(Dec 29): A growing number of currency funds are looking to battered currencies that could benefit from lower interest rates as they attempt to replicate 2023’s blockbuster returns from the carry trade.

Betting on a so-called value strategy — by buying into the cheapest currencies and positioning for them to rise against more expensive ones — is now being adopted by an increasing number of investors, according to Bank of New York Mellon Corp (BNY Mellon), which has a bird’s-eye view on more than US$45 trillion (RM209.38 trillion) of asset flows. CIBC Asset Management, Allspring Global Investments and Neuberger Berman, which together control more than US$1 trillion, are among those anticipating these value trades will outperform next year.

It’s a brave stance for currency funds, 80% of which have exited the market since the 2008 financial crisis amid a slump in volatility and the rise of algorithmic trading. Carry — which exploits the gaps between interest rates in different countries — has handed them a much needed banner year, with borrowing in yen to buy a basket of three emerging-market currencies netting a hefty 42%, for example. That’s nearly double the gains in the S&P 500 stock index. Value, by contrast, lost money.

But a looming pivot by global policymakers towards interest-rate cuts is spurring wagers that 2024 will be different.

“We are starting to rotate more towards value,” said Michael Sager, deputy chief investment officer at CIBC, who sees the driver of his portfolio shifting away from carry. “The expected return on value trades looks very, very large.”

The strategy certainly has some ground to make up. Value has been on its worst run in more than a decade, losing money this year and last, according to a Bloomberg GSAM gauge of the strategy. By contrast, carry has been a winning bet, with the strategy helping currency funds deliver their best two years of performance since the early 2000s.

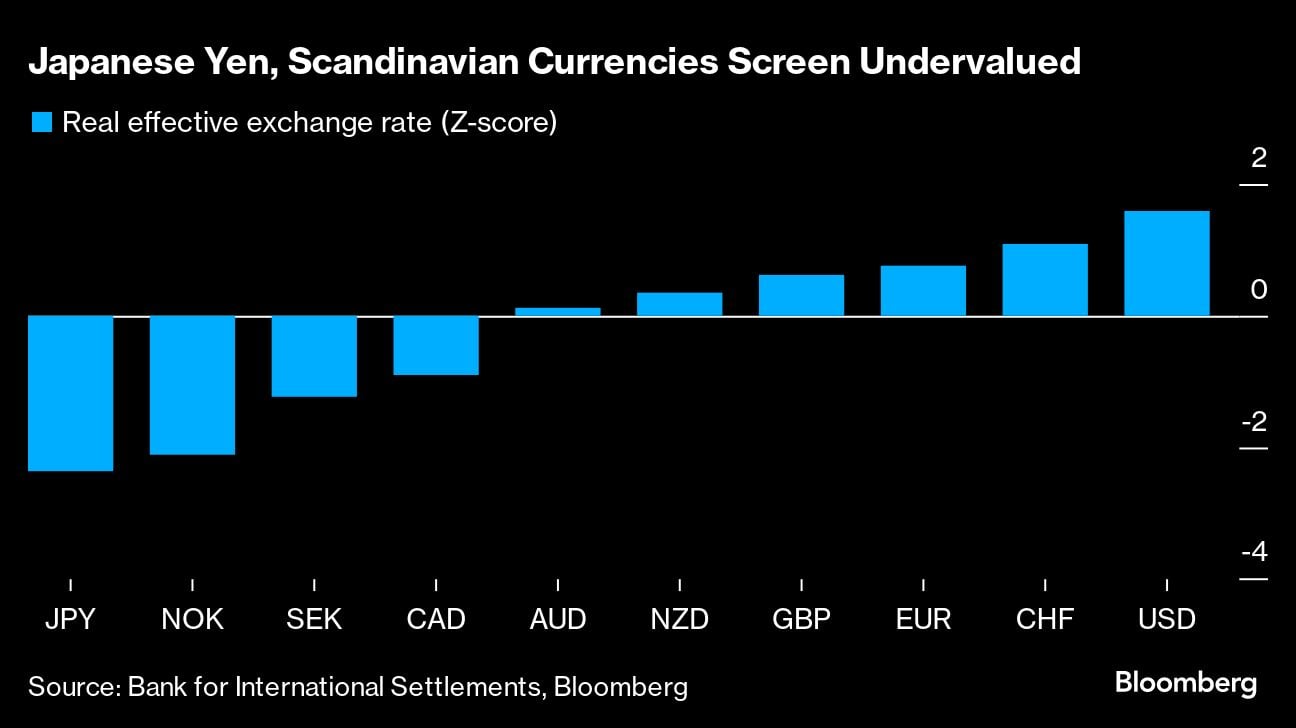

Yet the popularity of carry trades has laid the groundwork for a sharp U-turn in performance. The most undervalued Group of 10 (G10) currency is the Japanese yen, the favoured funder for reaping lofty profits from higher yielding currencies. The Norwegian krone and Swedish krona also look undervalued, while the US dollar is the most overvalued, according to a Bloomberg ranking based on the Bank for International Settlements’ (BIS) calculation of real effective exchange rates.

“Holdings of carry currencies are really full right now and that’s made them expensive,” said John Velis, a currency strategist at BNY Mellon, who favours pitting Latin American currencies against underheld southeast Asian currencies — a reversal of the carry trend. “It’s time for value strategies to start to pay off.”

Indeed, some value strategies are starting to work already. Norway’s krone, the Swedish krona and the yen saw the biggest gains among G10 pairs against the dollar this month, after Federal Reserve chair Jerome Powell’s dovish pivot fuelled rate-cut bets and brought relief to the most beaten-down currencies.

For Bank of America Corp strategists, betting on the krone against the euro is a high conviction value trade. At Citigroup Inc, going short the Swiss franc against the yen is seen paying off.

“Value has been underperforming for years but sooner or later it will be the winning strategy,” said Ugo Lancioni, a fund manager at Neuberger Berman who anticipates the biggest gains to come from the yen. “At the end of the cycle, value tends to perform better than carry or momentum.”

However, FX managers should beware prematurely abandoning carry.

Indeed, even as a broad gauge of carry has slipped this month, betting on the Colombian peso versus the dollar — one of the top carry trades of the year — has returned more than 5%. The peso is one of 17 emerging-market currencies that has delivered positive returns versus the US currency in December.

“Carry can continue to perform in a slowdown,” said Parisha Saimbi, a currency strategist at BNP Paribas SA. “As we head through the first quarter, those strategies may become less favored and I anticipate a broader rotation into value.”

The key turning point for a broader suite of value strategies to start paying off will require the dollar to weaken. Despite a gauge of the index currently hovering near its lowest since July, the greenback remains overvalued, keeping up the pressure on currencies around the world.

Fidelity International and JPMorgan Chase & Co warn that the dollar may surprise with strength in the first half of next year, while BNP Paribas sees value as unlikely to outperform until rate cuts begin.

Still, Lauren van Biljon, an Allspring portfolio manager, is preparing to position for a reversal of weakness in the yen and South African rand, where she says “the valuation gap looks too extreme to persist.”

And for early movers like CIBC’s Sager, the expectation for outsized swings and potential big payouts is worth the wait.

“The trouble with value is that it’s like a rubber band,” said CIBC’s Sager. “You stretch it and stretch it and one day it snaps back, but you never know when that day is going to be.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}