Overview

In the dynamic landscape of the UK hotel sector, 2023 was a testament of the market’s resilience amidst challenges, with UK hotels showing significant surge in key performance metrics. Throughout the year, London in particular witnessed a boom in development projects with office-to-hotel conversions particularly popular.

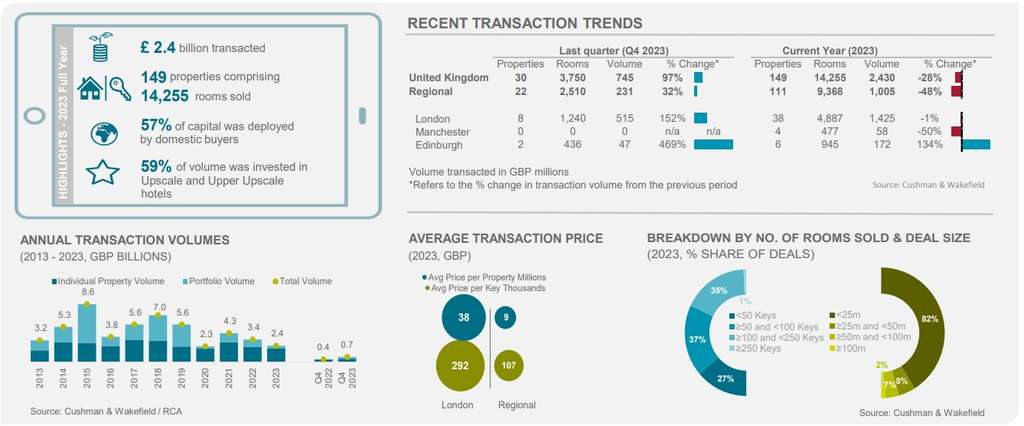

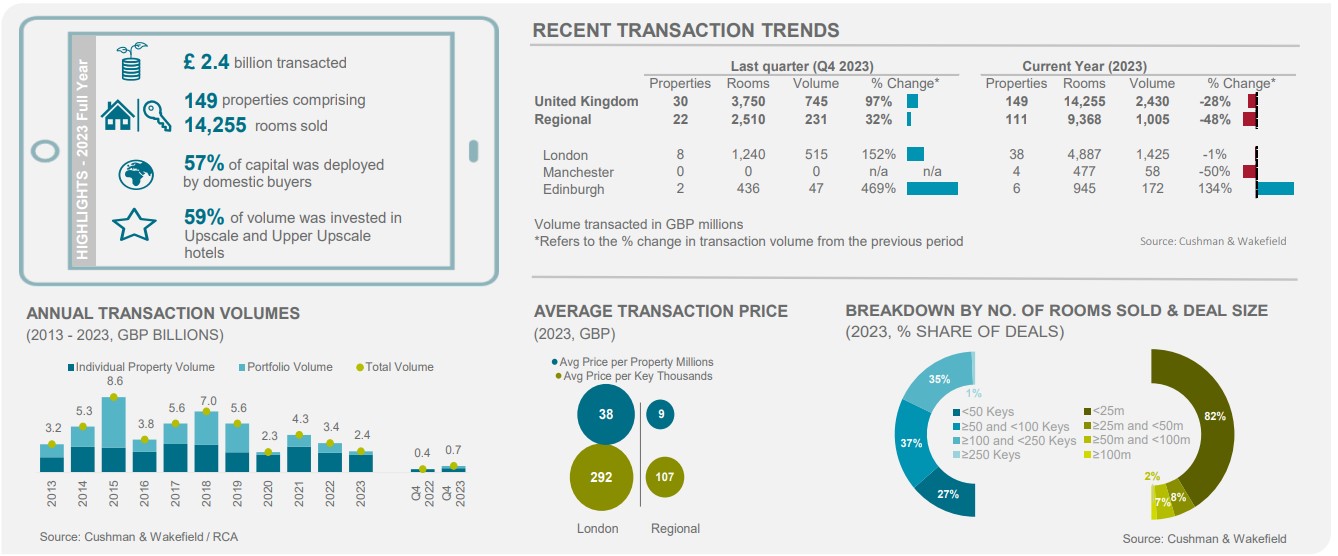

Investment volumes reached £2.4bn¹, experiencing a 28% decrease from 2022 levels, albeit this is less of a decline than other commercial real estate asset classes. Over £0.5bn of this investment was aimed at converting offices to hotel – the prime location of many office buildings, coupled with the desire to maximise underused real estate and the growing demand for hotels, have all played a role in fuelling this trend.

