Shriram Finance, one of India’s largest retail-focused NBFCs, has emerged stronger after a successful merger between group entities – Shriram Transport Finance and Shriram City Union in 2022. After a 10-year lull, where the stock went nowhere, it’s grown from ₹240/share to ₹650/share (2.7X) over the last 24 months.

With disbursements growing steadily and funding costs showing early signs of cooling, the company may be headed into its most profitable phase yet. Here’s why.

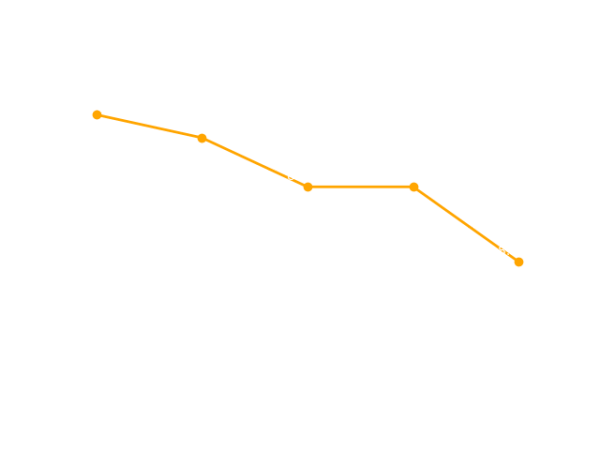

Easing Margin Pressure

Of late, Shriram Finance has experienced pressure on its net interest margin (NIM). Initially, this was due to lower lending yields from increased financing of new vehicles and a change in the loan portfolio mix with fewer gold and personal loans, which are typically higher yield loans.

Although the cost of funds has decreased slightly in recent quarters, it wasn’t enough to compensate for declining yields. More recently, excess liquidity resulting from a large foreign currency borrowing further compressed NIMs. Remember, net interest margins = interest yield – interest cost. NIMs are for financials what gross profit margins are for non-financial companies.

Source: Shriram Finance – Quarterly filings

Source: Shriram Finance – Quarterly filings

The company’s management, however, expects margins to recover as this excess liquidity is deployed and managed. Its focus on growing gold and MSME loans could also contribute to improved NIMs.

With the RBI shifting to a neutral policy stance and taking measures to improve liquidity, Shriram’s funding cost trajectory could reduce further—a positive for margins given its largely fixed-rate loan book. As interest rates go down but a large portion of total loans remain at fixed rates, NIMs expand. Exactly the outcome every Shriram Finance investor is hoping for.

Story continues below this ad

Growth Engine Intact

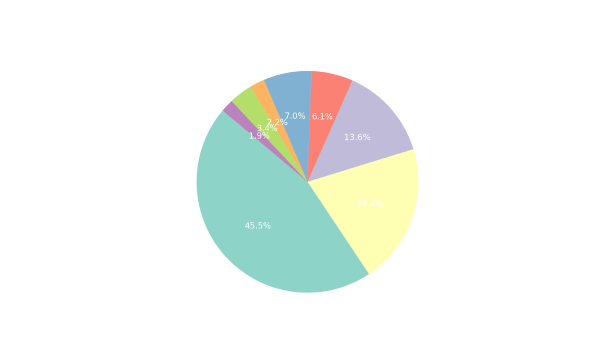

In 2022, Shriram Group merged its key lending arms—Shriram Transport Finance, Shriram City Union Finance, and holding company Shriram Capital—into a single entity: Shriram Finance Ltd. The move simplified the corporate structure, diversified the loan book beyond commercial vehicles to include MSME, personal, and two-wheeler loans, and enabled cross-selling across a unified branch network. Thus, creating a large diversified NBFC with 2.4 Lakh crore in total loans outstanding as of Q3FY25.

With commercial vehicle loan financing at 45.5% of the total loan book and trending downwards, benefits of the merger are beginning to emerge.

Source: Shriram Finance – Quarterly filings.

Source: Shriram Finance – Quarterly filings.

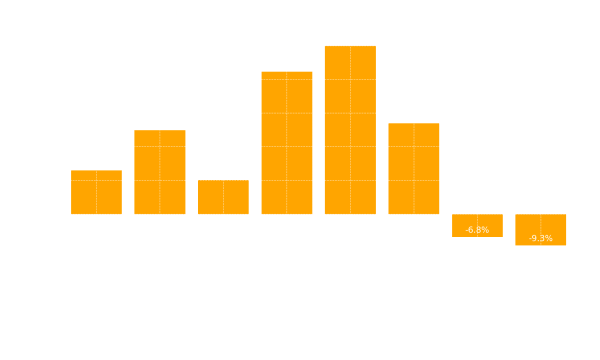

For one, the management has the flexibility to grow the overall pie without having to rely exclusively on commercial vehicle loan growth. This is evident from the Q3FY25 segment growth number.

Source: Shriram Finance – Quarterly filings

Source: Shriram Finance – Quarterly filings

Shriram Finance clocked a 15.8% YoY rise in disbursements in Q3 FY25, driven by strong momentum across used vehicles, MSMEs, passenger vehicles, and two-wheelers.

Story continues below this ad

Commercial Vehicle (CV) lending, still the largest segment at 45% of AUM, is riding a multi-year tailwind from rising ticket sizes and high resale values. Passenger vehicle finance, now 20% of AUM, is scaling rapidly, with management targeting over 20% annual growth. MSME loans, at 14% of AUM, are still being rolled out across branches, offering untapped growth. Two-wheeler loans grew 17.7% QoQ in Q3, outpacing market growth by 3x. With fleet utilization at peak levels, credit costs under control, and cost-to-income stable around 28.6%, Shriram’s diversified book is geared for continued high-teens AUM growth.

