Image © Adobe Images

The Dollar has risen in reaction to the release of November’s U.S. inflation data showing a 0.1% rise month-on-month in headline CPI, an increase on October’s 0% print and larger than the flat 0% reading the market anticipated.

Core CPI inflation read at 0.3% m/m in November, up on October’s 0.2%, albeit in line with investors’ expectations.

The reading comes on the day the Federal Reserve’s Open Market Committee (FOMC) meets to deliberate on the details of their next policy decision, due to be announced tomorrow.

“The U.S. inflation report suggests that disinflation is not a straight-line affair. Prices overall ticked up slightly despite lower energy prices,” says David Kohl, Chief Economist at Julius Baer.

The Fed might reference the slight uptick in m/m inflation to push back against the recent shift in market expectations towards more and earlier rate cuts in 2024, a situation which prompted the USD to fall through November.

“For the Fed’s taste, market expectations of rate cuts in the near future are likely to have gone too far. It is therefore to be expected that Fed Chairman Powell will try to dampen speculation about rate cuts at the press conference after tomorrow’s FOMC meeting,” says Christoph Balz, Senior Economist at Commerzbank.

Any success in pushing back on these bets by the Fed would be consistent with the current recovery in USD extending.

“November CPI showed price pressures mildly accelerate,” says Ali Jaffery, an economist at CIBC Capital Markets. “This reinforces our call that the Fed will not ease policy until late 2024.”

Above: GBPUSD at one-minute intervals. Track GBPUSD with your own custom rate alerts. Set Up Here.

The Pound to Dollar exchange rate has fallen through the hour following the inflation report and is quoted at 1.2518 at the time of writing.

Should the Fed push the timing of rate cut expectations further into 2024, Pound-Dollar can end the week firmly in 1.24s, all else being equal.

There are nevertheless reasons to suspect Dollar strength on the inflation-Fed narrative might ultimately prove limited, as the details of Tuesday’s report by no means point to rising inflationary pressures.

In fact, Viraj Patel, FX Strategist at Vanda Research, says the report is “dovish USD” as “under the hood” the details are soft.

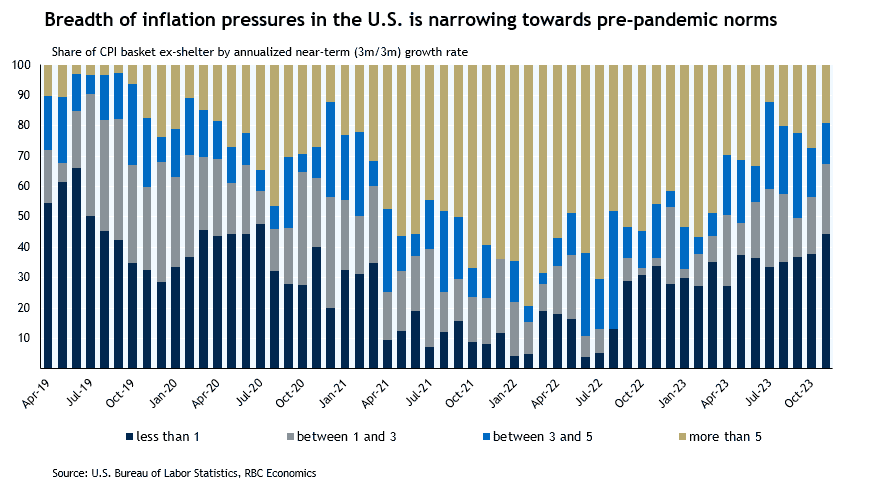

“Only 35% of the basket showed more than 0.2% MoM inflation. Goods, clothing, food & energy all pretty much in deflationary territory (56% of basket saw price cuts). In other words, only a few things drove CPI upside,” he explains.

Above: The breadth of inflationary pressures in the U.S. are receding to pre-pandemic norms. Image courtesy of RBC.

Christoph Balz, Senior Economist at Commerzbank, says the underlying inflationary pressure is decreasing, but only gradually.

“In view of these trends, it is unlikely that the Federal Reserve will raise interest rates again. However, a rate cut is also not realistic until mid-2024,” says Balz.

The market might be coming around to this view, particularly in light of last Friday’s surprisingly robust U.S. labour market report.

Claire Fan, an Economist at Royal Bank of Canada says the Fed will retain the option to push interest rates higher as economic growth remains resilient and Chair Powell has actively pushed back against rhetoric around rate cuts in 2024.

“We continue to expect the Fed to stay on hold, until pivoting to gradual cuts in the second quarter of 2024,” says Fen.

“Price growth remains far enough away from 2% that the central bank likely will not declare victory just yet. We suspect the FOMC will keep monetary policy in a holding pattern and look toward the Q1 labor market and inflation data to determine its next move. Our base case for the first rate cut remains June 2024,” says Sarah House, Senior Economist at Wells Fargo.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}