Intensified competition for prime opportunities alongside the expected movement of base rates this year should see a clear slowing down in the outward movement of hotel yields. We expect to see an increase in deal flow in 2024, driven by refinancing events and a narrowing bid:ask spread. As market dynamics continue to evolve, market leaders anticipate a vibrant period of growth in the UK hotel sector and a reversion to a more “normal” level of deal activity.

Investment Trends

The market continues to experience constrained deal flow, largely as a result of the mismatch between sellers holding out for prices based on buoyant trading whilst buyers struggle given the far higher cost of debt. The bid:ask spread is showing signs of narrowing whilst macroeconomic uncertainties dissipate. In 2024, we expect to see an uptick in deal activity as this gap narrows and refinancing events stimulate the market.

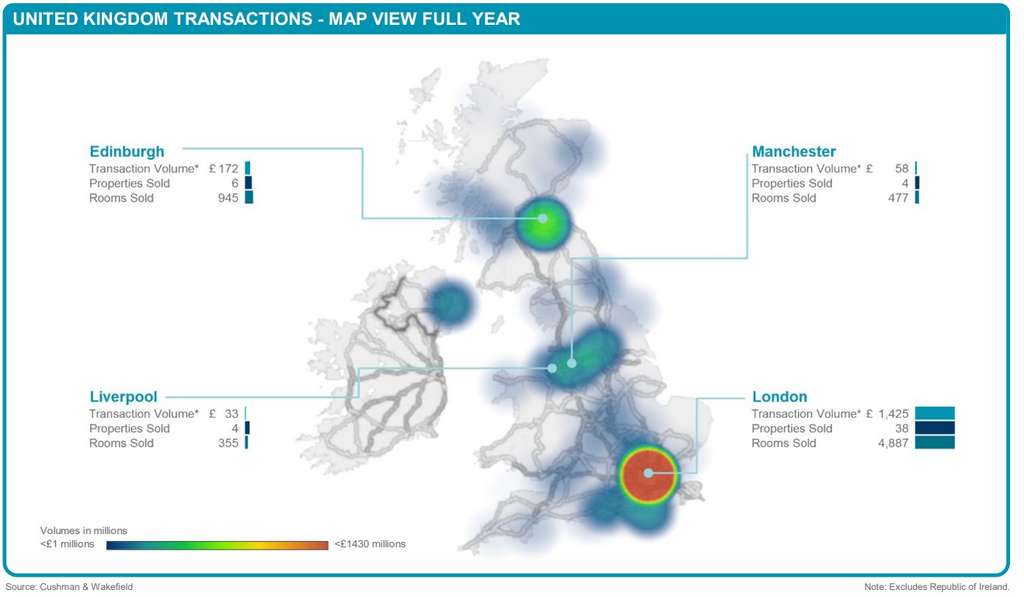

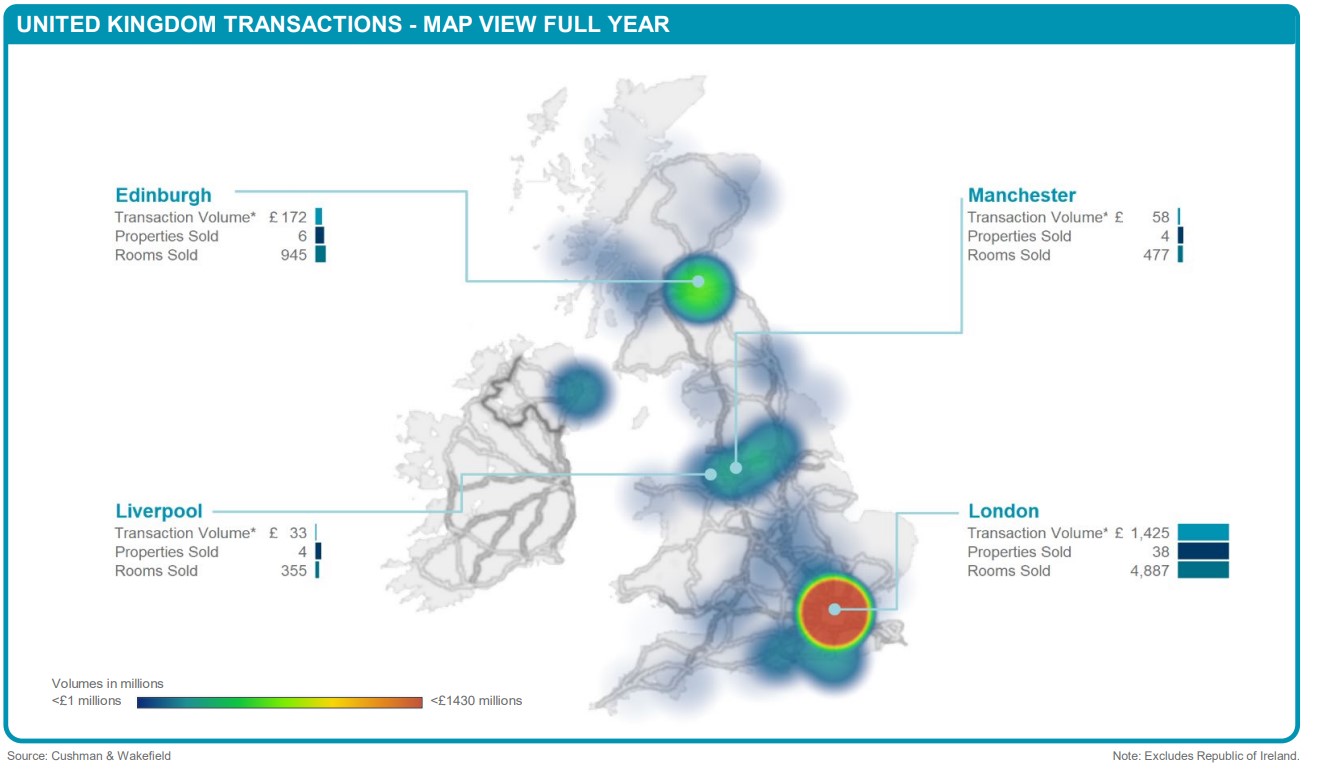

The overall volume covered 149 properties across the UK, representing 14,255 individual rooms. While the overall annual volume of deals was down compared with 2022 (£3.4bn), the final quarter of 2023 (£745m) was 97% up on the same period 12 months earlier (£379m).

