Emerging markets and developing economies (EMDEs) face a daunting challenge in securing sufficient climate finance to limit global warming to 1.5°C. Local capital markets in many EMDEs lack depth, are characterized by high interest rates, short maturities, and insufficient volumes to meet climate-related needs, and can, at best, provide only about 50% of the funds needed for the climate transition.

The gap will have to be met by international climate finance from public and private sources. Estimates for climate investment needs in EMDEs vary from USD 1 trillion to USD 2 trillion annually by 2030 to reach net zero greenhouse gas emissions by 2050. However, currency risk remains a key barrier to deploying international capital to climate projects in EMDEs.

This paper explores risks arising from the mismatch between debt denominated in “hard” currencies (e.g., US dollars or euros) and the revenues used to repay the debt denominated in local currencies—as is frequently the case for climate-related projects. In such situations, depreciation of the local currency can make debt repayment more expensive in local currency

terms, threatening the financial viability of projects. The first section of this paper analyzes the sources and effects of currency risk for climate investments in EMDEs. Several key challenges emerge, including:

- Affordable long-term lending for climate projects in EMDEs is often unavailable in local currency, but hard currency loans create risks for actors across the climate investment landscape. Borrowers (e.g., EMDE governments and local private companies) face increased debt burdens in the event of currency devaluation. This, in turn, creates heightened credit risk for loan providers (e.g., DFIs and foreign investors).

- Commercial financial products to hedge currency risk are often costly for borrowers in EMDEs. These products are priced based on a combination of real and perceived risks of investing in EMDEs, and their costs often fully offset the lower interest rates available for hard currency loans for climate projects. Moreover, these hedging products are frequently unavailable in frontier-market currencies, or for longer maturities even in the more developed emerging markets.

While stronger macroeconomic policy frameworks and deeper financial markets in EMDEs are the most effective long-term solutions to these challenges, affordable hedging mechanisms to reduce the delivered cost of capital and unlock private climate finance for EMDEs are critical near-term measures. To that end, several innovative solutions have been suggested for countries at different levels of financial development, and which are at varying stages of implementation.

