The NCAA is exploring potentially significant changes to its membership financial reporting system (MFRS), the accounting process by which schools annually disclose their athletic departments’ revenues, expenses and capital. While the association has made various tweaks to the MFRS over the last decade, there is increasing pressure to tackle long-standing criticisms about the system’s perceived shortcomings, as well as to address the dawning era of college athlete compensation.

Originally adopted in 2003, the MFRS is under new scrutiny in the wake of the House v. NCAA proposed settlement, which relies on the system to calculate both the past damages amount as well as the injunctive relief—athlete revenue sharing that would take place over the next decade. Which MFRS categories should be included in establishing the revenue “pool” has been the subject of recent debate among expert witnesses.

Beyond that, a number of MFRS categories lack clarity, leaving much interpretation to the schools, such as with the catch-all category “other operating revenue.” As Sportico previously reported, there’s so much wiggle room in the process that a handful of schools manage each year to claim a perfectly balanced budget, down to the dollar.

The last major changes to the MFRS came in 2015, following the recommendations of an NCAA financial data focus group that sought to eliminate broad interpretations and the renaming of certain revenue and expense categories, among other revisions.

Mario Morris, the NCAA’s chief financial officer, told Sportico that one of his main considerations is how the system could better specify athletic department expenditures that go directly to athletes, including cost-of-living adjustments and the “education-related” benefits provided for in the NCAA v. Alston Supreme Court ruling.

Overall, Morris says he thinks the current MFRS captures “75% to 80%” of an athletic department’s true economic picture but would like to find a way to “get it to 90%.” Morris, who previously served as executive deputy athletics director at Notre Dame, says he has received no shortage of input on this since arriving at the NCAA two years ago. He plans to continue to engage athletic department CFOs ahead of the governing body putting out its next version of financial reporting instructions by spring 2025. Those would then apply to the FY25 reports due by Jan. 15, 2026.

At the start of this year, the College Athletic Business Management Association (CABMA), a trade group under the umbrella of the National Association of Collegiate Directors of Athletics, formed a task force to present its MFRS-related recommendations to the NCAA.

“So many more people are going to be looking at this than ever before,” said Katie Davis, a partner at accounting firm James Moore & Co. who is helping to coordinate CABMA’s task force. “Both the NCAA and CFO groups need to go back to the drawing board and need to rethink things.”

James Moore & Co., which is contracted by a number of Division I schools, conducted a survey of athletic department business officers this year, in which the majority of respondents expressed a desire for greater clarity in the definitions of MFRS categories.

“There needs to be more consistent and clarified financial reporting so that those making decisions know what they are basing their decisions on,” she said. “You’ve got [college] presidents and chancellors at the table. You’ve got attorneys and lobbyists and all these others that maybe don’t fully understand what the financials are telling them, because it is not clear how the NCAA has defined some of the categories.”

For example, Davis cites Alston monies provided to athletes, which the MFRS instructions recommend being allocated towards “other operating expenses.”

The NCAA’s Morris concurs that schools’ financial reporting should better highlight the ways in which expenditures flow to athletes. “We have been able to provide a lot more benefits [to athletes] over the last 10 years,” Morris said. “We have gotten there in different ways.”

He cited as examples cost-of-attendance subsidies, the deregulation of meals, Alston benefits, NIL and revenue sharing. “We need to be able to tell that story,” he said.

Additionally, Morris says there is a lot of room for improvement in identifying the flow of money between schools’ main campuses and athletics. Currently, the MFRS has categories for “direct” and “indirect institutional support,” and a subcategory for the latter that breaks out athletic facilities debt service and lease expenditures. However, these categories allow for significant interpretation that make apples-to-apples comparisons between institutions nearly impossible.

The data collected from public universities’ MFRS reports serves as the basis of Sportico’s college sports finances database, as well as those compiled by USA Today and the Knight Commission on Intercollegiate Athletics (in conjunction with Syracuse University).

The NCAA does not itself publish the information, nor does it require its members to post their reports online, though some do voluntarily. Morris said that he would “personally” be in favor of the NCAA making the data public, “but it’s not my call.”

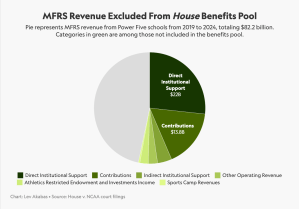

The proposed House settlement, submitted to a federal court in July, utilizes the MFRS in making two calculations, one for past damages and the other for the injunctive relief “benefits pool.” The revenue-sharing formula behind that pool includes only eight of the 19 MFRS revenue categories: ticket sales; game guarantees; media rights; NCAA distributions; conference distributions; conference distributions from football bowl revenue; royalties/licensing; and football bowl revenues.

Among the most significant excluded categories are “institutional or government support,” “other operating income” and “contributions.” Over the four-and-a-half-year period in which the revenue figures are being tallied, these excluded categories alone account for tens of billions of dollars in combined revenue.

Economist Daniel Rascher, the House plaintiffs’ expert witness, has previously explained in court filings that the decisions over which MFRS revenue categories should be part of the calculations were based on the “yardstick” of how the NFL, NBA and NHL calculate their league revenue in collective bargaining agreements with players.

In his calculation for potential damages, Rascher uses what he refers to as a “middle-ground approach,” and includes revenue from “programs, parking and concessions” and 50% of the contributions. (This category is referred to as “donations” in Sportico’s database.) Because schools include mandatory payments for season ticket privileges under donations, Rascher reasons that at least half of that money should be included.

Earlier this month, Ted Tatos, an expert retained by the plaintiffs’ in the rival Fontenot v. NCAA antitrust case, filed a declaration in the House case arguing for the “economic justifications” of including seven of the 11 MFRS categories that Rascher excluded.

The result of this would be to nearly double the revenue figure ($82.2 billion) from what Rascher ($46.4 billion) tallied, a figure Tatos argues is “artificially restricts college athlete compensation.”

Because Tatos didn’t have access to the MFRS reports for each Power Five conference member, he instead relied on financial data schools submit to the Department of Education for its Equity in Athletics Data Analysis (EADA). The MFRS is more detailed than—and generally considered superior to—the EADA.

In a reply declaration filed last with the court week, Rascher pushed back against Tatos’ dissent, contending his fellow economist “inappropriately includes categories of cash flow to athletic departments that are not revenue …in any sense comparable to the yardstick professional league revenues included in (CBAs).”

Davis, for her part, quibbles with the decision to include the NCAA distributions category, saying that much of that money is already being used on athletes to provide scholarships and Special Assistance Funds. Nevertheless, she commends the House settlement for the way it considered each of the various MFRS categories.

The settlement agreement requires that annual MFRS data will be provided to the plaintiffs’ lawyers by May 15 of each year and gives the class counsel the right to “reasonably audit” the reports. It also anticipates that significant changes to the MFRS could occur over the next decade, in which case the parties “will work in good faith to ensure accurate reporting of the revenue categories that are calculated to determine shared revenues and the pool.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}