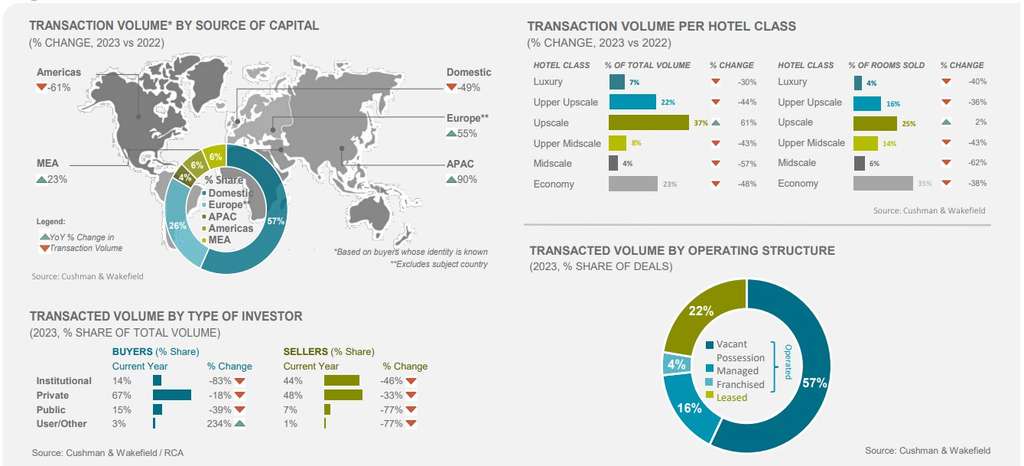

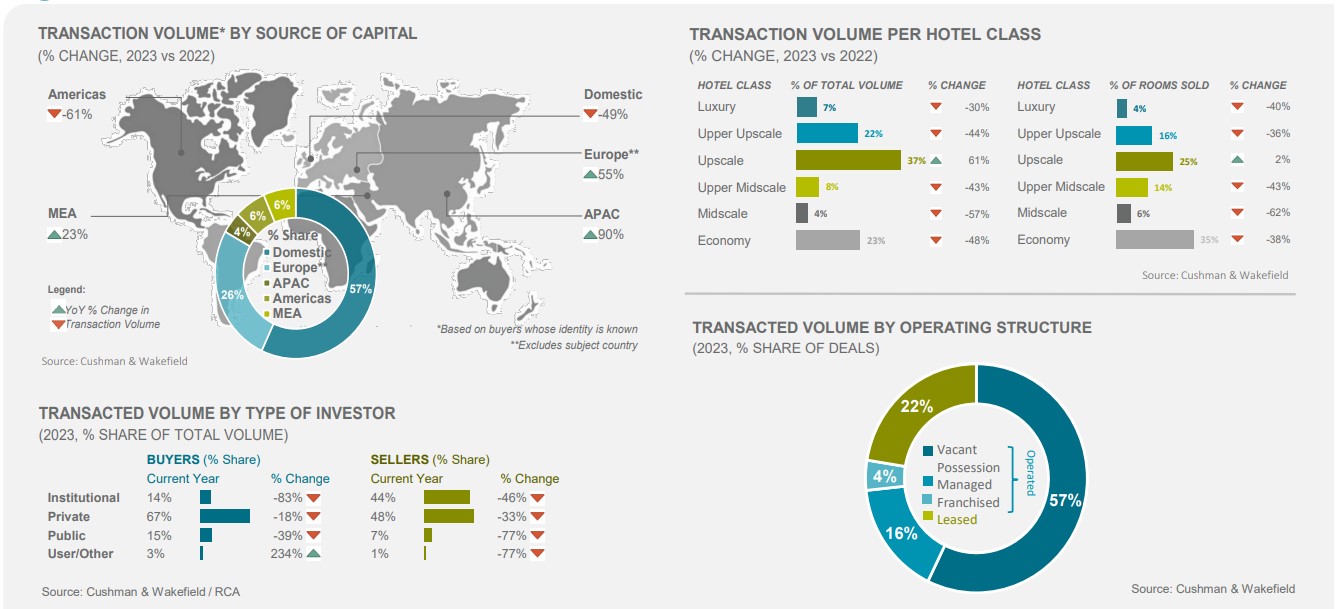

In terms of capital deployed, private buyers were the dominant force in deals completed at 67%, while institutional-backed capital (14%) shrank dramatically compared with the previous year. Domestic buyers represented more than half of deals, followed by those from Europe (26%).

Prime Yields

Yields present a nuanced landscape, sitting generally 75-100 basis points softer YoY. The persistent “flight to quality” remains dominant, intensifying competition for prime opportunities and supporting persistently tight yields for the best quality product. Base rates are anticipated to move in during the second half of 2024 after which a gradual sharpening of yields should be expected.

Market Performance

As of December 2023, the UK hotel industry has witnessed a remarkable upswing in performance. ADR over the LTM stood at approximately £120 (+26% on 2019) indicating a real growth of 6.1%. Occupancy sits 40 bps behind 2019 and is expected to fully recover by mid-2024. Despite the real RevPAR growth of 5.9% since 2019, the spread between RevPAR and GOPPAR has widened due to pressures on the cost base.

Supply Outlook

UK-wide room supply grew +0.7% YoY at December 2023, in contrast to a 5.8% growth in room nights. Office to hotel conversions have delivered a number of opportunities for developers, especially within key markets like London and Edinburgh which will drive additional supply growth looking forward. In certain markets, room supply will see additional growth as hotels come back online following the conclusion of several government asylum contracts.

