Can this semiconductor equipment giant come out of its latest slump and become a winner over the next five years?

ASML Holding (ASML -3.11%) is a critical player in the semiconductor industry, as chipmakers and foundries use its equipment to manufacture chips. That explains why the Dutch semiconductor equipment giant has clocked impressive gains on the stock market in the past five years.

The robust demand for ASML’s chipmaking equipment to fulfill the growing need for semiconductors has led to a nice jump in its revenue and earnings, as seen in the preceding chart. The good part is that ASML seems built for more growth over the next five years, as the demand for its offerings remains solid amid the artificial intelligence (AI) boom. This became evident from the company’s results for the second quarter of 2024, released on July 17.

Let’s take a closer look at ASML’s latest quarterly performance and check why investors can expect more upside in this semiconductor stock over the next five years.

ASML sees big boost in bookings but investors still hit the panic button

All eyes were on the bookings ASML received in the second quarter, and that figure of 5.6 billion euros was well ahead of analysts’ expectations of 4.41 billion euros. ASML’s bookings stood at 4.5 billion euros in the same quarter last year and 3.6 billion euros in the first quarter of 2024.

So the company’s order book increased nicely last quarter, both sequentially and on a year-over-year basis. It’s worth noting that ASML received 2.5 billion euros’ worth of orders for its extreme ultraviolet (EUV) lithography machines last quarter, accounting for almost half of its total orders for the period.

These EUV machines are used for making advanced chips based on smaller process nodes, which are capable of delivering high computing power while consuming less electricity. Foundries and chipmakers are using these EUV machines to churn out AI chips, which explains why its EUV bookings increased by 56% on a year-over-year basis, contributing to a sizable backlog worth 39 billion euros.

However, investors pressed the panic button following ASML’s results for a couple of reasons and the stock fell 12%. First, the company’s revenue outlook of 7 billion euros for the current quarter is lower than the Street estimate of 7.5 billion euros. Second, concerns about restrictions on ASML’s sales to China have also contributed to the sell-off in ASML stock following its latest results.

That’s because China accounted for almost half of ASML’s top line last quarter, and the demand for the latter’s older equipment is strong in that country. So reports that the Biden administration is considering imposing stricter restrictions on sales of semiconductor technology to China are weighing on ASML stock.

Investors shouldn’t miss the bigger picture

Investors would do well to take a look at the broader picture, as the healthy demand for AI chips over the next five years should allow ASML to overcome any potential loss of business in China should stricter sanctions be imposed. The global AI chip market is expected to generate $296 billion in revenue in 2030, growing at an annual rate of 33% during the forecast period. This should create demand for more EUV lithography equipment.

According to Market Digits, the EUV lithography market could generate $37 billion in revenue in 2030, compared with $9 billion last year. ASML has a monopoly in EUV lithography machines, which means that it is set to enjoy robust incremental revenue growth as this market expands in the long run.

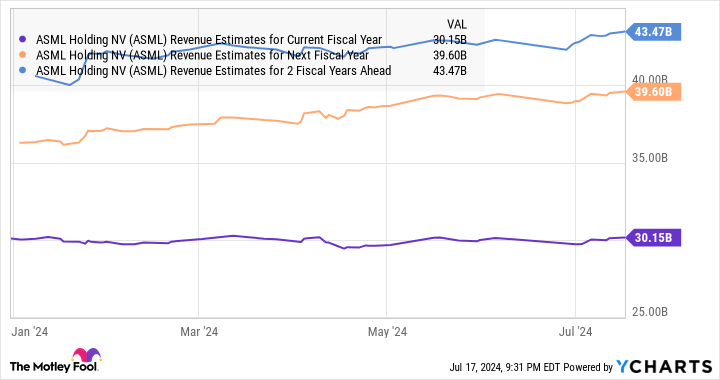

Moreover, ASML is expecting to return to growth in 2025 following a flat revenue performance in 2024, driven by the recent recovery in the semiconductor market which is fueled by catalysts such as AI. Analysts are expecting its top line to increase 3% in 2024 to $30.2 billion, but the forecast for the next couple of years is quite solid.

ASML Revenue Estimates for Current Fiscal Year data by YCharts

ASML should be able to sustain such healthy growth for a longer time considering the long-term opportunity in the AI chip market. Analysts are expecting its earnings to increase at a compound annual growth rate of 21% for the next five years. However, ASML’s earnings are expected to grow at a much faster pace in 2025 and 2026 following a small decline in the current year from last year’s levels of $21.22 per share.

ASML EPS Estimates for Current Fiscal Year data by YCharts

There’s a good chance that ASML could grow at a faster pace than analysts’ expectations over the next five years on the back of AI-driven demand for its chipmaking equipment, and that could lead the market to reward this AI stock with healthy gains. That’s why investors would do well to capitalize on the drop in ASML stock following its latest earnings report, as it could bounce back and soar higher in the long run thanks to the catalysts I’ve discussed.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ASML. The Motley Fool has a disclosure policy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}