Both European and US markets are on track to end the week higher, while Asian markets remain mixed due to different economic landscapes.

In Europe, the DAX reached a new high on Thursday following the ECB’s third rate cut of the year, and Wall Street continued its uptrend, driven by solid company earnings.

Chinese stock markets, however, extended their decline as additional stimulus measures failed to meet market expectations.

Europe

European benchmarks are higher for the week, with the Euro Stoxx 600 rising by 0.98%, Germany’s DAX climbing by 1.08%, and France’s CAC 40 gaining 0.08% over the past five trading days.

The British FTSE 100 also saw an increase of 1.59%, supported by strong gains in banking stocks, following positive earnings results from US banks.

At the sector level, financials and industrials led the broader gains, as banking stocks surged on the back of optimism surrounding US earnings, and the defence sector continued to rally amid uncertainty in the Middle East.

In contrast, the consumer and technology sectors underperformed, driven by significant drops in shares of LVMH and ASML following disappointing third-quarter earnings results.

Airbus shares soared by more than 12% this week due to rumours of a major order from Etihad Airways and an upgrade by JP Morgan, which also lifted shares of Rolls-Royce, resulting in a 7.3% rise over the week.

Additionally, major European banks, including HSBC, UBS, BNP Paribas, and Barclays, all posted gains ranging between 1% and 4%.

On the earnings front, ASML reported its results a day ahead of schedule, revealing that its key metric—bookings—fell well short of analysts’ expectations.

Its shares plummeted 16% on Tuesday, marking the largest single-day drop in 26 years. The Dutch firm also downgraded its 2025 guidance, citing weaker demand, potentially linked to China export restrictions.

LVMH similarly reported a revenue decline for the first time since 2020, attributed to a slowdown in Chinese consumer demand, leading to a 7% decline in its shares over the week.

The euro weakened further against the US dollar following the widely anticipated ECB rate cut. The EUR/USD pair fell to just above 1.0830 during Friday’s Asian session, its lowest level since 5 August.

Eurozone inflation was revised down to 1.7% year-on-year from the initial estimate of 1.8% in September, reinforcing expectations of an accelerated ECB rate-cut cycle.

ECB President Christine Lagarde stated: “We are breaking the neck of inflation.”

Wall Street

US stock markets will also likely end the week in positive territory, buoyed by strong corporate earnings and resilient economic data.

US tech earnings began with Netflix, which exceeded market expectations across all major metrics, resulting in a more than 5% rise in its share price during after-hours trading.

This optimism is likely to continue propelling Wall Street into Friday’s session.

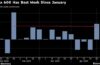

Over the past five trading days, the Dow Jones Industrial Average increased by 0.88%, the S&P 500 rose by 0.46%, and the Nasdaq Composite gained 0.17%.

Within the S&P 500, six out of eleven sectors posted weekly gains, with sectors that benefit from lower interest rates, such as utilities and real estate, leading the charge—up by 2.49% and 1.34%, respectively.

On the other hand, technology and energy stocks underperformed, both falling by over 1%.

Nvidia shares reached an all-time high earlier in the week but retraced some of their gains as the US pledged to continue restricting chip exports to China, despite continued strong demand for artificial intelligence GPUs.

Most semiconductor stocks fell this week, following ASML’s sharp decline, as regulatory challenges weighed on sentiment.

Investors are expected to closely monitor upcoming quarterly earnings reports from major tech firms in the next week or two.

Morgan Stanley also reported robust third-quarter results, with its shares climbing by more than 9% over the week.

The investment bank’s profit surged by 32%, driven by strong performance across its wealth management, equity trading, and investment banking divisions.

Asia-Pacific

Stock markets in the Asia-Pacific region were mixed this week, with Japanese and Chinese markets in the red, while Australian markets remained in positive territory.

On a weekly basis, the Nikkei 225 declined by 1%, the ASX 200 rose by 0.8%, and the Hang Seng Index dropped by more than 4%.

China’s housing ministry briefings failed to meet expectations, leading to a continued retreat in regional equity markets.

However, stronger-than-expected GDP growth, along with better-than-expected data for retail sales, industrial production, and fixed asset investment in September, led to a broad rebound in Chinese markets on Friday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}