Demand Outlook

Hotel overnights are projected to surpass 2019 levels by 2024, with domestic overnights leading the recovery. The easing of inflation, wage growth and relatively low unemployment, has contributed to an increase in consumer spending throughout 2023 and is anticipated to persist into 2024. Cross-continental demand recovery, especially from Asia and the US, should provide further support to this upward trajectory.

Cushman & Wakefield’s Hotel Market Beat reports provide an overview of the hospitality sector trends, with a focus on hotel transaction activity. These reports are available on a pan-European level as well as for the key hotel markets within Europe.

Note¹: Note: A contingency of 5% is assumed for transactions in the last 12 months, as some deals are revealed with notable delay.

About Cushman & Wakefield

Cushman & Wakefield (NYSE: CWK) is a leading global commercial real estate services firm for property owners and occupiers with approximately 52,000 employees in approximately 400 offices and 60 countries. In 2022, the firm reported revenue of $10.1 billion across its core services of property, facilities and project management, leasing, capital markets, and valuation and other services. It also receives numerous industry and business accolades for its award-winning culture and commitment to Diversity, Equity, and Inclusion (DEI), Environmental, Social and Governance (ESG) and more.

To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter.

Jack Wallsworth

Associate

+44 207 152 5803

Cushman & Wakefield

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}