Growing and protecting your savings on the path to retirement is a venture well-served by “setting and forgetting,” putting the money in and not thinking about it as best you can as you attend to work and family and the rest of daily life.

Market fluctuations can make that state of inattention harder to attain and maintain, especially when the market crashes, as it has in the past and surely will again. Sure, the bull market is back. But what can you do to stay bullish on your retirement strategies when the bears roar once more?

Below are three retirement hacks to consider.

Image source: Getty Images.

Hack 1: Diversify to spread the risk and effect

Diversifying among asset classes is a great first step. While it can be tempting to simply buy certificates of deposit (CDs) or keep money in savings accounts, these guaranteed funds are also just about guaranteed to badly trail inflation as the years go on, and simply can’t be expected to keep up with the stock market in terms of total return.

Meanwhile, the volatility of high-growth stocks can prove less appealing as your retirement window grows shorter, leaving less time to recover from losses and take advantage of gains. Diversifying along the way is as close to a panacea as you can get here.

A mix of well-chosen stocks, bonds, cash, and real estate, for instance, mitigates your risk from exposure to any single type of investment while providing steady growth to your bottom line and raising the bottom for what a market crash might do to your nest egg.

Hack 2: Dollar-cost averaging and the Rule of 72

Dollar-cost averaging is a simple but effective strategy. The idea is that you invest a fixed amount on a regular basis, regardless of the investment’s cost. Millions of employees are doing that right now by funding 401(k)s, IRAs, and similar retirement plans.

For example, say you invest $100 every pay period in a certain mutual fund. When the market is down, you get more. When it’s higher, less. In the end, you are averaging your cost of investment.

Historically, the market trends up, and you don’t have to be an expert stock picker, either. Since its launch in 1993 as the first U.S.-listed exchange-traded fund, State Street’s SPDR S&P 500 ETF (SPY -0.13%) has provided a compound annual return of 10% by simply replicating the performance of that major index.

At a 10% fixed rate of return, a dollar invested now becomes about $10 in seven years. That’s the Rule of 72. If you invest $100 a month, say $50 a pay period, without fail for 30 years, you can expect to have about $217,000 at that rate.

Dollar-cost averaging combines that potential with the wealth-growing power of disciplined savings, building your nest egg through market gyrations.

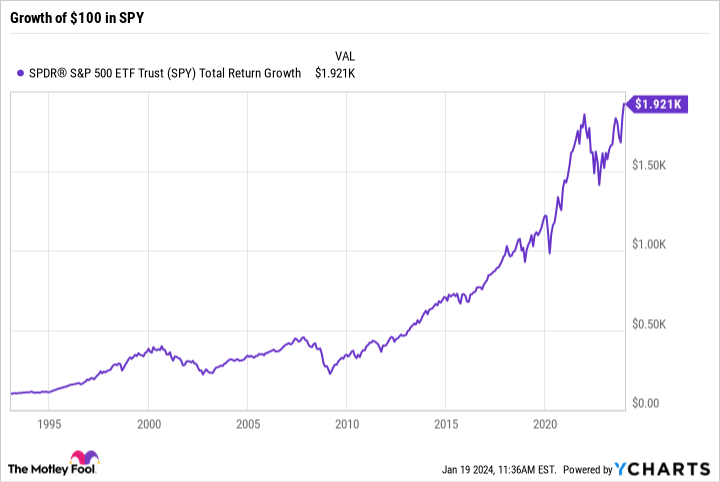

SPY Total Return Level data by YCharts

The chart above shows how a $100 investment made in that ETF when it launched — and neither added to nor drawn from since then — has grown to nearly $2,000. Add to it regularly through good markets and bad, and you’ll have a lot more.

Hack 3: The power of an emergency fund

Creating an emergency fund, one specifically designed to meet at least six months’ worth of living expenses, is a great idea for both your working and retirement years. Having one in place can help ensure you don’t have to drain retirement savings when unexpected expenses pop up, as they can be expected to do.

This is one account you might consider keeping in your less volatile investment choices, including cash, to ensure you have available what you need if the emergency arises during a bear market, allowing your retirement-dedicated investments to continue undisturbed.

Bearing with the booms and busts

As in investing in general, your approach to dealing with market booms and busts when it comes to saving for retirement depends on your appetite for risk and your timeline and plans for that day and beyond.

That said, diversifying your portfolio, practicing dollar-cost averaging, and maintaining a dedicated emergency fund can fortify your financial future against market crashes and position you to see nice gains during the upswing.

Remember, financial resilience in retirement is the result of proactive measures taken long before your working days end. These three hacks deserve consideration among them.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}