Is the Strait of Hormuz open or closed? Depending on the day (or hour), you might get a different answer from the governments of Iran and the United States. In what the International Energy Agency has described as the largest oil supply disruption in history, the transport of oil and natural gas from the Persian Gulf has been greatly impeded due to the ongoing conflict between the United States and Iran.

Markets don’t seem to care anymore. Crude oil prices have come back down somewhat, though they are still well above where they began the year, and the S&P 500 index has just made all-time highs. Here’s how markets have handled the energy supply disruption so far, and what the conflict could mean for the stock market in 2026.

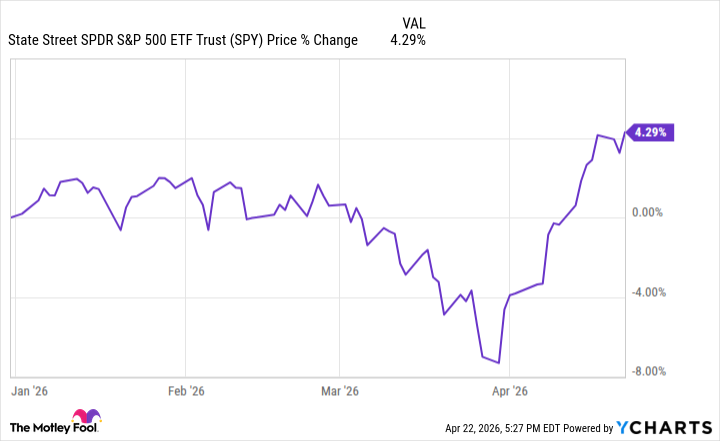

A stock market bounce-back for the ages

Crude oil prices began rising in late February before spiking to above $110 a barrel in early April, when Iran’s blockade of the Strait of Hormuz intensified. Now, with a temporary ceasefire in place, oil prices have fallen back to between $90 and $100 as of this writing on April 22, even as Iran and the United States continue to engage in blockades while also pursuing negotiations.

The stock market clearly believes that the conflict will end soon. After entering correction territory in April, both the S&P 500 index and Nasdaq-100 index have gone on to record some of their best 10- to 15-day return periods in history. Right now, the S&P 500 is up 4.3% year to date.

Image source: Getty Images.

Differences between past energy shocks

Back in the 1970s and early 1980s, Middle East oil embargoes and rapidly rising oil prices shook the U.S. economy to its core, causing steep inflation, recessions, and stock market crashes. Why isn’t that happening now?

I see three key reasons why the stock market is shrugging off this conflict. First, the price of oil went up by multiples in the 1970s, while today it is only up around 50% from the start of 2026. Second, the United States economy and its leading companies are much less exposed to oil as an input cost than they were 50 years ago, when the country was a manufacturing powerhouse. Third, the United States is now the world’s largest oil producer, giving it greater flexibility to manage price and supply fluctuations domestically.

The U.S. economy will assuredly be hurt if oil prices stay elevated for a significant time. Rising gasoline prices will hurt consumer discretionary spending, among other inputs, for sectors like the airline industry. But the action in the stock market in recent years has been driven by internet companies and artificial intelligence (AI), which are minimally affected by rising oil prices. The sectors that would be most negatively impacted now only account for slivers of the main indexes. The AI boom is getting its electricity from the United States’ natural gas, renewables, and nuclear power. Oil is simply not a big part of that story.

Where do we go from here?

If international markets are largely cut off from Persian Gulf-sourced oil supply, that could spell trouble for regions such as South Asia, China, and Europe, which rely on energy imports. It would also have severe impacts on specific sectors of the economy. Airlines, for example, could face jet fuel supply issues, especially in Europe. Again, this will negatively affect parts of the global economy that rely heavily on imported oil. But it does not mean the United States stock market will crash.

I expect that U.S. stock market returns in 2026 will be driven by sentiment around semiconductors, AI, and the potential public debuts of several massive private companies — SpaceX, OpenAI, and Anthropic. Unless oil spikes significantly from here, there should be minimal impact on the stock market in the short term. Investors should not try to react to the Iran conflict when building their stock portfolios, regardless of how the situation plays out.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}