Ryan Horne

Razvan Remsing

Like a phoenix rising from the ashes, currency alpha has re-emerged after a decade-long slumber. Foreign exchange—the largest, most liquid financial market globally—has been reinvigorated by two underpinning currency alpha strategies: momentum and carry.

To shed light on what has contributed to a renewed uptick in opportunities, we explored three significant periods for momentum and carry strategies, as applied to FX markets:

To gain a clearer understanding of these different regimes and the behavior of G10 currency pairs, this analysis will examine key macroeconomic factors frequently used as inputs for fair-value currency models.

- Interest Rates: Diverging interest rates between two countries can impact the relative value of their currencies;

- Economic Indicators: GDP, inflation rates and trade balances can influence currency prices; and

- Central Bank Policy Uncertainty: Monetary policies have a significant impact on currency prices, and unpredictable guidance can create price movements and trading opportunities.

Dispersion, Dispersion, Dispersion

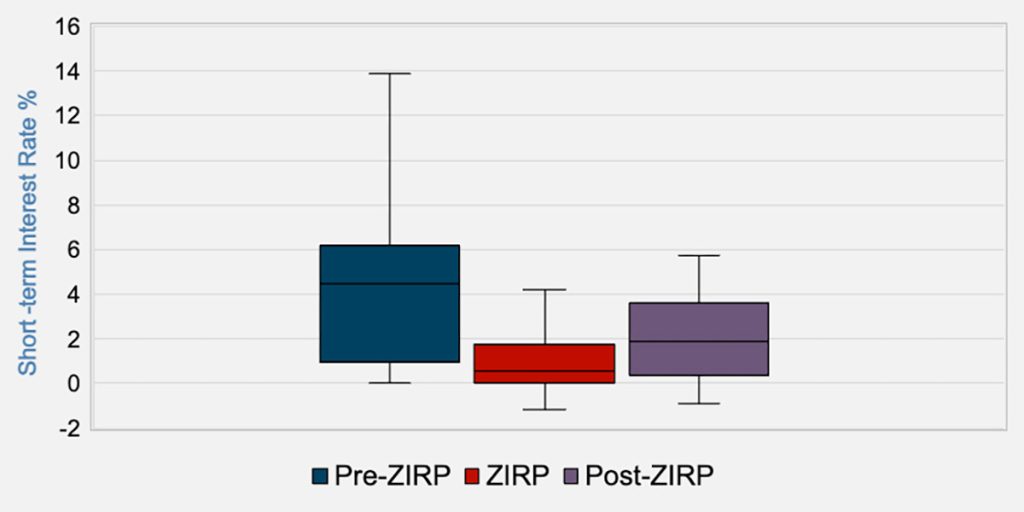

Figure 1: Interest Rate Dispersion: Jan 1990 to Jun 2023

The rate dispersion across our three distinct periods reveals notable differences. In the period before the global financial crisis and the consequent application of ultra-low interest rate policies, there was a notable divergence between major economies’ interest rates.

The 2008 GFC marked a substantial narrowing in rate divergence, as nations adopted zero or near-zero interest rates. In contrast, the post-ZIRP era has shown a renewed surge in rate differences, largely fueled by inflation dynamics.

Source: Macrobond

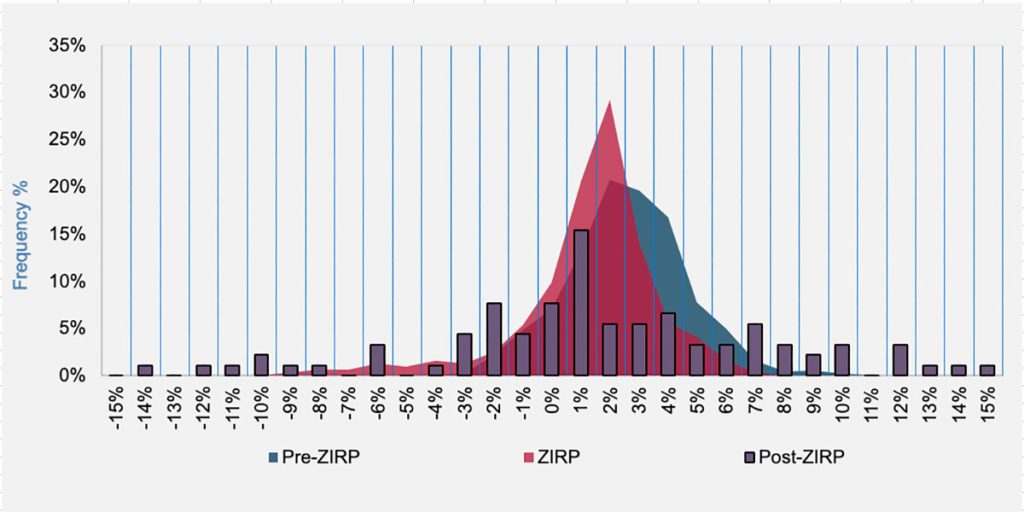

Figure 2: Annual GDP Distribution for G10 Currencies: Since 1990

The ZIRP era exhibited a narrow set of GDP growth rates concentrated around 2%. The GFC dealt a significant blow to economies worldwide, leaving most developed nations struggling to restore their growth prospects.