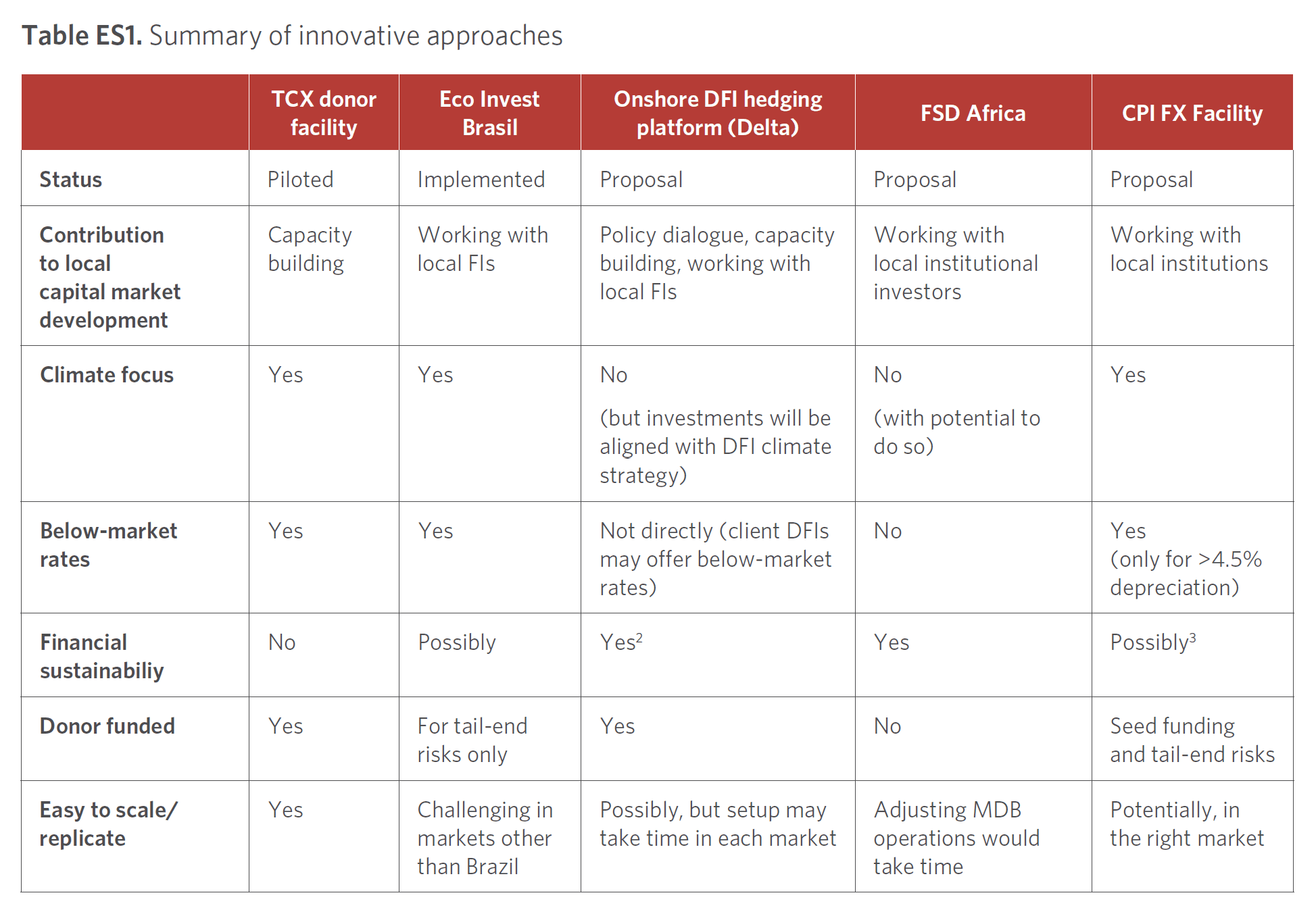

The second section of this paper examines five solutions, either at the proposal stage or in early implementation, to better understand their operation and potential to improve the affordability of hedging tools and enhance local currency lending:

1. A donor-funded guarantee facility planned by The Currency Exchange Fund (TCX) to complement its existing offerings.

2. Eco Invest Brasil, a partnership between the Brazilian government and the Inter-American Development Bank.

3. An onshore DFI hedging platform to support local currency lending by DFIs (named Delta by its sponsors).

4. An MDB transfer mechanism developed by FSD Africa.

5. An FX hedging facility in India, developed through the Global Innovation Lab for Climate Finance.

These innovative models use various mechanisms to affordably mitigate currency risks for climate projects in EMDEs. These include enhancing concessional capital to subsidize hedging products, creating onshore platforms to facilitate local currency financing, refinancing loans from multilateral development banks (MDBs) in local currency to recycle capital, and spreading

currency risks among different stakeholders.

Each solution has tradeoffs, and several are market-specific, which may impede their replicability. They may also face challenges to their long-term financial sustainability, implementation speed, and scale.

CPI has compared these solutions across various aspects – as summarized in the table below.

Recommended actions

To meet EMDEs’ climate finance needs, innovative financing mechanisms such as those analyzed in this report must be implemented and scaled urgently. Key to this effort is a collaborative approach involving donors, MDBs, and EMDE governments, each playing a vital role in fostering sustainable financial practices aligned with climate objectives.

As each EMDE faces unique challenges, it is critical to recognize that different markets require tailored solutions. The three climate-focused proposals target high-emitting emerging economies such as Brazil and India, where local currencies are more accessible. This highlights the discrepancy with least developed countries (LDCs), which are low emitters with very underdeveloped financial markets. There is a significant need for highly concessional financing for climate-related investments in LDCs, which are often left behind in climate finance efforts.

- Concessional capital providers (donor governments, philanthropies, DFIs, MDBs, etc.) can contribute concessional capital to help scale mechanisms that provide more affordable hedging solutions.

- MDBs can consider running pilot programs to adapt and scale some of the above models across EMDEs. At the same time, MDBs could also expand on local currency lending and provide technical assistance to deepen domestic capital markets and enhance financial sector resilience.

- EMDE governments can strengthen macroeconomic policies and regulatory frameworks to support the growth of their financial sectors, implement strategic country platforms to align financial and climate goals, and enact reforms to enable effective blended finance structures and the development of secondary markets for climate finance.

- Research institutions should analyze how to improve access to and affordability of hedging instruments to effectively scale up international private financial flows. For MDBs/DFIs, research should explore the expansion of local currency lending, the promotion of risk-sharing instruments, and effective blended finance approaches. For the private sector, research should promote participation in currency risk management through government- or MDBsupported products. For EMDE national governments, research should assess the policy adjustments needed to facilitate FX hedging instruments and create an enabling environment for their effectiveness.

{kind=link}

{kind=link}

{kind=link}

{kind=link}