Asset Quality

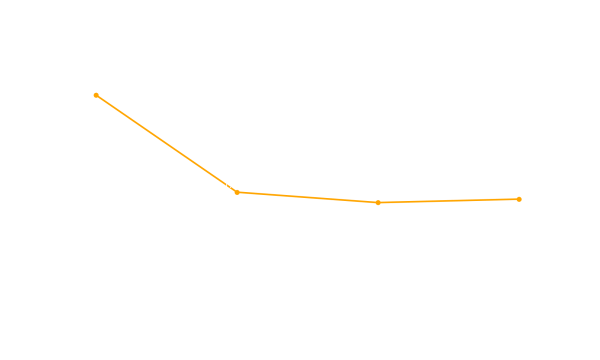

More importantly, this growth is not coming at the cost of poor underwriting standards. At least for now. Overall Gross Non-performing Assets (GNPA), percentage of loans that are due by more than 90 days, has inched up marginally from 5.32% to 5.38%, but on a YoY basis, it is down from 5.66%.

Since the Commercial Vehicle segment dominates the loan mix at 45% of total loans, asset quality in the CV segment, typically considered higher risk, determines the NPA ratios of the overall portfolio.

Although the overall CV portfolio GNPA stood at 5.38%, Shriram’s core used vehicle sub-segment, which likely makes up 70%+ of the CV book, has consistently delivered sub-2% credit cost for over a decade, according to executive vice chairman of Shriram Finance, Umesh Revankar.

Story continues below this ad

Source: Shriram finance – Quartery filings

Source: Shriram finance – Quartery filings

According to a CRISIL credit rating report, dated February 28, 2025, “The company is expected to continue to retain its predominant market position in the pre-owned CV financing business and the SME loan segment… the company faces limited competition from other organised financiers, including banks, in this segment, due to inherent riskiness of the target product and the customer profile. In the SME loan segment, the company is a leading financier among retail NBFCs.”

PAT & Profitability Trends

Q3 FY25 PAT surged 96% YoY to ₹3,570 crore, aided by a one-time post-tax gain of ₹1,489 crore from the sale of Shriram Housing. Adjusted PAT still grew at a healthy 14.4% on a yearly basis, although this is not a standout result given that peers have grown better.

Source: http://www.screener.in

Source: http://www.screener.in

ROE – Return on Equity could trend higher toward historical pre-merger levels of 17–18% if margin expansion and cost efficiencies play out as expected.

Source: Shriram Finance – Quarterly filings

Source: Shriram Finance – Quarterly filings

Valuation: Compelling Relative Play

Story continues below this ad

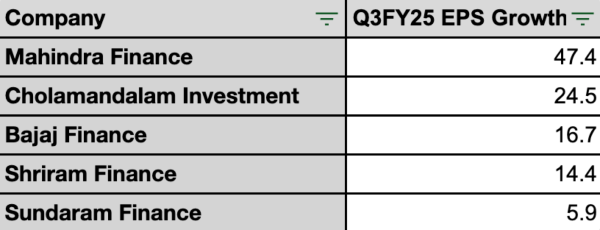

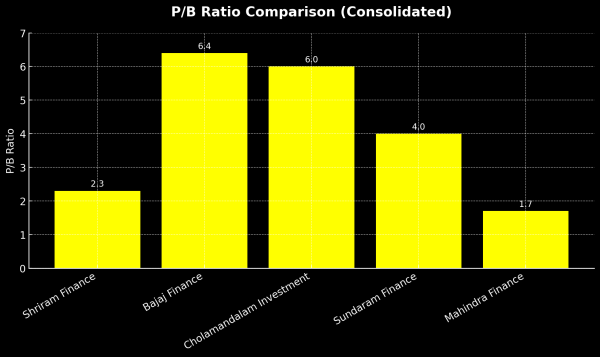

Despite its scale and profitability, Shriram trades at just 2.3x book. Compared to five large NBFCs, this is lower than valuations of Bajaj Finance, Cholamandalam Investment, Sundaram finance.

Source: http://www.screener.in

Source: http://www.screener.in

Perhaps this is justified. Bajaj and Chola deliver higher ROEs (>20%) than Shriram Finance. EPS growth of three out of five large NBFCs in Q3FY25 is higher than Shriram Finance’s EPS growth. Even the asset quality is not as pristine compared to peers, given its business model differs from large NBFC peers. So, there are challenges in making an apple-to-apple comparison, but where ROE, EPS growth, and asset quality stand today, one can argue that current valuations might be justified.

However, if margins rebound post-rate cuts and credit costs stay benign, ROE could trend toward 18%, making a 2.5-3.0x book multiple reasonable.

In conclusion, Shriram Finance is no longer just a truck lender. It’s a diversified, tech-enabled retail credit platform with strong underwriting, improving asset quality, and high-teens growth. With the rate cycle turning, it may be one of the better-positioned NBFCs to expand margins and deliver on profitability. For investors seeking growth without paying 6x book value, Shriram Finance might just be the sweet spot.

Story continues below this ad

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Rahul Rao has been investing since 2014. He has helped conduct financial literacy programs for over 1,50,000 investors. He helped start a family office for a 50-year-old conglomerate and worked at an AIF, focusing on small and mid-cap opportunities. He evaluates stocks using an evidence-based, first-principles approach as opposed to comforting narratives.

Disclosure: The writer or his dependents do NOT hold shares in the securities/stocks/bonds discussed in the article.

Story continues below this ad

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}