Contrastingly, the pre-ZIRP and post-ZIRP eras have exhibited a considerably broader span of GDP growth rates and, as we look at today’s macro landscape, dispersion is prevalent once again.

Source: Macrobond

- The U.S. has shown a strong economic recovery, aided by substantial stimulus spending and a strong labor market.

- Japan’s economy is showing resilience with ultra-low interest rates.

- Rising interest rates and falling house prices have hampered recoveries for Australia and New Zealand, but both are expected to benefit from higher commodity exports.

- The EU faces another potential energy crisis, financial sector weakness and the overhang of the Ukraine war.

- The UK is struggling with high inflation and life after Brexit and is especially vulnerable to interest rate rises.

These variances in recovery highlight that while some economies have adapted to the new normal, others are still navigating their way.

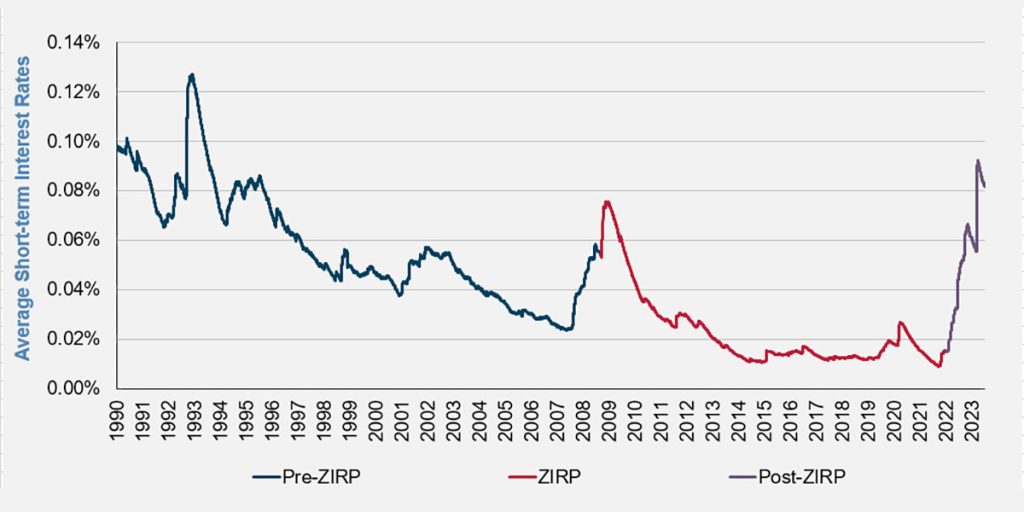

Figure 3: Central Bank Policy Uncertainty

Before ZIRP, there was significant volatility and frequent shifts in central bank policies, mainly due to global economies adopting diverse strategies to manage their idiosyncratic circumstances. The start of the GFC marked an initial jump in volatility, swiftly followed by a decline to historically low levels due to consistent forward guidance about maintaining zero-to-low interest rates.

Source: Macrobond

More recently, central banks have found it increasingly challenging to provide accurate guidance, largely due to the unpredictable nature of inflation. Consequently, the volatility associated with these financial instruments has soared, hitting highs not seen since the early 1990s.

Currency Strategies Are Back With a Vengeance

The global financial crisis led to an era of financial austerity whereby governments and central banks implemented measures aimed at reducing their debt loads and stabilizing their economies. This era was also marked by a period of range-bound and suppressed macroeconomic indicators notable for driving FX prices: inflation, interest rates, central bank policies and GDP figures. As these essential macroeconomic indicators became both more stable and more similar to each other, opportunities for directional currency trading strategies such as carry and trend were hard to come by. During ZIRP, there was a decade-long period during which carry and trend struggled in FX markets, bringing the period average performance for these strategies into negative figures, according to Deutsche Bank’s DB Currency Momentum and DB Currency Carry Indexes.

In the post-ZIRP period (through the end of 2023), currency trend and carry models within Aspect Capital have continued to demonstrate the return of opportunities. These have come from all corners of the globe, including regions such as Latin America, Eastern Europe and Asia, which joined more traditional currency behemoths such as the U.S. and Japan.

One notable trend developed in the Mexican peso, which consistently strengthened against the U.S. dollar over the last few years. Furthermore, the wide interest rate differential between the eurozone and Eastern European countries created a favorable carry environment, leading to strong opportunities in shorting the euro against the Hungarian forint and Polish zloty, as two examples.

The above examples highlight the diverse opportunity set this post-ZIRP period offers for systematic strategies, spurred by the recent divergence and dispersion of macro indicators that have once again led to a return to the robust performance we were accustomed to before ZIRP. As deglobalization, political instability and persistently wide-ranging inflation continue; and as central banks adopt different policies, the macroeconomic indicators essential to creating strong trend and carry opportunities have re-emerged, placing currency alpha once again among the core return drivers for systematic strategies.

Razvan Remsing is the global director of investment solutions at Aspect Capital. Ryan Horne is an investment solutions analyst at Aspect Capital.

This feature is to provide general information only, does not constitute legal or tax advice and cannot be used or substituted for legal or tax advice. Any opinions of the authors do not necessarily reflect the stance of Institutional Shareholder Services Inc. (ISS) or its affiliates.

Tags: Aspect Capital, foreign exchange, FX, interest-rate dispersion, macroeconomics, zero-interest-rate policy, ZIRP

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}