Ask any City adviser whose bread and butter is arranging stock market flotations what the past three years have been like and you will get similar answers.

“It’s been tough,” was the verdict of a senior lawyer who advises on initial public offerings. “Pretty hard going,” was how a veteran investment banker, who focuses on equity capital markets, summed up the dearth of listings.

There are tentative signs, however, that business may pick up. On October 7 Applied Nutrition, based in Liverpool, confirmed its intention to float on the London Stock Exchange in a deal that could put a £500 million valuation on the maker of protein products and energy drinks for professional athletes and fitness fanatics.

Ebury, a British payments business that is backed by Santander, also increased its preparations for a potential London listing next year that could give it a market capitalisation of £2 billion with the appointment of Bruce Carnegie-Brown, a City veteran, as its chairman. Similarly, the owners of Canopius are considering a possible IPO of the Lloyd’s of London insurer.

Then there is Shein, the giant fast-fashion group, which is eyeing a London listing that could give it £50 billion price-tag. The prospect of Shein, which is based in Singapore, joining London is already attracting scrutiny amid worries about labour practices in its supply chain but if the deal happens it could be Britain’s largest ever IPO.

“It’s a slow pick-up but you can definitely feel that it is heading that way,” the lawyer said.

Company flotations are a central feature of the capital markets. Deals by businesses to list their shares on the stock exchange are an important fundraising tool for companies that also provide their existing investors with a means to crystallise gains by selling stock. Listings also bolster the wider City ecosystem by generating lucrative fees for the bankers, lawyers, accountants and other advisers that orchestrate IPOs. Then there is the prestige it brings to Britain’s financial services sector when a big foreign company picks London as the place to go public.

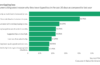

There has, however, been a slump in flotation activity since the post-Covid boom in IPOs faded away in autumn 2021, a year when 126 businesses made their debut in London through deals that raised a combined £16.7 billion, according to data from the stock exchange. The number of listings shrank to 45 the following year, when £1.6 billion was raised, and 23 IPOs that raised £953 million in 2023.

The decision by the Japanese conglomerate Softbank to float the Cambridge-based microchip designer Arm on Wall Street rather than London in September last year, despite lobbying by the British government, was a particular blow. The IPO valued Arm, a FTSE 100 business before Softbank bought it for $32 billion in 2016, at $52.3 billion, cementing its status as one of the UK’s most successful technology companies.

Applied Nutrition has confirmed its intention to float in London

APPLIED NUTRITION

This decline in flotation activity has fuelled worries both in government and among some City advisers that London has lost its appeal as a listing venue, particularly compared with rival markets overseas such as New York and Amsterdam, where companies that list can potentially clinch higher valuations. It has also come to epitomise broader concerns about the health of the UK’s wider capital markets and the competitiveness of London as an international financial centre. As well as the faltering IPO market, several companies that were already quoted have recently dropped London as their primary listing in favour of New York to bolster their valuations.

Still, some argue that worries about London are overdone. The flotation market is not completely closed, with 11 businesses listing in London so far this year, raising a combined £586 million through small deals. They have included Raspberry Pi, a maker of pocket-sized computers, and Aoti, a developer of wound care products. Thomas Ryder, the chief executive of Applied Nutrition, said the London market was “the obvious choice” for his business, even though it sells its products in more than 80 countries.

Furthermore, other exchanges overseas have also experienced relatively muted IPO volumes. “If you look at Europe, including Germany and France, they have had a tough 2024 for IPOs as well, it’s not like the UK’s on its own,” James Fleming, the head of UK investment banking and broking at the Wall Street lender Citigroup said.

Raspberry Pi is among the companies that raised funds in London

RASPBERRY PI

Still, worries about the UK market are serious enough to have pushed the government and the Financial Conduct Authority, the City regulator, into a series of reforms to loosen the listing rules to make London more attractive. These have included easing the free-float requirements and restrictions on dual-class share structures in late 2021, and a much wider overhaul of the listing rulebook that came into force in late July and was billed by the FCA as the biggest revamp in decades.

This most recent overhaul has been criticised by some investor groups for stripping away protections for shareholders, thereby denting the UK’s reputation for high corporate governance standards. Nevertheless, City advisers credit it with helping to stimulate London’s IPO pipeline.

“The UK reforms, in a European context, have made it as competitive as the rest of the region,” one of the bankers who spoke to The Times said. The recent fall in inflation was also putting IPOs back on the table, he added. “We’ve been through quite a turbulent period from an earnings perspective. You never want to IPO until you’ve got confidence in your forward-year growth expectations.”

Eagerness among private equity firms to offload companies is another driver. Listings, one exit avenue traditionally pursued by buyout houses, have been stifled partly by market volatility, which has been driven both by the rapid increase in interest rates since late 2021 and geopolitical turbulence. These factors have, until recently, also made it harder for private equity houses to sell businesses, either to other buyout firms or trade buyers.

This means private equity houses have been holding on to some companies for longer than they had planned and face pressure from their investors to exit these investments and return cash.

“The desire of private equity firms to monetise investments is a big driver of future IPO supply,” Fleming said.

Still, some City fund managers are wary of buying into companies that are listed by buyout houses, not least because shares in a number of the businesses floated by private equity firms during the 2021 boom have underperformed. UK-focused stockpickers also face pressures of their own.

“I don’t know anyone who hasn’t got outflows in the mid- and small-cap space,” one veteran fund manager said. “If we have money in the market then we’ll get lots [of IPOs], but without capital we won’t.

“All the debate around listing rule changes is all very well, and it helps, but if you haven’t got any money it’s irrelevant. It’s like getting a plumber to fix something when actually you haven’t got any water supply: it’s a waste of time.”

Despite this, financiers are cautiously optimistic that the flotation market will improve. “I can see four to five £1 billion-plus IPOs in the UK in the next 18 to 24 months,” predicted Fleming, with £1 billion being the amount raised, rather than market valuation.

One of the other bankers said he was “confident there will be more next year than there were this year”, although he added with a laugh: “That gives a low bar to chin.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}