourg (-1.4%) and Austria (-0.7%). The highest increases were observed in Portugal (+3.1%), Croatia and Slovenia (both +3.0%), Malta and Romania (both +1.7%).

Swiss CPI rises to 1.7% yoy in Dec, matches expectations

Swiss CPI was flat at 0.0% mom in December, above expectation of -0.1% mom. Core CPI (fresh and seasonal products, energy and fuel) rose 0.2% mom. Domestic products prices rose 0.3% mom. Import products price fell -0.7% mom.

For the 12-month period, CPI rose from 1.4% yoy to 1.7% yoy, matched expectations. Core CPI rose from 1.4% yoy to 1.5% yoy. Domestic products prices rose from 2.1% yoy to 2.3% yoy. Imported products prices from also rose from -0.6% yoy to -0.2% yoy.

Also published, retail sales rose 0.7% yoy in November, above expectation of 0.0% yoy.

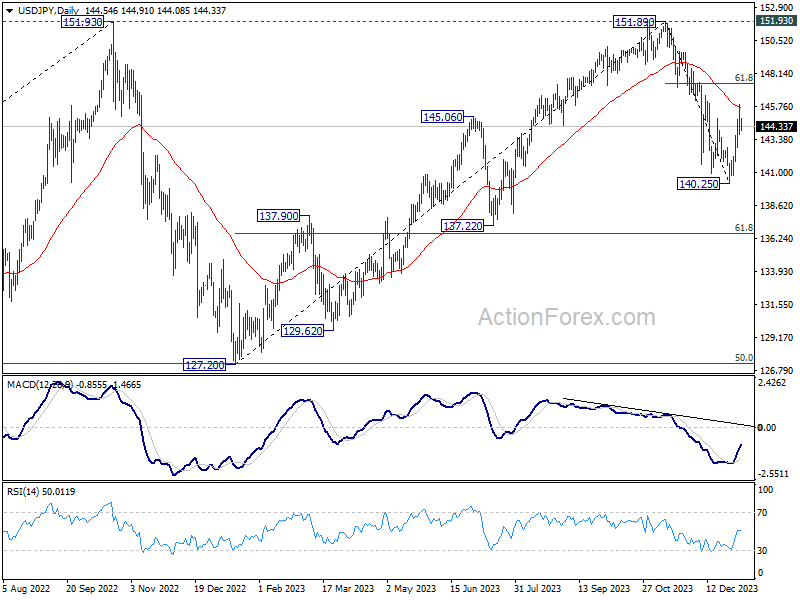

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.63; (P) 144.80; (R1) 145.80; More…

Intraday bias in USD/JPY stays neutral at this point. On the upside, above 145.97 will resume the rebound from 140.25. But upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, below 143.17 minor support will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | Germany Factory Orders M/M Nov | 0.30% | 1.10% | -3.70% | -3.80% |

| 07:00 | EUR | Germany Trade Balance (EUR) Nov | 20.4B | 17.9B | 17.8B | 17.7B |

| 07:30 | CHF | Real Retail Sales Y/Y Nov | 0.70% | 0.00% | -0.10% | -0.30% |

| 07:30 | CHF | CPI M/M Dec | 0.00% | -0.10% | -0.20% | |

| 07:30 | CHF | CPI Y/Y Dec | 1.70% | 1.70% | 1.40% | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | -15.8 | -15.4 | -16.8 | |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Dec | 96.4 | 93.8 | 94.0 | |

| 10:00 | EUR | Eurozone Industrial Confidence Dec | -9.2 | -9.5 | ||

| 10:00 | EUR | Eurozone Services Sentiment Dec | 8.4 | 4.9 | 5.5 | |

| 10:00 | EUR | Eurozone Consumer Confidence Dec F | -15.0 | -15.1 | -15.1 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Nov | -0.30% | -0.10% | 0.10% | 0.40% |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}