Make better investment decisions with Simply Wall St’s easy, visual tools that give you a competitive edge.

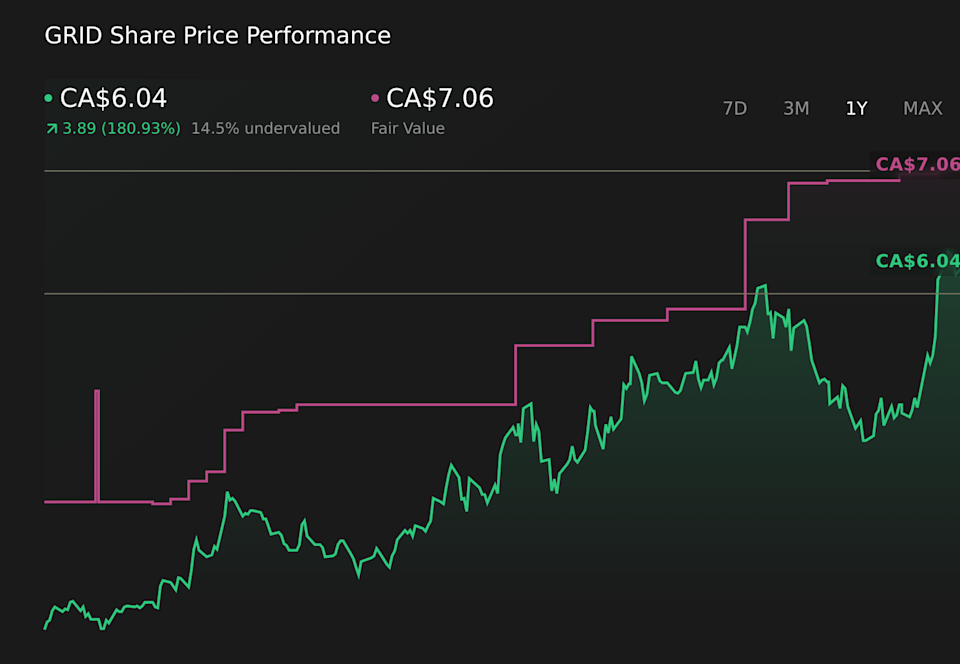

The analyst narrative around Tantalus Systems Holding centers on a CA$7.00 price target that sits close to an unchanged fair value estimate of CA$7.06. Supportive analysts link this CA$7.00 level to the company’s current execution and what they see as a meaningful growth runway, while more cautious voices point out that it may leave limited room for error. As you read on, you will see how these views, along with recent licensing and capital markets developments, shape the evolving story around the stock.

-

National Bank initiated coverage of Tantalus Systems with an Outperform rating and a CA$7.00 price target, which lines up closely with the current fair value estimate of CA$7.06.

-

The new Outperform rating indicates that National Bank views the current execution and growth runway as supportive of the stock trading around the CA$7.00 level.

-

Because the National Bank price target sits close to the CA$7.06 fair value estimate, some readers may view the implied upside as limited, which can make the risk or reward feel less compelling.

-

The reliance on a single, recent research initiation means there is still limited external coverage, which can leave investors with fewer reference points when assessing valuation and execution risks.

Do your thoughts align with the Bull or Bear Analysts? Perhaps you think there’s more to the story. Head to the Simply Wall St Community to discover more perspectives!

-

Fair value estimate is unchanged at CA$7.06.

-

Revenue growth assumption remains about 23.84%.

-

Net profit margin input remains roughly 7.66%.

-

Future P/E moves from about 55.07x to about 55.60x.

-

Discount rate shifts from 7.65% to about 7.68%.

Narratives connect a company’s real world story to the assumptions behind its forecasts and fair value, updating as new information feeds into the model. They help you see how business developments, risks, and numbers all fit together in one place.

Head over to the Simply Wall St Community and follow the Narrative on Tantalus Systems Holding to stay up to date on:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}