Software had a chance to take the baton — but chips grabbed it back.

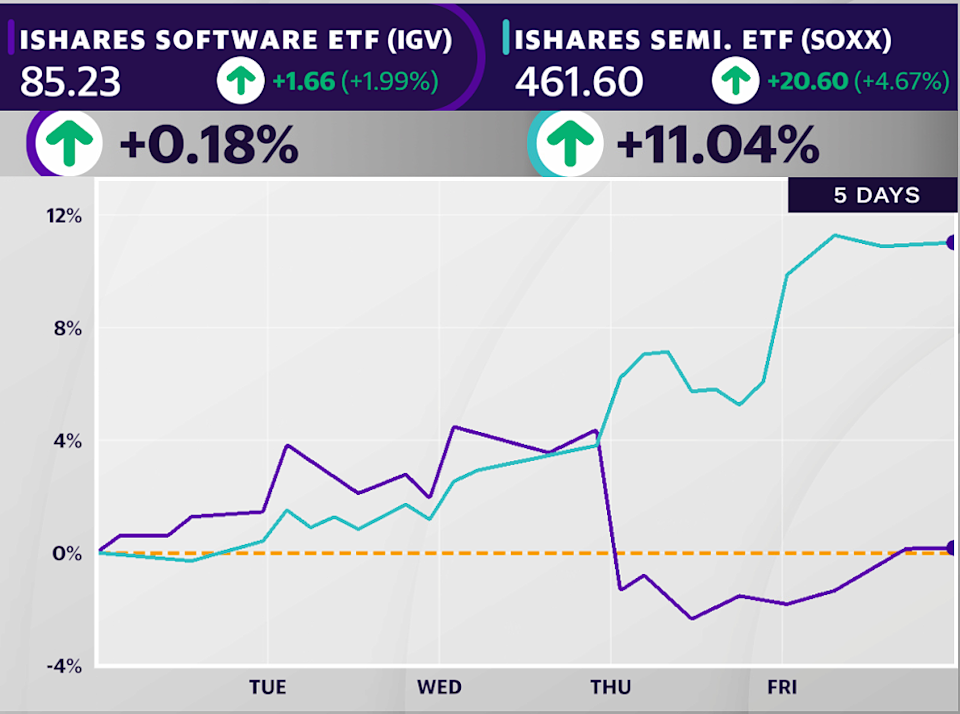

The iShares Expanded Tech-Software Sector ETF (IGV) is no longer breaking down. After sliding over 5% on Thursday — its worst day since the April 4 post-”Liberation Day” sell-off — it fought back to finish slightly positive on the week.

That rebound still leaves it far behind the iShares Semiconductor ETF (SOXX), which is up 11% over the same stretch — a sharp reversal from the broader tech-breadth story that had been building. One chart making the rounds this week showed the software vs. semis ratio posting its biggest one-day drop on record.

That doesn’t kill the software comeback thesis. But with the broader market surging higher, bulls really wanted to see IGV pressing to fresh April highs by now. Instead, the group pulled back and handed leadership right back to chips.

The good news for software bulls is that IGV did hold where it needed to, finding buyers near two key levels landing at $82: its 50-day moving average and the 50% retracement of the move from its April 10 low to Wednesday’s high.

That keeps the false breakdown and recovery case alive, even if the group is no longer leading.

Meanwhile, the PHLX Semiconductor index (^SOX) and related iShares Semiconductor ETF are riding a record 18-day winning streak — with the past 13 sessions also marking record highs. The index is having its best month since February 2000, up 40% in April.

Inside the chip complex, milestones are piling up.

Nvidia (NVDA) cleared $5 trillion in market cap again this past week. Intel (INTC) was up 24% Friday — the most since October 1987 — after clearing its dot-com highs post-earnings. And Texas Instruments (TXN) jumped the most since 2000 after beating on its earnings on Wednesday.

Impressively, none of those names even topped the chip leaderboard.

Arm (ARM) surged over 40% — the most in two years — while Advanced Micro Devices (AMD) was up 25%. Taiwan Semiconductor (TSM), Qualcomm (QCOM), and KLA (KLAC) were all up in the high single digits — a sign that strength is spread across AI chips, foundry, wireless, and equipment.

Software is acting much more selectively.

Synopsys (SNPS) closed the week up 11%, but its double-digit return was an outlier. Cadence Design Systems (CDNS), Palo Alto Networks (PANW), and CrowdStrike (CRWD) were all up 5% to 7%.

But GitLab (GTLB) just hit an all-time low, while Cognizant (CTSH) and Fair Isaac (FICO) made fresh multimonth lows this week. ServiceNow (NOW) is also on pace for a seventh straight monthly decline after having its worst day ever on Thursday.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}